“To act or talk as if one is relaxed and not afraid when one is actually afraid or nervous” ...Webster’s Dictionary

There is a slow evolution in thinking regarding how far the Fed can go before tipping the economy into a full-scale recession. Initially, Chairman Powell was very confident that the Fed had the means to curtail overall demand and hence inflation without contributing to higher unemployment. This confidence is best expressed when Powell took questions from reporters after its May FOMC decision, to wit:

“I think we have a good chance to have a soft or softish landing or outcome if you will. And I’ll give you a couple of reasons for that. One is, households and businesses are in very strong financial shape. You’re looking at, you know, excess savings on balance sheets—excess in the sense that they’re substantially larger than the prior trend. Businesses are in good financial shape. The labor market is, as I mentioned, very, very strong. And so, it doesn’t seem to be anywhere close to a downturn. Therefore, the economy is strong and is well-positioned to handle tighter monetary ( May 4 Press).

Something happened since that May press conference such that Powell is now expressing reservations on how successful the Fed can be in avoiding a recession. In his testimony to the Senate Banking Committee, on June 22, he recognized that a “certain possibility” there is a risk that Fed’s plan for a series of rate hikes could lead to a recession. More tellingly, he acknowledged that ‘’the question of whether we are able to accomplish that is going to depend to some extent on factors that we don’t control.” This is in reference to rising commodity prices stemming from Russia’s invasion of Ukraine and clogged-up supply chains because of China’s lockdowns.

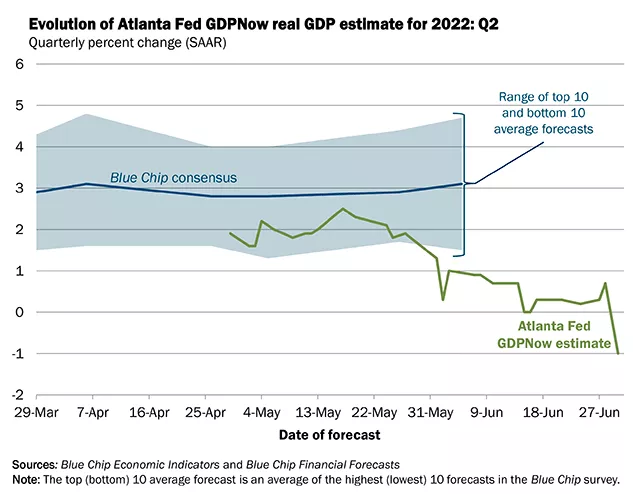

And, indeed, events have overtaken Powell’s earlier optimism. GDP shrank by 1.6% in the first quarter of 2022, in stark contrast to the nearly 7% annualized GDP expansion in the prior quarter. Bear in mind that these results for Q1 preceded the most recent interest rate hikes. The Fed may not have appreciated the extent to which the economy was already decelerating when it started on its current path. Forecasters, including the Fed’s own forecasting group, are now anticipating further declines in Q2 which would then qualify, by definition, as a recession. The only question remaining is how long and deep will the recession be.

The Fed has too much at stake politically to pause or back off . So do not expect the Fed to throw in the towel any time soon. They have made it abundantly clear that they fear the consequences of sustained inflation damaging the economy above all else. Yet, they are still whistling by the graveyard should the incoming data continue to disappoint.

Comments

Log in or sign up to join the conversation.