With two trading days to go in January the major stock indices seem to be set to end the month at new highs and there are fewer analysts trying to insist that the "recession" is around the corner.

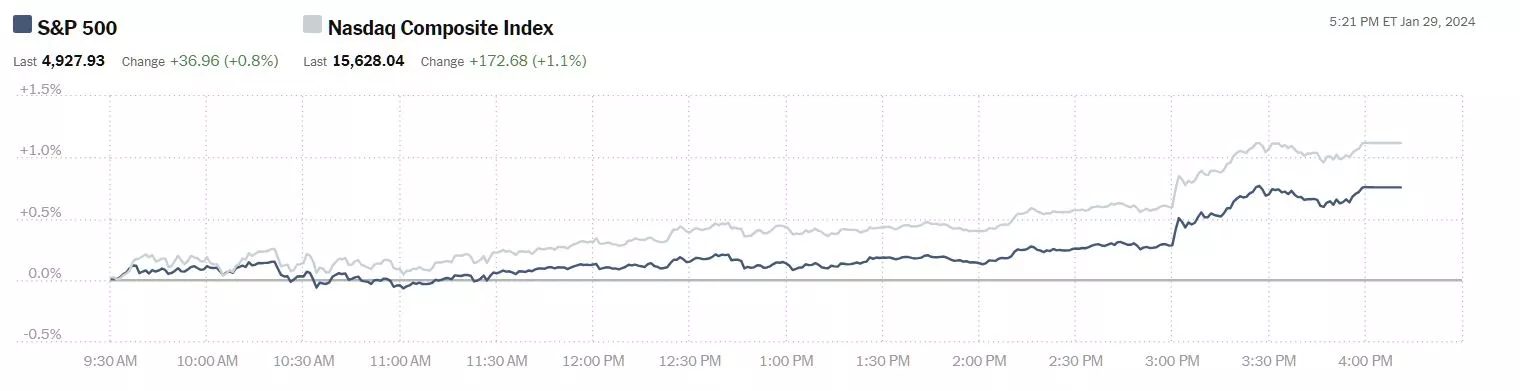

On Monday the S&P 500 closed at 4,928, up 37 points, the Dow closed at 38,333, up 224 points and the Nasdaq Composite closed at 15,628, up 173 points.

Chart: The New York Times

Top gainers in the session were led by Archer-Daniels-Midland (ADM), up 5.6%, followed by Carnival Cruise Lines (CCL), up 4.5% and Illumina (ILMN), up 4.3%.

Chart: The New York Times

In morning futures trading, S&P 500 market futures are trading down 6 points, Dow market futures are trading down 56 points, and Nasdaq 100 market futures are trading down 18 points.

Some of the biggest news of the week comes to us from contributors at the Staff of Just Markets who report Chinese Real Estate Developer Evergrande To Be Liquidated.

"WTI crude oil prices fell by 1.6% on Monday as a Hong Kong court ordered the liquidation of Chinese real estate giant Evergrande (EGRNF) adding to concerns about the economic health of the world's largest oil importer."

Elsewhere JustMarkets staff reports, "Asian markets traded mixed yesterday. Japan's Nikkei 225 (JP225) was up by 0.77%, China's FTSE China A50 (CHA50) decreased by 0.35%, Hong Kong's Hang Seng (HK50) was up by 0.78% on the day, and Australia's ASX 200 (AU200) was positive by 0.30% on Monday.

Australia's December 2023 retail sales fell by 2.7% month-on-month, worse than market forecasts, which expected a 1.0% drop. This was the sharpest retail sales decline since August 2020.

Japan's unemployment rate fell to 2.4% in December from 2.5%, which was in line with the consensus forecast. It was the lowest unemployment rate since January as the number of employed rose 380,000 to 67.54 million and the number of unemployed fell 20,000 to 1.56 million.

China's 10-year government bond yield fell below 2.5%, hitting its lowest level in nearly 22 years, as traders bet that China will further ease policy to support its struggling economy. Expectations that other major central banks will start cutting interest rates this year also give the People's Bank of China (PBoC) flexibility to cut interest rates. Last week, the People's Bank of China announced it would cut banks' reserve requirement ratio by 50 basis points in February, which is expected to free up about 1 trillion yuan of long-term capital for the economy."

Contributor Patrick Munnelly gives us his Daily Market Outlook - Tuesday, Jan. 30.

"Asian markets saw a mixed trading session with the momentum from Wall St's record highs offset by weakness in China. The Nikkei 225 initially rose after a surprise drop in Japan's unemployment rate, but later gave up most of its gains. This evening, the Bank of Japan will release a summary of this month’s policy meeting, during which interest rates were left unchanged and remain in negative territory. However, in comments following the meeting, BOJ Governor Ueda appeared to suggest that rates could begin to rise starting from the spring. Consequently, today's summary will be closely scrutinized for indications of whether this is indeed a realistic possibility.Hang Seng and Shanghai Comp were under pressure as attention shifted to earnings releases, with Hong Kong experiencing losses in property and tech sectors. Additionally, the Hong Kong government initiated the process of passing new national security laws.

The upcoming Eurozone Q4 GDP data will give us an understanding of the level of economic activity at the end of 2023. If there is a further decline following the 0.1% decrease in Q3, it could signal a recession at the year-end. We predict that there will be no change in overall output for the region, narrowly avoiding meeting the technical definition of a recession (which requires at least two quarters of negative growth). However, certain member countries, particularly Germany, may see declines in their GDP. Given the recent update on monetary policy, it is expected that the European Central Bank will cut interest rates in April, and today's data is unlikely to change those expectations. Furthermore, we will also receive January's consumer and business confidence data for the Eurozone. The consumer confidence figure, which is a second reading, initially showed a decrease from December but remained higher than recent lows. It is anticipated that business confidence will show a more positive outlook for the services sector compared to the industrial sector, which is still under significant pressure.

Before the Bank of England's update on Thursday, today's readings on money supply and lending will provide insights into how past interest rate hikes have impacted the economy. Of particular interest will be the figures on lending in the housing market, as there are indications that recent decreases in market interest rates are benefiting this sector. Expect that mortgage approvals will increase for the third consecutive month in December, reaching their highest level in four months.

Stateside, a crucial measure of consumer confidence is expected to increase for the third consecutive month in January, reaching its highest level since last July. This likely reflects the impact of lower inflation rates and expectations of interest rate cuts."

Contributor Peter Boockvar notes GDP Stronger...But Why? And What Does It Mean?

"Personal spending added 190 bps, which was a bit better than expected and mostly led by spending on services. Government spending was the second biggest contributor, adding almost 60 bps, most of which was state and local spending. They are having to spend all the money they got from the Federal government via a few of the big programs legislated a few years ago.

Trade added 43 bps because of an almost 70 bps add via exports (in the face of a very mixed overseas demand picture), while imports took away 25 bps. Gross private investment contributed 40 bps with little add from residential investment and more from spending on “info processing” and “software.” Spending on “structures” (which can be a variety of things) added 10 bps. There was almost no contribution from inventories after the sharp Q3 build.

Real final sales grew by 3.2% quarter-over-quarter annualized and final sales to private domestic purchasers were up by 2.6%.

Adding seven-tenths to the headline GDP report was the price deflator, which came in at 1.5% instead of 2.2% as expected. If it was in line, real GDP would have printed 2.6%, closer to the estimate of 2%. By the way, the core personal consumption expenditures price index was as expected and what the Federal Reserve is looking at.

Bottom line? An in-line inflation deflator print would have put this figure at 2.6% versus the estimate of 2%. This number is going to get revised a few more times anyway and we’re already a month into Q1."

Well, it is a good thing for the country and the economy that we are starting to see some of the impact of the infrastructure funds hit the market...

TM contributor Mark Vickery reporting on Q4 earnings notes Markets Stroll Higher Ahead Of Key Data; SMCI, FFIV, WHR Beat.

"One sign that we’re in a resilient bull market presently is that we’ve strolled into a potentially thorny period of economic and earnings data with market levels up more than a week straight, and we keep climbing further into the green...

A sixth record closing high for the S&P 500 just this month/year alone ought to give a good impression of where the market’s collective head is at presently. The S&P gained +0.76% — led by all-time highs from Microsoft (MSFT), which reports fiscal Q2 earnings after tomorrow’s close — while the Nasdaq performed even better: +172 points, +1.12% on the day. The small-cap Russell 2000 won the day, +1.38%, while the blue-chip Dow brought up the rear, making +224 points for the session, +0.59%.

And the hits don’t stop there. Silicon Valley-based Super Micro (SMCI), after already having climbed +74% year to date and +59% from near-term lows on January 18th, outperformed recently raised guidance in its fiscal Q2 report released after today’s closing bell...

Cloud management network F5, Inc. (FFIV) also easily outpaces fiscal Q1 expectations on both top and bottom lines this afternoon, posting earnings of $3.43 per share for a 40-cent beat, on quarterly sales of $693 million, which bettered the $687 million analysts were expecting...

American appliances stalwart Whirlpool (WHR) also beat estimates in Q4 for both revenues and earnings after the closing bell today, notching earnings per share of $3.85 from $3.64 expected (still four cents below the year-ago’s $3.89 per share) on $5.09 billion in quarterly sales, which topped the $5.05 billion consensus estimate...

Tomorrow, we’ll see economic prints for Case-Shiller home prices, Job Openings and Labor Turnover Survey (JOLTS), and Consumer Confidence. We’ll see earnings for UPS (UPS) and Pfizer (PFE) ahead of Tuesday’s opening, Microsoft, and Alphabet (GOOGL) after its close."

The Staff at Read The Ticker give us chart photos of the 2024 Soft Landing Working It.

"Can it last? Can the US Gov keep the plates spinning until the US 2024 elections?"

Chart 1 - Gov debt holding up business activity.

Chart 2 - Gov doing all the hiring!

Chart 3 - ISM Services PMI holding up business, manufacturing recession continues (or going to Mexico)

That's a wrapful of good news.

Peace.

More By This Author:

Thoughts For Thursday: Indices Continue Climbing

Tuesday Talk: Spiking

Thoughts For Thursday: What Kind Of A Week Is This?

Comments

Log in or sign up to join the conversation.