The stock market slipped hard last week, though it was seemingly back on its feet at the end of trading yesterday. Like invisible black ice on pavement, anticipated rate hikes which have yet to materialize were largely blamed for the street's start of the year tumble.

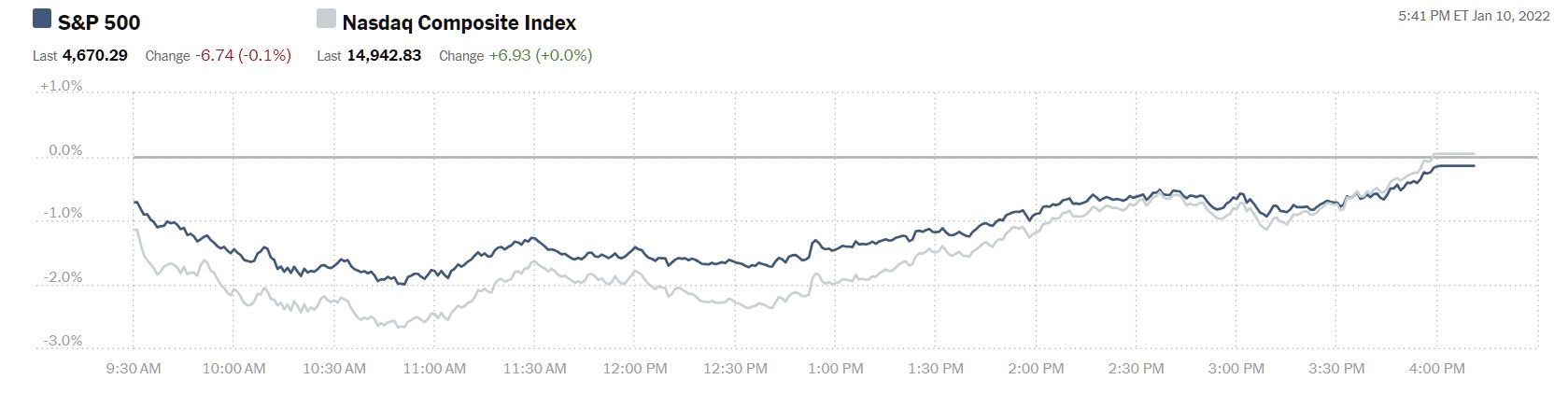

The S&P 500 closed at 4,670, down 7 points, the Dow closed at 36,069, down 163 points, while the Nasdaq Composite closed at 14,942, up 7 points. Market futures, in pursuit of Monday's late in the day rally, are cautiously trading green. Currently S&P futures are trading up 11 points, Dow futures are trading up 40 points and Nasdaq 100 futures are trading up 57 points.

Yesterday's most actives were in the Healthcare, Pharma and Tech sectors. The biggest gainer was vaccine maker, Moderna (MRNA) whose stock was up 9.3%. Forbes reported on a Singapore study that showed the company's vaccine to be the most effective, while elsewhere the company reported it would have an Omicron booster by the fall and Moderna CEO Stephane Bancel suggested that people over 50 and the immunocompromised may require an annual booster.

Chart: The New York Times

With Jerome Powell set to testify before the Senate Banking Committee today as he seeks confirmation for a second term as Chairman of the Federal Reserve Bank, Tuesday Talk takes a look at what some TalkMarkets contributors have to say about interest rate hikes.

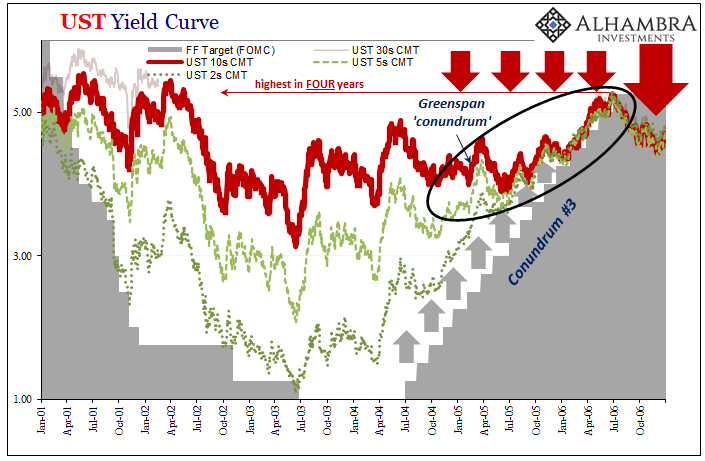

Contributor Jeffrey P. Snider takes a historical look in his article It’s Not Perfume But It Does Smell Funny: Conundrum 5.

"(After George W. Bush's re-election in November 2004) ..with the fed funds target still at 1%, (then Fed chair) Alan Greenspan and his staff of Economists began to consider whether or not they’d done too much; worried they had erred too far on the side of dot-com bust and deflation (which was never a real risk).

So, the doves turned hawks and rate hikes started up and continued one after another after another.

Not even a year into the cycle, however, again Economists were stumped. The Fed was raising rates but LT bond yields just weren’t buying it; on the contrary, the bid for safety and liquidity confounded these rate hikes. As Chairman Greenspan claimed while at the Capitol, the yield curve, “can be thought of as an average of ten consecutive one-year forward rates.”

Therefore, the Fed starts hiking and the entire yield curve is expected to respond, to dutifully obey what everyone including Congress has been told is its master, Master Alan. This wasn’t happening."

Snider labels this 2004-2005 phenomenon as "Conundrum #3" a nod to the notion that in matters of monetary policy everything new is old.

"On the contrary, as ST rates including UST notes toward the front of the yield curve marched upward, LT rates starting at the 7s and out were lower by February 2005 than they had been in June 2004. Dancing his commentary out from fedspeak, Mr. Greenspan’s meaning became very plain all of a sudden when the topic shifted to bond yields:

For the moment, the broadly unanticipated behavior of world bond markets remains a conundrum. Bond price movements may be a short-term aberration, but it will be some time before we are able to better judge the forces underlying recent experience."

"Thus by February ’05 the Federal Reserve’s revered Chairman judged it was far better to lie in front of Congress rather than admit LT yields had bested these “best and brightest” Economists twice already...Rather than citing the idea of too much money as the reason for inflation caution from the Fed June 2004 and onward, instead, Greenspan told everyone:

Whether inflation actually rises in the wake of slowing productivity growth, however, will depend on the rate of growth of labor compensation and the ability and willingness of firms to pass on higher costs to their customers. That, in turn, will depend on the degree of utilization of resources and how monetary policymakers respond."

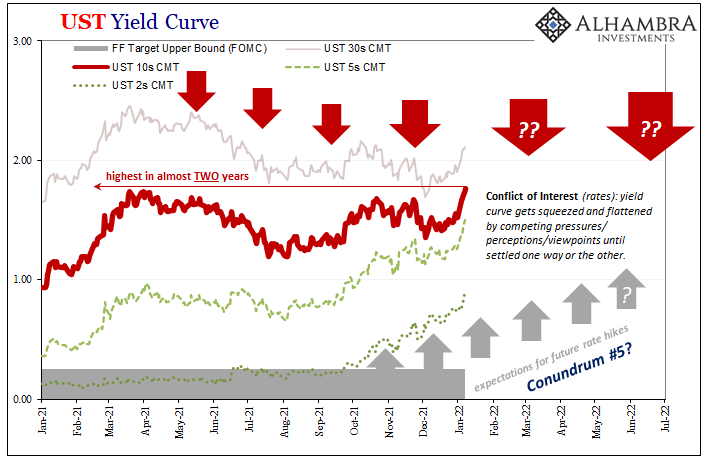

Fast forwarding to January 2022, Snider makes the following observation:

" (Back then in February 2005, Greenspan was sounding) Basically, the same convoluted backdoor nonsense as Jay Powell’s Fed is right now using trying to justify current hawkishness leading to his own conundrum; actually, Powell’s second, as discussed last week; fifth, maybe, overall. Tight labor market, wages, blah, blah, blah.

Is there too much money? They (still) have no idea."

In the chart below Snider presents what he calls the Fed's 5th Conundrum.

"...What had happened in each “conundrum” was the same thing we’d see again in 2018; the Fed can, for a time, influence the short end of the curve up to its middle, or belly, then, contrary to Greenspan’s “series of one-year forwards” nonsense, it becomes all Irving Fisher from there onward...So, if the market judges that growth and inflation prospects aren’t actually great over the intermediate and longer term, this will be reflected in LT bond yields that stay relatively low even if they rise a small amount due to this “hawkish” pressure from below – up until a point (landmine) when the Fisherian perspective takes over regardless of the Fed’s outlook, policy positions, or any kind of Congressional testimony...Conundrum is just an unnecessarily fancy way of attempting to dismiss this conflict of interest rates policymakers always lose."

See the full article for a detailed look at the other Fed conundrums.

TM contributors Padhraic Garvey, CFA, Benjamin Schroeder and Antoine Bouvet in their column, Rates Spark: Still In The Driving Seat write:

"US rates should once again set the tone in global fixed income markets. Powell’s hearing will be an opportunity to gauge the aggressiveness of the Fed’s tightening cycle, and it could see the curve front-load hikes further...The prospect for abrupt policy tightening is keeping investors up at night."

Source: Refinitiv, ING

"The swap curve currently implies 150bp of hikes by the end of 2023, almost priced to perfection when compared to the latest Fed’s dot plot. The question then is, why all the drama? The answer is that, increasingly, investors are seeing an even greater number of hikes if the recent hawkish turn is any guide. This could go one of two ways. Either more hikes are front-loaded to 2022 – this seems to be the way markets are currently thinking – or the tightening cycle continues after 2023...We're expecting the US curve to re-flatten only later this year."

TalkMarkets contributor Cullen Roche in an excellent, but long article titled Who Will Buy The Bonds? outlines what actually happens and might happen as the Fed moves to raise interest rates again.

"(For starters) The Government doesn't need to pay you interest. Now, this is very, very important. In theory, the US Government could fund all of its spending by issuing 0% overnight notes. They could run a deficit and just send brand new cash to the recipients of the excess spending. In this theoretical alternative reality the demand for government-issued money relative to everything else would show up as inflation instead of some policy-determined interest rate."

"I’ve described interest rates as being similar to a dog on a leash. That is, the Fed walks the Treasury market around and decides how much the dog will move at any point. At the handle the Fed has absolute control of how much the leash moves. They set the overnight rate and the dog has no control over it. Yes, the dog can influence it. Sometimes it will run fast (think, high inflation) and sometimes it will run slow (think, low inflation). Sometimes it will stop to poop (think, recession). Heck, sometimes it will even go backwards (think, deflation). "

"What does all of this mean for interest rates specifically? Well, our dog walker has made it pretty clear that they want the dog to slow down so they’re trying to rein it in some. The problem is, every time they try to slow our dog down they seem to overshoot or time the slowdown exactly wrong. This is why the Fed’s stimulus has become permanent. They want to rein the dog in, but every time they do the dog slows more than expected. Rinse, wash, repeat."

"So, how much room does the Fed have before the dog will freak out? Just looking at the current structure of the interest rate curve it looks like they have a relatively razor-thin margin for error here...Another way of thinking about this is asking yourself what would happen to inflation and the broader economy if the Fed shocked rates to 10% tomorrow morning?...Mortgage rates, for instance, would skyrocket and the demand for housing would instantly collapse. All risk assets would reprice massively. You’d get an immediate deflationary shock that almost certainly causes a recession. This is obviously an extreme example, but the Fed is toying with a relative example of this where their margin for error appears much lower than some presume."

"None of this means that interest rates can’t rise or that inflation won’t remain high. I’ve stated that I expect inflation to remain high well into 2022 and then moderate as the year goes on. But asking “who will buy the bonds” is like asking “who will pick up the printed money”? You will. I will. Because in a world of relative value where safe fiat currencies are scarce in a relative sense, it would be irrational not to want to gather up every last USD you can get your hands on because it’s the best currency in a world of bad currencies...(However) I think the Greenspan Conundrum is fully back in play here and that if the Fed starts raising rates aggressively they’ll find themselves backpedaling out of that position before long."

Holy Graf Zeppelin, Batman!

Changing topics, contributor Justin Holt writes that Smart Factories To The Supply Rescue are key to a worldwide economic recovery.

"Digitalization is sweeping through manufacturing plants and transforming today’s sleepy mills into the smart factories of tomorrow...the catalysts include...exponential computing power, Big Data, artificial intelligence (AI), and machine learning (ML)."

These trends can be translated into four technology sector segments which are tracked via the S&P Kensho Smart Factories Index and which investors can participate by investing in the new (10/21) ProShares Kensho Smart Factories ETF (MAKX):

-

Digital Manufacturing Solutions (52.6% of index weight1): Covers the software enabling connected, integrated digitalization of manufacturing activities, including the equipment used for environment sensing and monitoring, advanced process control, and predictive maintenance. Led by cloud adoption, digital transformation with remote capabilities has gone from nice-to-have to need-to-have.

-

Per an Intel research report,2 manufacturers experience up to 800 hours of unscheduled downtime annually (30% of it unplanned), while their skilled workers are aging, leaving 2 million jobs at risk of not being filled.

-

Cost savings and waste reduction are additional catalysts to adoption. A McKinsey study3 found that AI-enhanced predictive maintenance of industrial equipment can generate a 10% reduction in annual maintenance costs, up to a 20% downtime reduction, and a 25% reduction in inspection costs.

-

-

The Industrial Internet of Things (IIoT) (22.9% of index weight): Represents the interconnection of big, ubiquitous data, sensors, instruments, and other devices networked together with computers’ industrial applications. It is key to facilitating manufacturers’ ability to connect, automate, track, and analyze industrial activities.

-

Industrial Machine Vision (17.2% of index weight): Includes technology that combines sensors, cameras, computers, and ML/AI with visual data to identify product defects and model and predict equipment processes and product results.

-

Digital Twins Technology (7.3% of index weight): Provides a virtual replica of any physical product, piece of equipment, or asset. For example, a digital twin could be a virtual version of a manufactured product, the entire production line, an entire factory, or network of plants.

Holt provides the five-year forward growth outlook for each key technology and 2021 performance of companies in each segment in the chart below.

Check out the full article for more information.

From the "Where To Invest" Department we go to contributor Chuck Carnevale's 18 minute video 9 Consumer Discretionary Stocks To Buy.

Carnevale's current suggestions are: AutoNation (AN), Best Buy (BBY), BorgWarner (BWA), DR Horton (DHI), eBay (EBAY), H&R Block (HRB), Mohawk Industries (MHK), Toyota Motor (TM), and Whirlpool (WHR).

As always, Caveat Emptor.

That's a wrap for today, and I will see you this Thursday.

Comments

Log in or sign up to join the conversation.