The recent announcement by the Bank of Canada that its policy interest rate will increase by a full 100bps set off a flood of analysis regarding the future of mortgage rates. Immediately, the financial media jumped to the conclusion that the 5-year fixed rate, the most popular rate adopted by Canadian homeowners, would steadily increase. There are constant references to warn future borrowers to brace themselves for a run-up in mortgage rates in the coming months. However, the setting of mortgage rates is never a matter of directly translating from the bank rate to the mortgage rates . A lot more goes into determining mortgage rates.

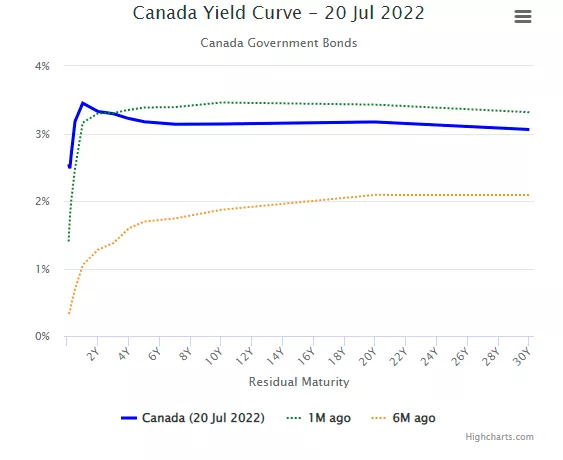

The mortgage lender’s funding cost determines most of what goes into setting the mortgage rate. Here, we need to turn to the Canadian bond market for an indication of the costs of funds. Customarily, a commercial bank will set its mortgage rate about 1.5%-2% above the 5-year Canada bond yield, depending on market conditions. Even before the Bank of Canada raised its rate on July 13th the commercial banks’ cost of funding was declining as evident by the flattening of the yield curve beyond 2-year money. More to the point, the most recent announcement of the rate hike resulted in a yield-curve inversion, in which long-term interest rates are lower than short term rates. Although not a foolproof forecasting tool, an inversion is a strong signal that bond investors expect recessionary conditions to be near at hand. The bond market is saying that the Bank of Canada will be forced to lower rates, once the economy starts to slump.

The Bank of Canada has been targeting inflation for several decades and they have been successful in keeping inflation within its 1-3% target. So far, so good. Now, that inflation has jumped dramatically to 8%, the Bank has adopted a highly aggressive policy, quickly and decisively, to reign in overall demand in the expectation that this will wrestle inflation to the ground. Reigning in economic performance often comes with a cost in which a central can be perceived as overdoing rate increases and, ultimately, causing a recession.

Whiter the future of the 5-year mortgage in Canada? A lot will depend on the cost of funds available to the commercial banks, and the cost of funds depend on the strength of the overall economy. The U.S. economy is showing signs of weakening with 2022 Q1 registering a small contraction and early indications that Q2 will also be very weak. The US bond market is inverted and market participants are signaling that there is a growing probability that the recession is already underway. Should the US enter a recession, it hard to conceive that Canada will be able to avoid a slowdown. So, before one jumps to the conclusion that mortgage rates are destined to move in only direction, it is necessary to keep a close watch on what the bond market is signaling.

More By This Author:

The Federal Reserve is whistling by the graveyard

Does the Fed Read its Own Research Findings?

Retailers Sound The Alarm Bells About The Coming Recession

Comments

Log in or sign up to join the conversation.