Most of the 90 minutes last night was a waste—with both candidates lobbing well-worn clichés, slogans and sound bites at the audience and each other.

But there was one brief moment that made it all worthwhile. That was when Donald Trump peeled the bark off the Fed’s phony recovery narrative and warned that the stupendous stock market bubble it has created will come crashing down the minute it stops pegging rates to the zero bound.

“……Typical politician. All talk, no action. Sounds good, doesn’t work. Never going to happen. Our country is suffering because people like Secretary Clinton have made such bad decisions in terms of our jobs and in terms of what’s going on.

Now, look, we have the worst revival of an economy since the Great Depression. And believe me: We’re in a bubble right now. And the only thing that looks good is the stock market, but if you raise interest rates even a little bit, that’s going to come crashing down.

We are in a big, fat, ugly bubble. And we better be awfully careful. And we have a Fed that’s doing political things. This Janet Yellen of the Fed. The Fed is doing political — by keeping the interest rates at this level. And believe me: The day Obama goes off, and he leaves, and goes out to the golf course for the rest of his life to play golf, when they raise interest rates, you’re going to see some very bad things happen, because the Fed is not doing their job. The Fed is being more political than Secretary Clinton.

Trump thereby landed a direct hit on the false Wall Street/Washington postulate that the Fed has been the nation’s economic savior. And he also elicited an almost instant defense of its destructive, anti-capitalist regime of Bubble Finance—-albeit in the guise of a “fact check” by the New York Times’ Fed reporter, Benyamin Appelbaum.

To be sure, there were actually no “facts” to check in Trump’ statement. It was simply an entirely correct judgment that the utterly unnatural interest rates engineered by the Fed have fueled an egregious inflation of financial asset prices and that “some very bad things” are going to happen when the Fed’s market rigging operation is finally halted.

Still, and opinion or not, Appelbaum emitted a barrage of harrumphing and scolding, implying that Trump is some kind of yokel who does not understand the sacred independence of the Fed:

In attacking the Fed, Mr. Trump is plowing across a line that presidential candidates and presidents have observed for the past several decades. There has been a bipartisan consensus that central banks operate most effectively when they are shielded from short-term political pressures. Indeed, President Richard M. Nixon’s insistence that the Fed should not raise rates in the early 1970s played a role in unleashing a long era of inflation — and in convincing his successors that it was better to leave the Fed to its technocratic devices.

Technocratic devices? Now that is downright balderdash because what the Fed is doing is profoundly and resoundingly political.

To wit, after 94 months on the zero bound the Fed has executed the most massive income and wealth transfer in American history. Upwards of $2.5 trillion has been extracted from the hides of main street savers and retirees over that eight year period (@ $300 billion per year). All of that and then some was gifted to the banks and Wall Street speculators.

Needless to say, a wealth redistribution that monumental in scope and capricious in impact would never see the light of day among the unwashed “politicians” that Appelbaum apparently thinks are too benighted to be involved in monetary policy. That’s because whether or not they embrace the Keynesian nostrum that saving is bad and debt is good, the nation’s politicians are smart enough to know that the sweeping fiscal transfer at the core of Fed policy would be shouted down by the voters in a thunderous chorus of denunciation and derision.

Stated differently, the politician at least know that if the Congress were to enact anything remotely similar to the Fed’s savage and relentless attack on savers and wage-earners, they would be on the receiving end of the torches and pitchforks that would descend on the Imperial City.

In fact, this wanton redistribution from savers to debtors and speculators is occurring only because a happenstance of history has put lethal financial power in the hands of an insulated, unelected monetary politburo; and one that has been taken-over by a tiny posse of delusional and power-hungry Keynesian academics, to boot.

Journalistic hacks like Appelbaum, along with Steve Liesman of CNBC and Jon Hilsenrath of the Wall Street Journal, not only exhibit the worst kind of access-driven mendacity; they also faithfully perpetuate all the myths, shibboleths and outright lies that insulate the Fed from any policy accountability whatsoever.

In the case at hand, Appelbaum claims that it was Nixon’s manhandling of the spineless Fed Chairman, Arthur Burns, in the run-up to the 1972 election that proved the case for the strict “independence” of the Fed. Theresultant decade-long inflationary wave instigated by the nefarious Tricky Dick, therefore, was the inadvertent founding event; it allegedly fostered a newly minted separation of powers doctrine that has invested the 12 members of the FOMC with virtually dictatorial powers over the nation’s financial system.

Well, yes, Nixon was the evil-doer that paved the way to our present form of mutant casino capitalism. But it was not because Arthur Burns had a propensity to bend over in the presence of great power.

To the contrary, the real evil happened in August 1971 when Nixon was persuaded by a passel of so-called free market economists, led and inspired by Milton Friedman, to trash the Bretton Woods system, and sever the dollar’s last link to anything other than the whims and economic theories of the FOMC.

It did take several decades, of course, for the denizens of the Eccles Building to realize that with the shackles of gold and convertibility removed, they were free to generate dollar liabilities at will. Indeed, the great Paul Volcker fully understood what had happened at Camp David, and strove mightily during the next decade, first at the NY Fed and then in the Eccles Building, to keep the fiat genie bottled-up via sheer intellectual discipline and willpower.

But it couldn’t last, and not just because Alan Greenspan checked in his hard money doctrines in the cloak room of the Eccles Building the first day he arrived and never reclaimed the check. What happened was that the financial press discovered that it could swap journalistic integrity for access to the Fed’s inner sanctum, and the rest is now history.

What has materialized, in fact, is a cult of central bank flattery and subservience that is every bit in the emperor has no clothes modality. Not since the days of Bill Greider has a mainstream journalist even dared to suggest that Fed policies have untoward effects on the people or that its real function is to serve the interests of its Wall Street masters.

But now it’s gotten downright hideous. There is not an honest price left in any precinct of the financial system. Dangerous, unstable speculative bubbles infest every corner of the money and capital markets.

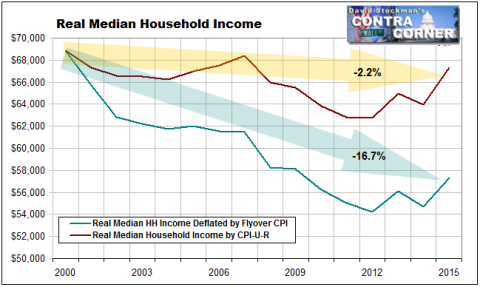

Likewise, the Fed’s fatuous policy of inflation targeting has caused the massive off-shoring of breadwinner jobs to the China Price for goods and the India Price for services. And that wasn’t the half of it.

At the same time, this sweeping and perverse job destruction policy has generated massive slack in the domestic labor markets—upwards of 180 billion hours in quantitative terms. That overhang, in turn, has suppressed nominal wage rates in the middle and bottom end of the labor market, causing wage-earners to fall increasingly behind a relentlessly rising cost of living.

Furthermore, our monetary rulers then added insult to injury by fueling the fantastic bubble in the stock market that Trump so accurately called-out last night. And the problem is not just that it will soon crash and wipe-out tens of trillions of paper wealth.

Actually, the real evil of ZIRP and QE has already been done.

To wit, can anyone not drinking the Wall Street Cool-Aid believe that John Stumpf and his patron, St, Warren Buffet, were actually running a bank?

In fact, the C-suites of corporate America have become stock market gambling dens. Corporate balance sheets have been strip-mined to fund the greatest financial engineering ponzi schemes—trillions in stock buybacks, M&A deals and other leveraged distributions — ever conceived.

The truth is, Janet Yellen is a paint-by-the-numbers academic fool who has no clue about the havoc she and her posse have unleashed on the American economy. Yet she gets away with it exactly owing to the “Fed independence” cover story so mendaciously peddled by the likes of Appelbaum, Liesman and Hilsenrath.

So thank heavens for the Donald. He knows a “rigged” operation when he sees it, and, at least last night, was undomesticated enough to let 100 million voters hear the truth.

I caught that too. It was likely completely missed by most of his supporters, but #Trump hit the nail on the head. It will be a scary day indeed.