Here’re some indicators at the weekly frequency for the real economy.

(Click on image to enlarge)

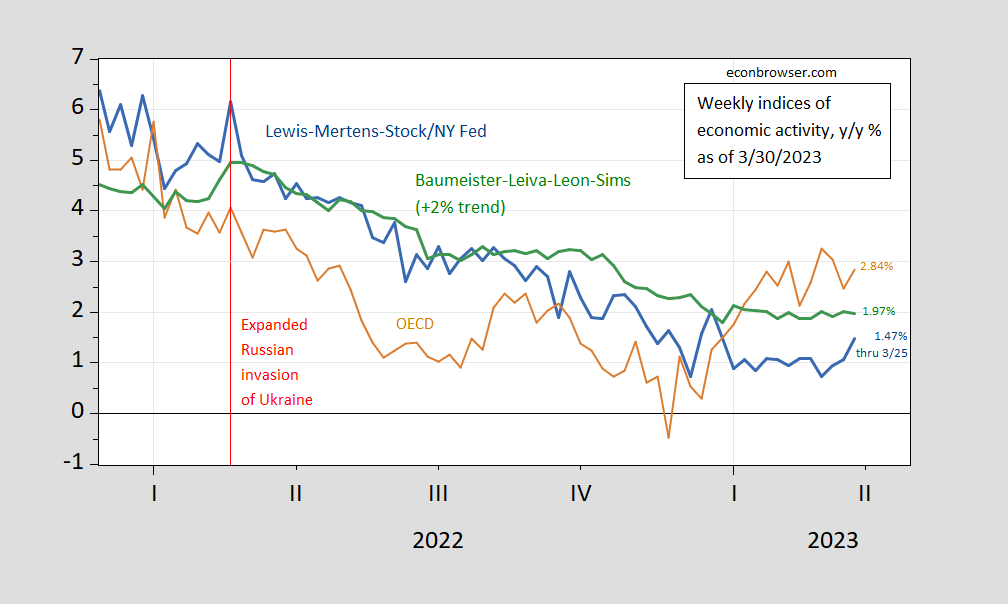

Figure 1: Lewis-Mertens-Stock Weekly Economic Index (blue), OECD Weekly Tracker (tan), Baumeister-Leiva-Leon-Sims Weekly Economic Conditions Index for US plus 2% trend (green). Source: NY Fed via FRED, OECD, WECI, accessed 3/30, and author’s calculations.

The Weekly Tracker continues to read strong growth at 2.84%, for the week ending 3/25, exceeding the WEI (1.47%) and WECI+2% (1.97%). The WEI reading for the week ending 3/25 of 1.47% is interpretable as a y/y quarter growth of 1.47% if the 1.47% reading were to persist for an entire quarter. The Baumeister et al. reading of -0.03% is interpreted as a -0.03% growth rate in excess of long term trend growth rate. Average growth of US GDP over the 2000-19 period is about 2%, so this implies a 1.97% growth rate for the year ending 3/25. The OECD Weekly Tracker reading of 2.84% is interpretable as a y/y growth rate of 2.84% for the year ending 3/25.

Recall the WEI relies on correlations in ten series available at the weekly frequency (e.g., unemployment claims, fuel sales, retail sales), while the WECI relies on a mixed frequency dynamic factor model. The Weekly Tracker — at 2.84% — is a “big data” approach that uses Google Trends and machine learning to track GDP. As such, it does not rely on actual economic indices per se.

The WEI reading, if applied to Q1, implies 2.37% (q/q SAAR). GDPNow as of 3/24 was 3.2% (q/q SAAR), while as of today, S&P Market Insight (nee Macro Advisers/IHS Markit) tracking is at 1% q/q and Goldman Sachs tracking is at 2.9% (as of Tuesday).

For the implications of GDPNow nowcast and IGM median, see this post.

More By This Author:

GDP (3rd), GDO, GDP+Deposits On The Move

Stress

Comments

Log in or sign up to join the conversation.