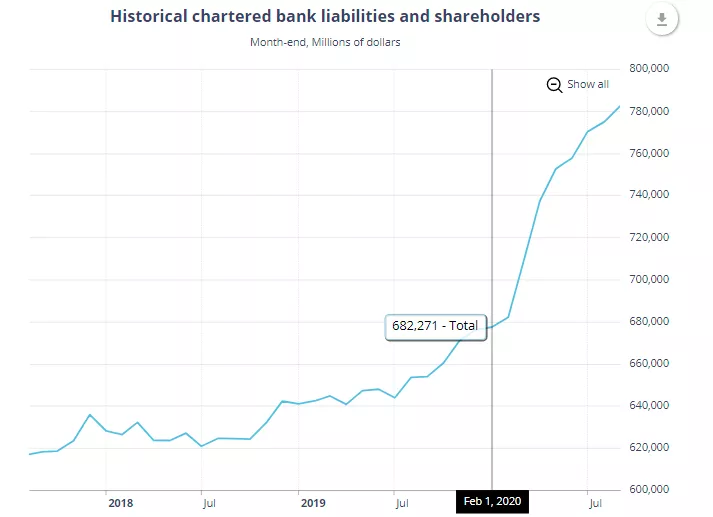

Among the many facets of the economy affected by the pandemic were commercial bank deposits. As the economies shut down in unprecedented ways, individuals and businesses withheld consumption and much of the savings flowed into the banking system. Canadian banks experienced a surge in deposits as they sought protection against a totally unknown threat from the spread of the virus and the economic shocks that followed. Canadians were not different from other developed nations in this regard. Although the worse of the pandemic has passed and life seems to be returning to normal, bank deposits continue to remain relatively high. Savers, for the first time in a decade or more, are offered deposit rates that are attractive. The commercial banks, for example, offer 5-year GICs at 4.5% and non-bank lenders at even higher rates.

Figure 1 Canadian Bank Liabilities

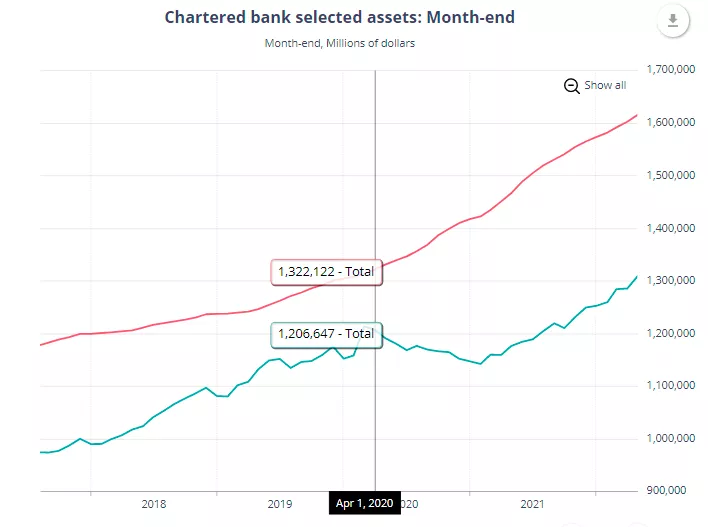

Throughout the very difficult times, starting in March 2020, when the economy was shutdown and until its reopening in the spring of 2021, the banks extended credit to the mortgage market and supported the housing market in general. Business credit was restricted, initially with the shutdown during the worse of the pandemic days, but there was some relief to the business community once the economy re-opened and bank credit grew.

Figure 2 Mortgage Lending (Red) and Business Lending (Green)

Now the lending environment has, once again, shifted. The Bank of Canada signals that it will raise its policy rate until inflation moves much closer to its target rate of 2%.Many consider the Bank in the process of making a policy error.And, the bond market supports that argument. The yield curve has inverted---- the 10yr-2yr spread is minus 50bps –and continues to signal a recession is on its way. The housing market is fearful of a serious downturn as monthly sales decline.

Should the banks tighten credit to the extend that the loan -to-deposit ratio declines, then the odds favor a significant downturn. Unable to reverse the growth in deposits, the banks may simply choose to restrict credit growth which is troublesome for banks’ margins. Any lack of lending to match deposit growth can result in squeezing bank profits. This is the over-riding concern for banks. The overriding concern for the broad economy is that credit restrictions are the primary reason for an economic slump.

More By This Author:

Comparing The 1970s Stagnation To Today’s Economic Conditions

Mortgage Rates in Canada are Not Destined to Increase

The Federal Reserve is whistling by the graveyard

Comments

Log in or sign up to join the conversation.