Stocks have maintained their descent downwards all week and it remains to be seen if today or Friday will bring an uptick before the Labor Day holiday.

Yesterday the S&P 500 closed at 3,955, down 31 points, the Dow closed at 31,510, down 280 points and the Nasdaq Composite closed at 11,816, down 67 points.

A comparative look at Monday and Wednesday's "Most Actives" paint a dour picture of this week's action to date.

Chart: The New York Times

"Down into the ground, to get out of the rain, boom-boom-boom-boom...", as the song goes.

Market futures are trading in the red this morning. S&P 500 market futures are down 28 points, Dow market futures are down 187 points and Nasdaq 100 market futures are down 123 points.

Here's a round-up of the glum news.

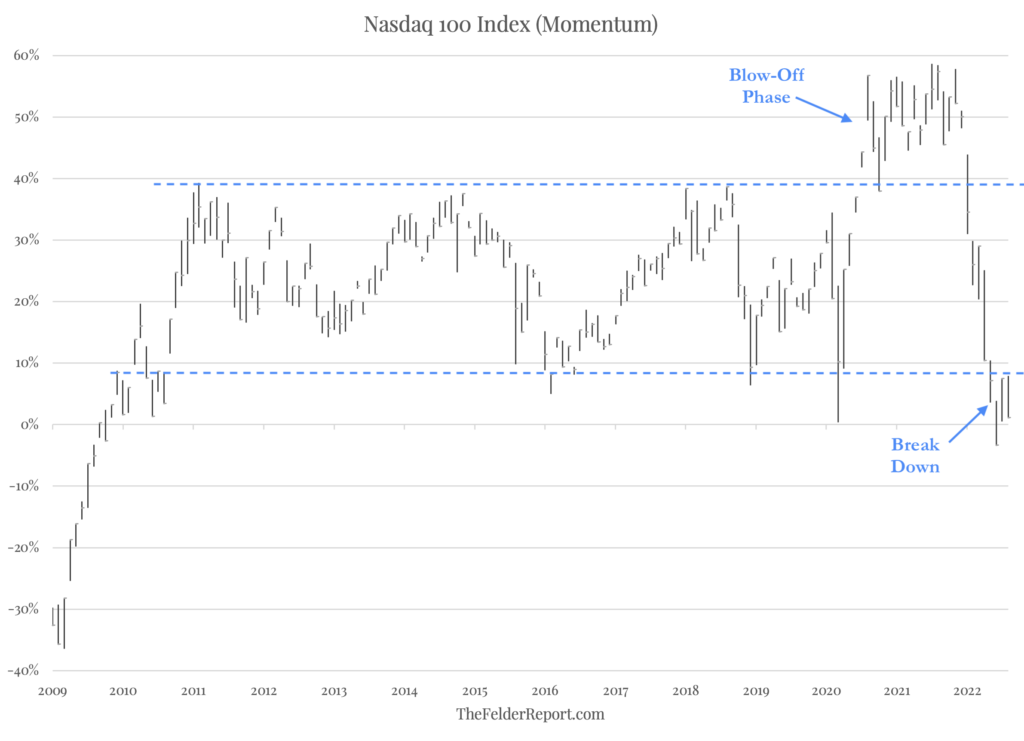

Contributor Jesse Felder writes that The ‘Massive Momentum Structure’ In The Stock Market Is Breaking Down.

"During the bull market that dated back to the 2009 low, the Nasdaq 100 Index formed a clear momentum range between roughly 40% (above the 36-month moving average) on the high side and 10% on the low side."

"The post-COVID rally saw a breakout above the upper end of that range, which represents the final “blow-off phase” of the bull market. This year’s reversal is notable in that not only did momentum fail to hold support at the 10% level for the first time in over a decade, it also failed to hold the 0% level, a “declarative first leg of decline,” in Michael’s words. And even to the untrained eye, it should be quite obvious that a major change in character is now underway."

TalkMarkets contributor Christopher Lewis forecasts that the outlook for the S&P 500 Continues To Look Weak.

"The S&P 500 initially tried to rally during the trading session on Wednesday but gave back gains as it continues to look like the market is ready to go much lower. This is a market where you fade rallies, but we also have the job numbers coming out on Friday, meaning that Thursday could be a bit of a lost trading session...people are starting to wonder whether they (The Fed) are going to ignore any signs of weakness in the economy in order to fight inflation. If inflation continues to be sticky, it’s difficult to imagine a scenario where the market simply takes off to the upside due to the concerns out there that people will pay attention to. As far as buying is concerned, I don’t have a scenario in which I’m willing to do it in the short term, and I will look at rallies as an opportunity to short this market as soon as we see signs of exhaustion."

Contributor Mish Schneider finds that The Russell 2000, Retail And Transportation Tell A Story.

Here is what she has to say about the state of the market from the point of view of the transportation index.

"The transportation sector IYT has been one of the biggest drivers of the commerce in recent years. With earnings growth slowing and valuations at above-average levels, some investors are wondering which sector can continue to lead and if Trans can continue growing, but the new lows look a little murky."

"Trans measures how many goods are transported globally."

The Staff at Bespoke Investment Group provides a historical look at First Day Of The Month Trends.

"Breaking this down further, below we break down some seasonal trends for the first trading day of September relative to all other months over the last 50 years (since 1972). During this span, the first trading day of September has been weaker than the first trading day of any other month with the S&P 500 averaging a decline of 0.11%. However, the positivity rate is above 50% and the median performance is a gain of 0.05%, and much of the negativity comes after the index posts a gain in August.

Over the last 50 years, September has averaged a loss of 0.32% (median: -0.07%) on the first trading day of September following gains in August, trading lower 54% of the time. On an average basis, September has been the worst first trading day of the month following gains in the prior month, but when it comes to both median and positivity rates, August is worse. On the other hand, when August resulted in losses for the S&P 500, September has averaged a gain of 0.16% on the first trading day of September, posting gains 59% of the time."

So maybe Thursday will provide a pre-holiday rebound?

Cryptocurrency is not proving to be any more risk-on than equities. Contributor Crispus Nyaga writes Bitcoin Break And Retest Points To More Downside.

"The BTC/USD (BITCOMP) price wavered as investors continued focusing on the extremely hawkish statement by Federal Reserve officials...Cleveland Fed’s Loretta Mester warned that the bank will continue hiking interest rates in the coming months.

“It would be a mistake to declare victory over the inflation beast too soon. Doing so would put us back in the stop-and-go monetary policy world of the 1970s, which was very costly to households and businesses.”

Her sentiment has been shared by most Fed officials, including Jerome Powell. They argue that higher interest rates are necessary since inflation is at an elevated level while the labor market is still tight.

Historically, BTC and other risky assets like stocks tend to underperform in a period of high-interest rates...Meanwhile, the fear and greed index shows that investors are getting fearful. It dropped from last week’s greed zone of 57 to the fear level.

BTC/USD forecast

The four-hour chart shows that the BTC/USD pair has been in a strong bearish trend in the past few weeks. The pair managed to move below the important support at 20,772, which was the lowest level on August 21st. It has also formed a break and retest pattern.

The pair moved below the 25-day and 50-day moving averages while the Relative Strength Index (RSI) has moved slightly below the neutral point at 50. Therefore, the pair will likely continue falling as sellers target the next key support at 18,500.

Though TM contributor Marc Chandler 's Editor's Choice column August CPI At 9.1%, While The Core Rate Jumps To 4.3% does not portend particularly positive developments, buried in the Asia-Pacific comments are these notes about the Japanese economy, allowing us to close-out today's column on a positive note.

"Japan's industrial production and retail sales were better than expected. Industrial production has surged 9.2% in June (month-over-month) in a response to the re-opening of Shanghai from COVID lockdowns and many expected a small pullback in July. Instead, the preliminary estimate has it growing by another 1% in July. Autos, boilers, and turbines output grew, according to the report. Retail sales rose by 0.8% in July, more than twice the median in the Bloomberg survey after the June series was revised to show a 1.3% decline rather than 1.4%. Autos, food, and beverages led to the better-than-expected report. Today's data suggests a firm start to Q3. Economists expect the world's third-largest economy to expand by around 2.0% in Q3."

Enjoy the holiday weekend.

More By This Author:

TalkMarkets Image Library

Tuesday Talk: Back In The Same Place

Thoughts For Thursday: Waiting By The Fishing Hole

Comments

Log in or sign up to join the conversation.