In my MJS article on inflation, I wrote:

Looking forward, the inflation surge is probably over. The upward pressure in rental rates is dissipating, while supply chain problems have already disappeared. Finally, because the Fed has been raising interest rates over the last year and a half, thereby slowing the economy’s growth, the labor market has cooled substantially, further relaxing upward price pressures.

That means that in the absence of any big surprises – like another large disruption to oil markets – inflation is likely to continue to moderate, although perhaps more slowly than most people would like. On the other hand, if the Fed has already overly tightened – as the effects of past interest rate increases continue to ripple through the economy – inflation may fall even faster, although perhaps at the cost of a recession.

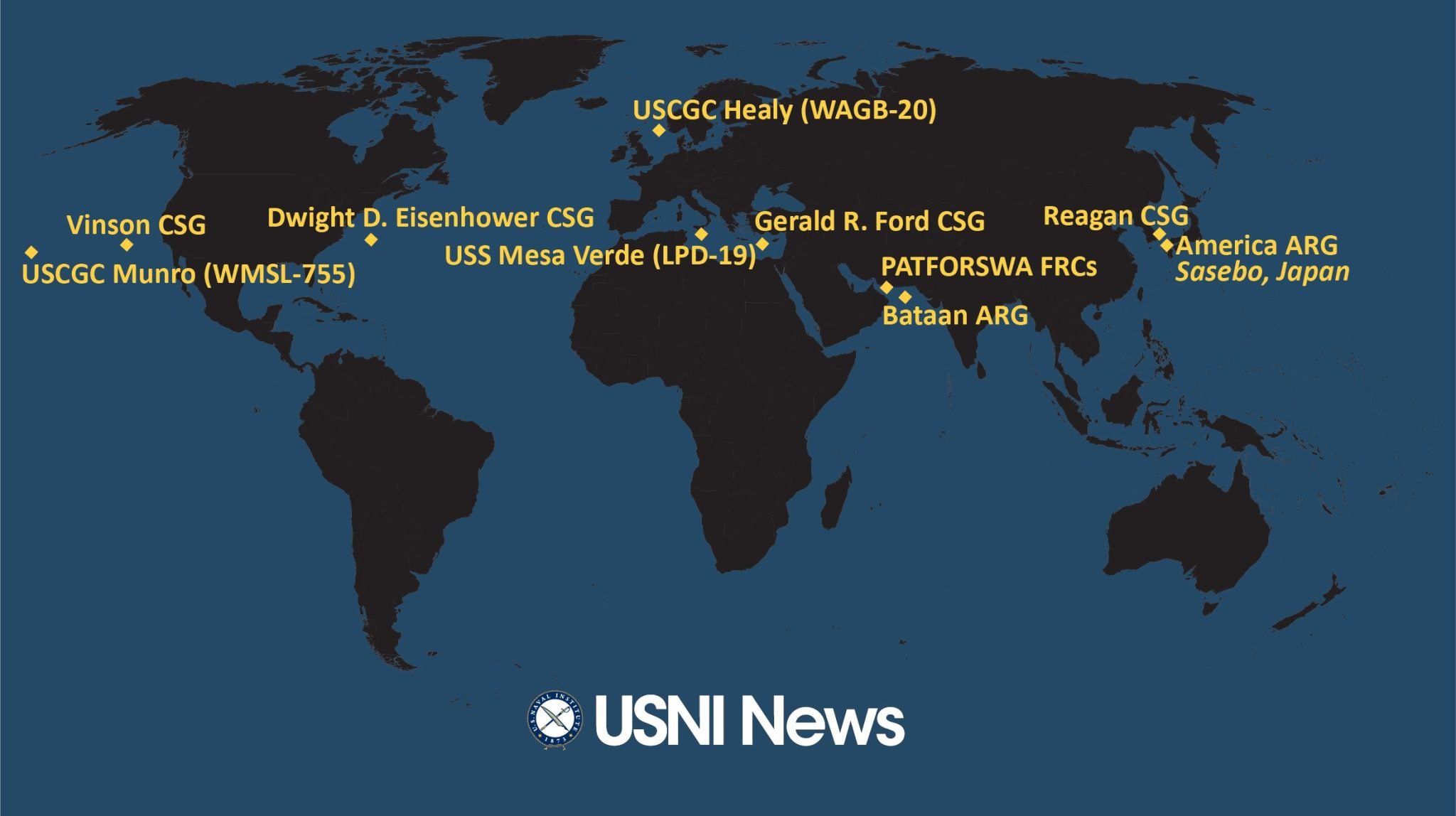

What’s one potential big surprise? Here’s a graphic:

Figure 1: Map as of October 16, 2023. Source: USNI.

Eisenhower Carrier Strike Group (CSG) to Med; Vinson CSG deploying to “Indo-Pacific”. Bataan Amphibious Ready Group (ARG) to Eastern Med.

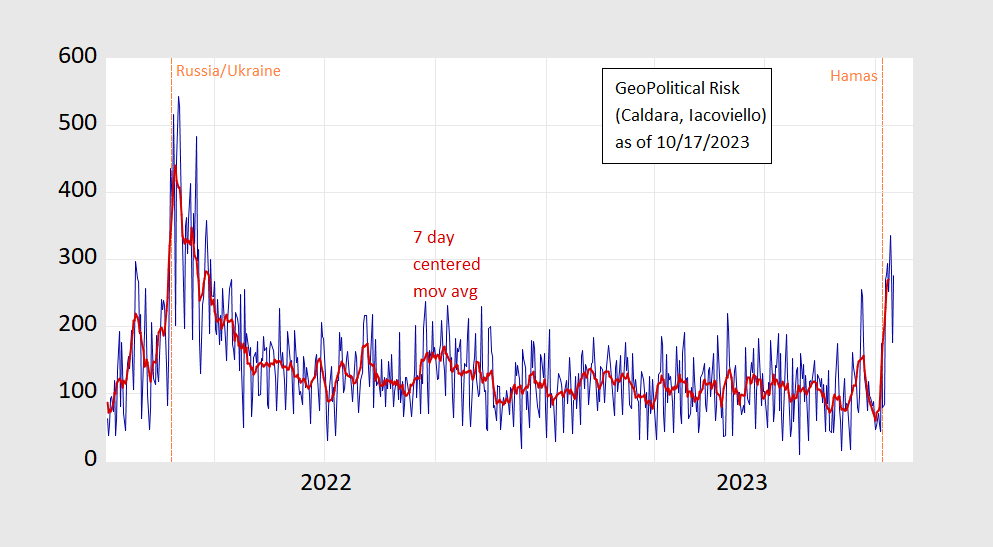

Here’s another:

Figure 2: GeoPolitical Risk daily index (blue), and centered 7 day moving average (red). Source: Caldara-Iacoviello, and author’s calculations.

The GeoPolitical Risk index is elevated, and likely to remain so. Expansion of the war to cause a tightening of oil supplies would certainly exacerbate inflationary pressures.

More By This Author:

Business Cycle Indicators, Mid-October“The Inflation Surge Is Over. Now We’ll See If Interest Rate Increases Cause Recession.”

Inversions, Bear Steepening Dis-Inversions, And Recessions

Comments

Log in or sign up to join the conversation.