Image Source: Pixabay

For many economic forecasters waiting for the recession to begin is very frustrating, as the Canadian economy continues to resist tipping over into decline. Starting in 2022, when the Bank of Canada announced it was tackling inflation head on, economists started to point out reasons why we should expect a recession, perhaps as early 2023. The Bank clearly had the pedal to the metal, and issued warnings of future rate hikes.

One of the most important early warning signals of an impending downturn is the shape of yield curve. Economists point to the fact that the bond yield curve continues to remain highly inverted, in which longer term rates are well below short rates. The inference is that central banks will be cutting rates in the very near future to ward off a recession. The bond market was already anticipating that rates would fall in the next couple years.

Some of most revered forecasters are still looking a little sheepish as they confront incoming data that refuses to confirm a recession So, why is the anticipated recession not showing up after the most aggressive monetary tightening in over two decades?

Immigration continues to be a driving force in the economy. Demographers are wont to boast that demographics can explain about 80% of all economic, political, and social developments. In 2022, Canada accepted 437,000 immigrants and the 2023 target has been set at 465,000. This trend will continue well into 2025 when 500,000 immigrants are slated to arrive. Added to these numbers are perhaps as much an additional half million who come on temporary visas, many of whom ultimately chose to remain and seek full immigrant status. This influx greatly impacts consumption, and especially housing demand.

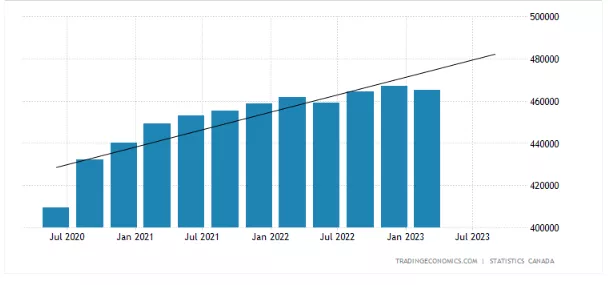

Federal government spending continues to support economic growth. While Federal spending is below trend line, established during the pandemic period, it continues to represent over 20% of the national income. Recently announced budget trimming does not appear to be significant in the overall trend.

Federal Govt Spending

Debt service ratios have not increased. With nominal income continuing to expand at rates equal to or exceeding inflation rates, the household sector can service both mortgage and non-mortgage debt. (Manageable debt levels). Granted that the mortgage market has yet to adjust fully to rate hikes with only 15-20% of existing fixed mortgages to be re-finance this year. However, there appears to be no financial stress in the mortgage and consumer debt markets. What adjustments must be made, due to higher interest rates, are being met with higher wages and salaries.

The housing market has not collapsed as feared. In the first weeks following the Bank of Canada’s announcement of a major policy shift, forecasters predicted a housing crash. The consensus was that housing prices would drop by as much 30% (a number favoured by my commercial bank economists). Tears all around, as homeowners would witness their home equity crumbling. None of this has happened. The national price level dropped, by less than 2% over the past 12 months. (Canadian house prices)

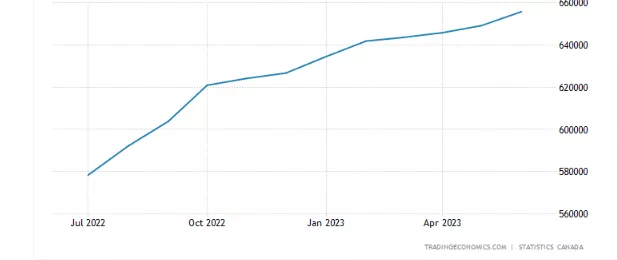

Commercial banks are tightening credit conditions but not to the extent feared earlier. Offering higher deposit rates, the banks have attracted ample funds loanable funds. While setting aside considerable provisions for loan losses, the commercial banks continue to be open for business, albeit more selectively on whom and for which industry borrowing is possible. If there were a recession underway, the credit markets often serve as a tripwire.

Loans to the Private Sector, Canada

However, do not make the mistake that every aspect of the economy is on solid ground. Business capital formation---- investment in new buildings, new equipment, and software--- is well below historical norms. For this reason, Canada’s productivity performance has been well below that of other advanced nations. Finally, our balance trade is going into the red, a reflection in the slow down in international trade, especially from the impact of the Chinese economic malaise.

More By This Author:

Why The Bank Of Canada’s Rate Hikes Are Not Working

The Bank Of Canada Has Entered The Realm Of Overkill

Central Bankers Are No Longer So Self-Assured

Comments

Log in or sign up to join the conversation.