We have been subject to a steady chorus of critics calling for more interest rate increases to tame the inflation beast. No longer are 25bp rate increases adequate, but central banks are asked to raise rates by 75pbs at their monthly policy meetings. Paul Krugman wisely pointed out that “there’s a real danger that the Fed may be bullied into overreacting” (Tightening). Krugman and others have argued that raising rates to content with supply shocks will not work, but just lead to sustained higher unemployment without moderating price increases. The Fed has repeatedly argued that it is necessary to curtail aggregate demand---- consumer spending, business investment, and government spending. By bringing demand more in line with supply, inflation can be brought down to the 2% target.

But is excessive aggregate demand the real culprit?

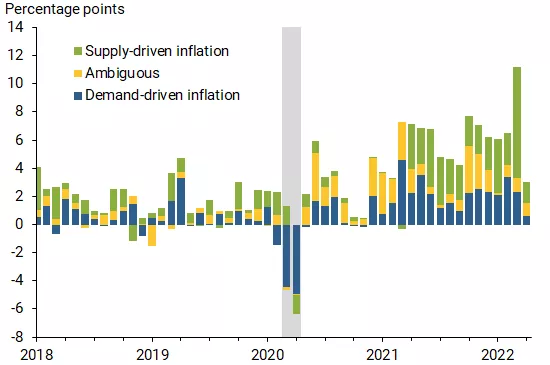

A recent Federal Reserve research report concluded that the bulk of inflation originates on the supply side, to wit:

Separating the underlying data from the personal consumption expenditures price index into supply- versus demand-driven categories reveals that supply factors explain about half of the run-up in current inflation levels. Demand factors are responsible for about one-third, with the remainder resulting from ambiguous factors . (Research)

Source: FRBSF Economic Letter, June 21,2022

The research intuitively identified an ebb and flow in price movements. At the onset of the pandemic, starting in March 2020, demand plunged, especially in the service sector. A year later, demand surged upon re-opening, aided greatly by government direct transfer payments. All the while, the inflationary pressures from supply constraints, especially for goods produced overseas, did not subside during 2021. International trade was greatly disrupted due to labor shortages, production cutbacks, and shipping delays. Industry officials expect shipping disruptions to ease considerably this year, nonetheless, uncertainty continues to dog importers and exporters alike.

Does the Fed leadership fully endorse its own research which concludes that: “factors other than demand account for about two-thirds of recent elevated inflation”? More to the point is the issue of self-induced recession. The Fed research report makes it abundantly clear that ”because supply shocks raise prices and suppress economic activity, the prevalence of supply-related factors raises the risk of entering a period of low growth and elevated inflation levels”, i.e., the worse of both worlds.

Comments

Log in or sign up to join the conversation.