GOOD MORNING ASIA / GOOD EVENING EAST COAST.

AUGUST 16, 2021.

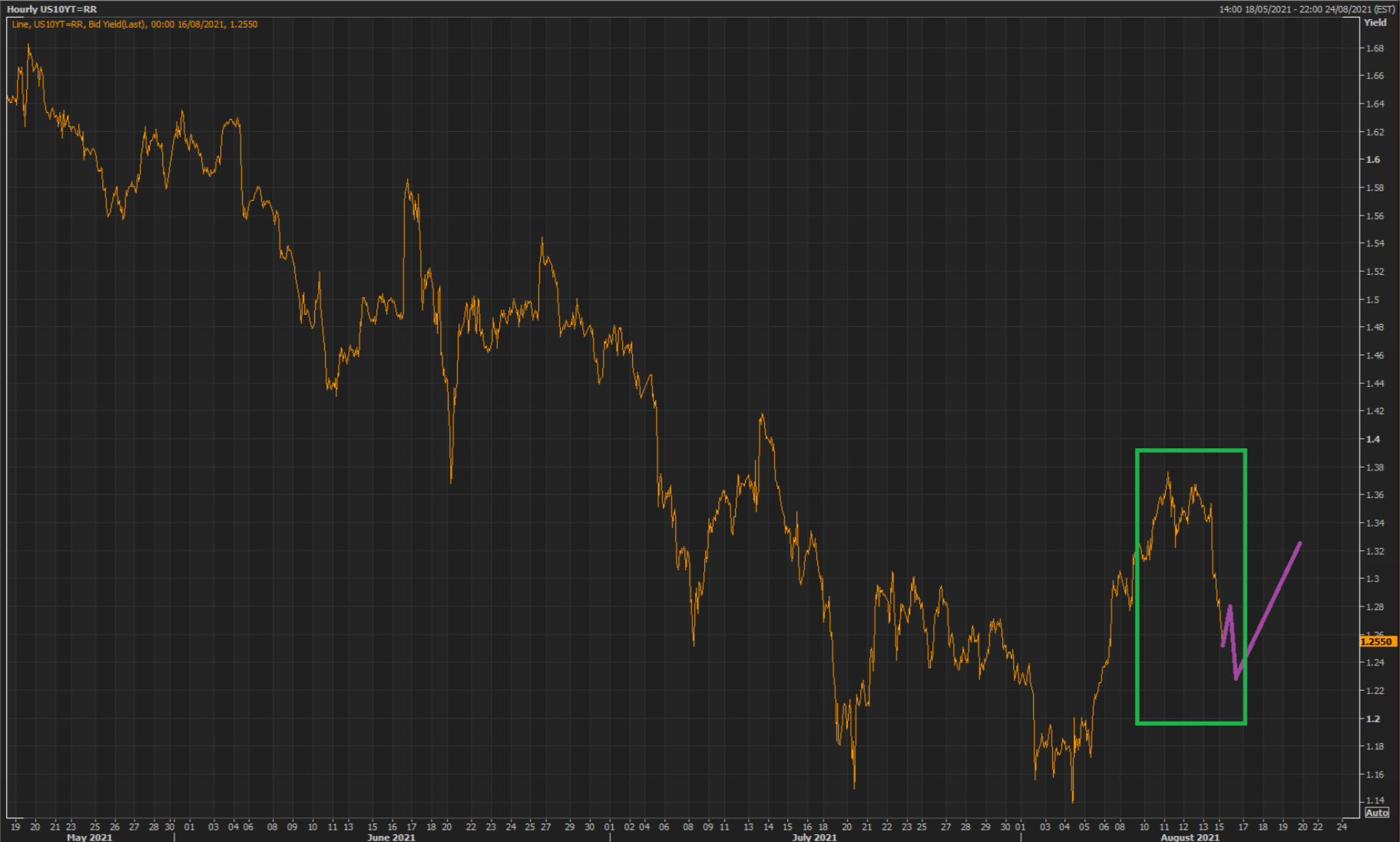

It looks like we are having an irregular correction, one of joshweir's "guy with the long mullet" types. We should expect a rebound in yield starting sometime within the next 24 hours.

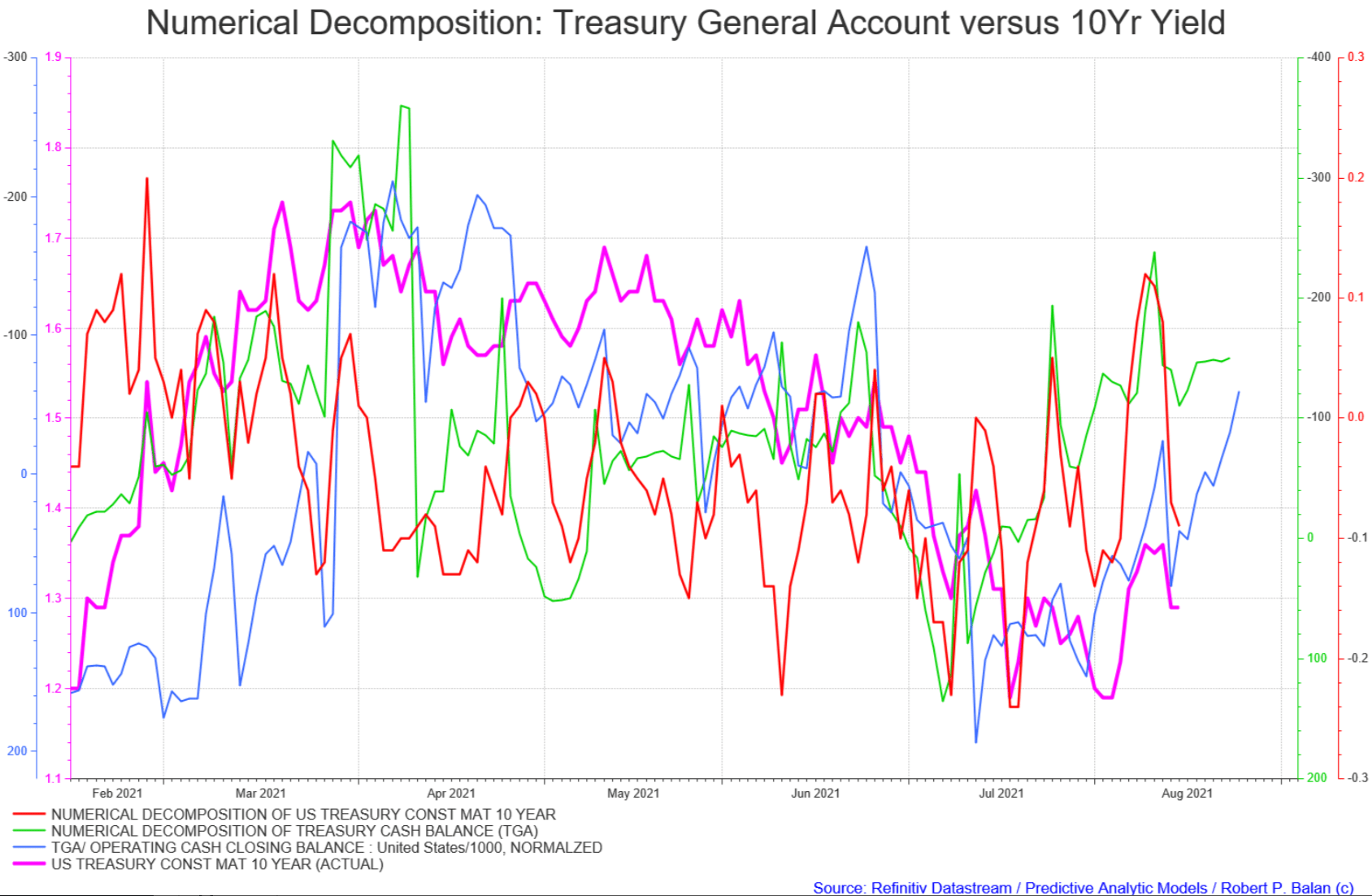

We can clearly see that tendency for a yield rebound as depicted by our quick-and-lazy (num decomp) of the TGA model.

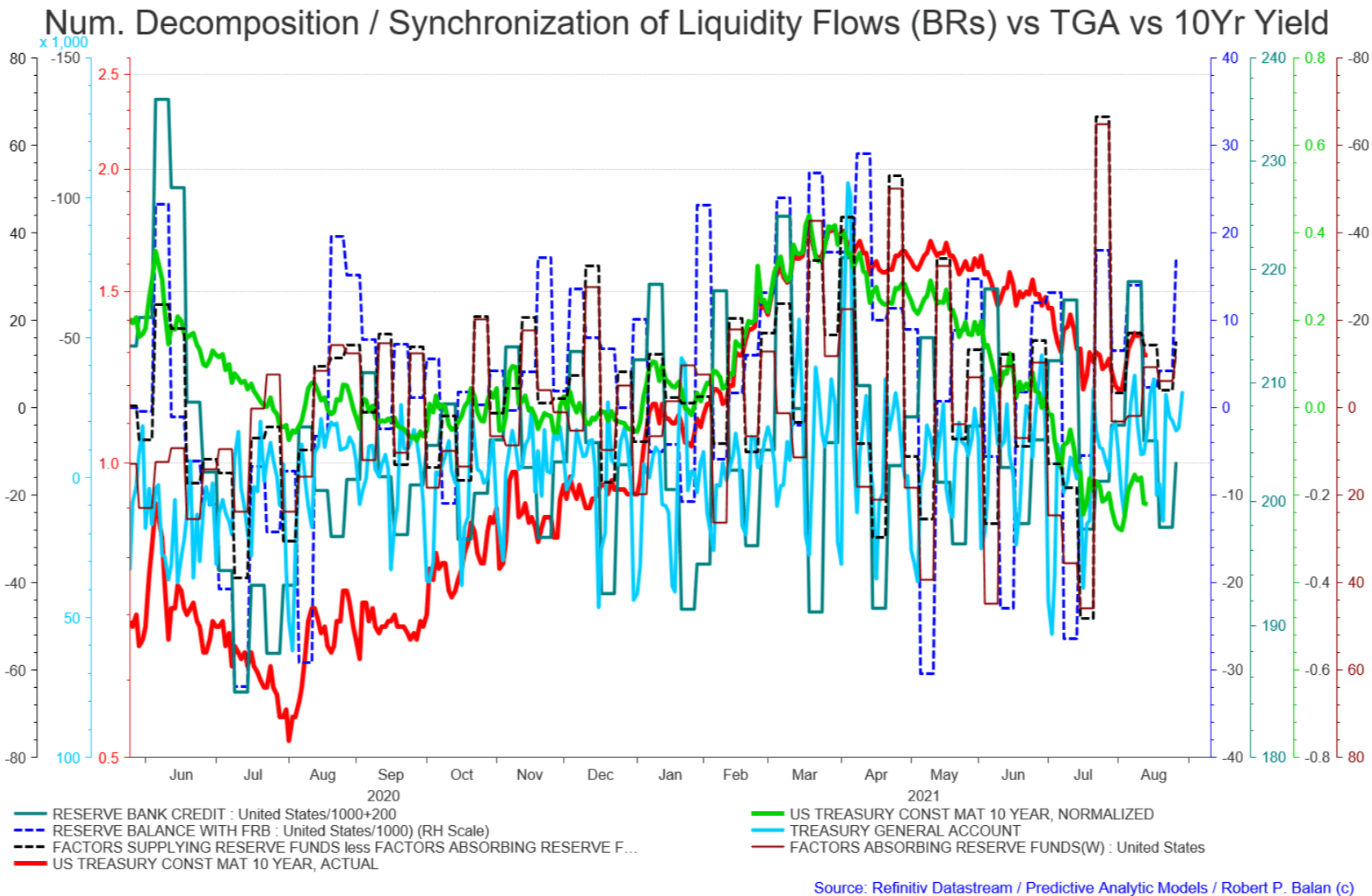

Here is a more robust aggregation of liquidity models showing the Yield's tendency to make a trough very soon, bounce back, and then finally make a trough on the 3rd week of August. From there, we should blast off in yield terms, as well as equity market terms.

So the impression I get is Yield and equities topping out early this week, then have corrections lower (VIX higher) until late 3rd week - early 4th week of August.

We need to translate that into bite sized components. That means bailing out of the long NQs soon, hopefully with a final tail wind provided by still falling yields over the next 48 hours. Then looking for levels to sell YM and RTY, and possibly sell TMF again until end of 3rd week August. Then we get set for a blast off in both equities and the Yield, following the seasonality of new liquidity flows.

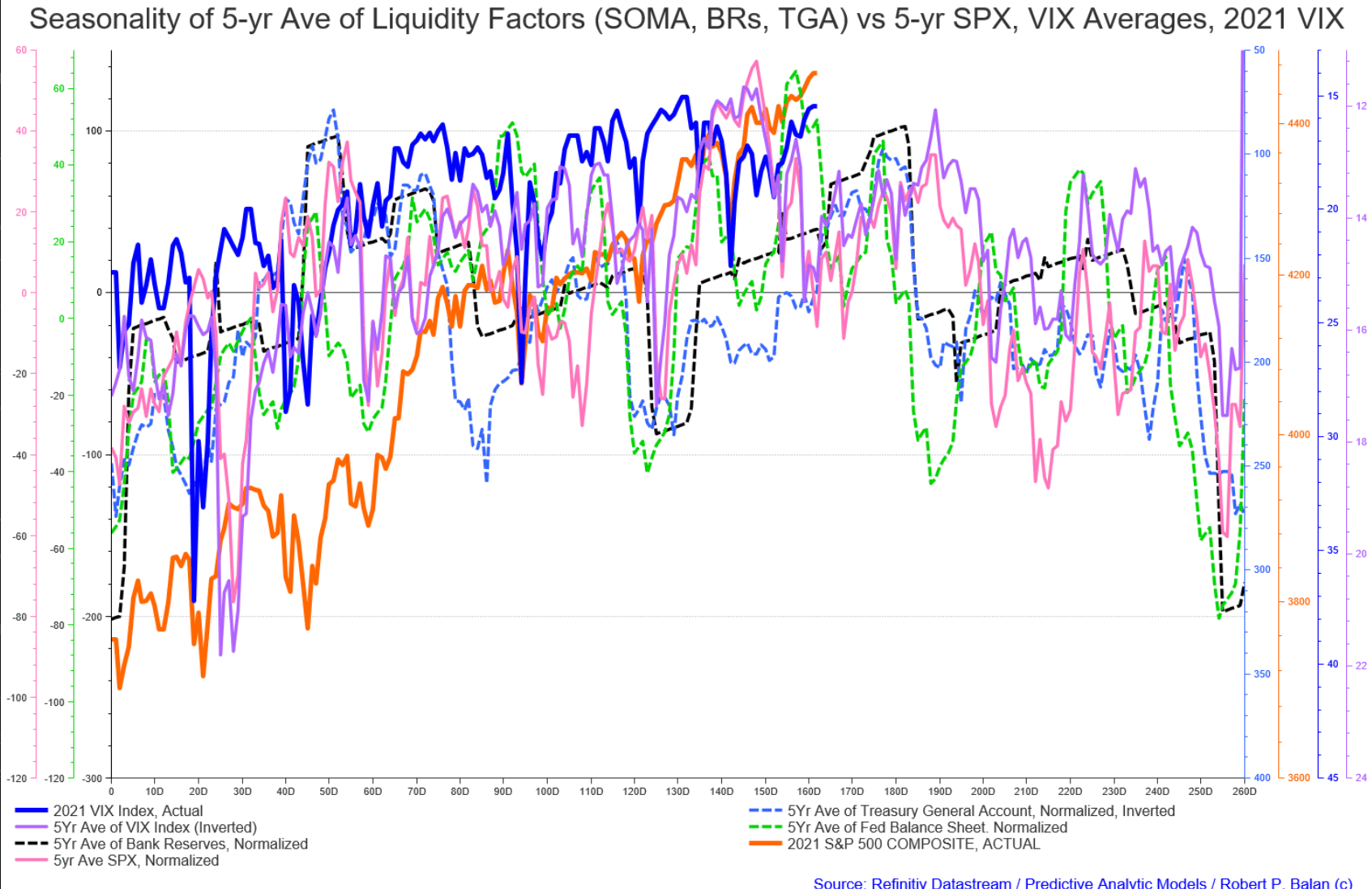

As we concluded a few days ago, the (lagged) impact of current year liquidity flows (which diverged slightly from historical seasonality) also shows that tendency for equities to weaken for the next few weeks. Note especially the slight deviance from the seasonality of the Fed's Balance sheet (dashed green line) but I suspect the current year seasonality profile will not diverge much from historical ones, at least the tendency, allowing for a miss of several days.

The next run-up in risk asst prices may last for four to five weeks, then we get into another liquidity sink hole period. And at that time, the sell off could be longer.

This is the exposure that our new, Weisshorn ETF fund should ideally exploit. But that should not stop us from hedging (even overhedging) a profitable run, and so hopefully its performance would not not lag so far from the main equity-futures based Swing Portfolio. If overhedging is a concept that you have not thought about, you may skip that part, but do try to follow the hedging process.

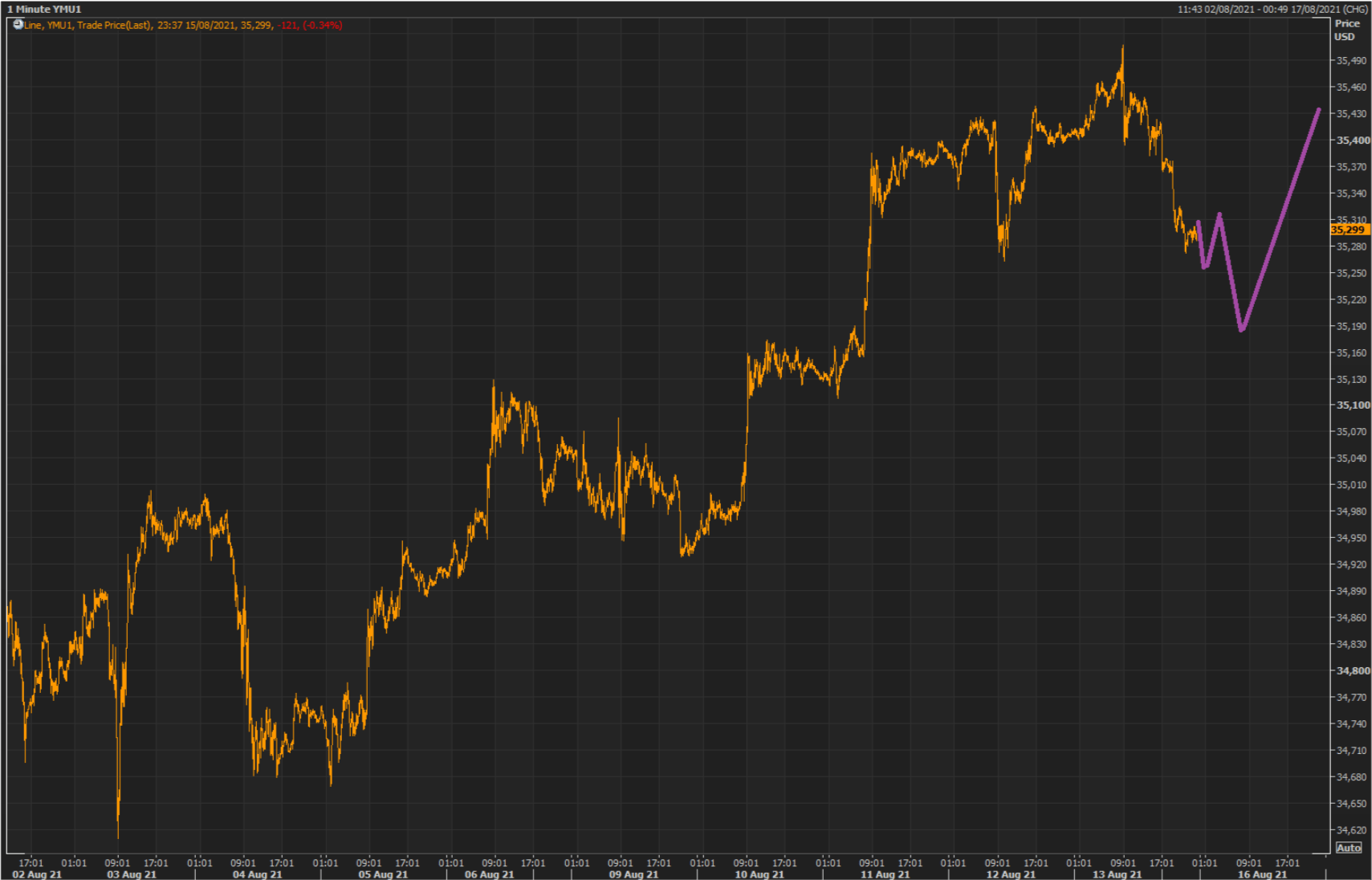

We submit therefore, that the YM decline is in its final stage and we should see a trough soon. YM and RTY should get their chance to shine, as yields pullback higher. We will do long scalps on YM and RTY later in the day.

Meanwhile, we wait for the right levels to do the trades. I get back to the sack, and I will see you gals/guys at Europe opening bell. GN.

-----------------------------------------------------------------------------------

------------------------------------------------------------------------------------

Here are the latest trades and performance of PAM's One-Contract Portfolio, with a margin capital of $100,000, making the same trades as the flagship Swing Fund, but doing consistent, one contract-trades.

----------------------------------------------------------------------------------------

Here is the current status of the PAM flagship Swing Fund, which includes open and closed trades.

During the first seven months of 2021, PAM delivered phenomenal real-dollar Hedge Fund trading performance, the best at Seeking Alpha:

PAM's flagship Swing Portfolio, year-to-date (July 30, 2021) delivered $145,817,615.48 net profit on $11,172,813 margin capital.

Year-to-date performance: 1243.32%.

........