Buoyed by remarks that the Fed will stick to its forecast of reducing interest rates during 2024, the stock market ran with the news and ended Wednesday's session on an upbeat note.

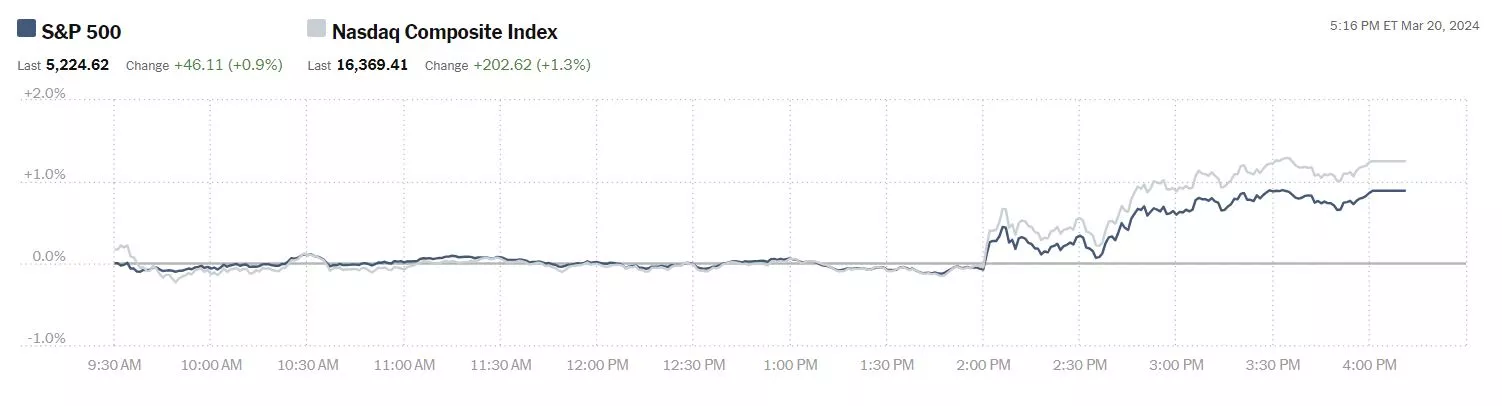

Yesterday the S&P 500 closed at 5,225, up 46 points, the Dow closed at 39,512, up 401 points and the Nasdaq Composite closed at 16,369, up 203 points.

Chart: The New York Times

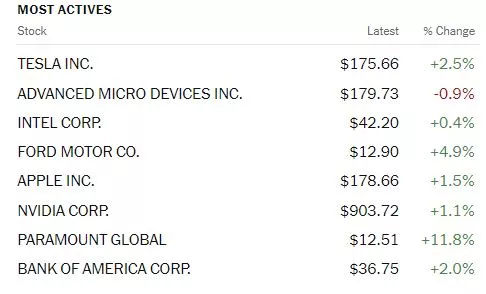

Most actives were led by Tesla (TSLA), up 2.5%, followed by Advanced Micro Devices (ADM), down 0.9%, and Intel Corporation (INTC), up 0.4%.

Chart: The New York Times

In morning futures trading S&P 500 market futures are up 28 points, Dow market futures are trading up 163 points, and Nasdaq 100 market futures are trading up 167 points.

TalkMarkets contributor Mish Schneider hedged her bets in her headline, FOMC - Dovish Or Hawkish Or A Bit Of Both?, but basically gave Chairman Powell a thumbs-up.

"The Fed kept rates unchanged and essentially suggested 3 rate cuts on the table for 2024.

Both the commodities and equities markets took that as a sigh of relief.

SPY made new all-time highs and gold and gold miners flew.

For 2025, the Fed sees the jobs rate as holding steady at 4.1%.

They see inflation dropping to 2.2% as measured by the PCE numbers.

And they see the Fed Funds rate dropping significantly by 2026 and in the longer run.

However, the Fed is committed to a 2% inflation rate.

And the most interesting part - Powell said that there could be seasonal effects in inflation data.

Sounds like many words to say the one word- “transitory”.

Powell is watching the labor market and will become more dovish if the unemployment rate rises.

He feels confident that the policy rate has peaked.

But also wants us to understand that “higher for longer” is not off the table.

Some analysts took the minutes as a more hawkish Fed, while the initial market reaction interpreted the meeting as dovish.

Powell did a great job pandering to both doves and hawks...

Are we readying for a “no landing” where everything runs up and inflation remains in control.

Or did the Fed just relay they want lower rates to pay off the ginormous debt in favor of worrying about the hyperinflation potential?"

Contributor Mark Vickery writes FOMC, Powell Give Investors The Warm Fuzzies.

"Markets enjoyed a bullish day of trading today, pushing higher from flat levels upon the latest output from the Federal Open Market Committee (FOMC) at 2pm ET. The Fed’s “dot-plot” still allows for three 25 basis-point (bps) cuts in 2024, likely to start — but not committed to — at the June meeting. Markets jumped on the news, finishing at or near session highs on the Dow (+401 points, +1.03%), S&P 500 (+0.89%, notching a new all-time record close) and the Nasdaq (+202 points, +1.25%). The small-cap Russell 2000 drooped into the closing bell, but was still up +1.92% on the day.

This marks the fifth-straight Fed meeting where no move on interest rates was taken. We remain at 5.25-5.50% — the “higher for longer” Fed Chair Jerome Powell had been advertising since the Fed began making moves higher two years ago — which is the highest we’ve seen interest rates since 2001. In his press conference following the FOMC release, Powell said the monetary policy body now has “greater confidence” that inflation is coming down to 2%.

Three rate cuts in 2024 would take us down to the range of 4.50-4.75% on the Fed funds rate, which would have an effect on mortgage rates coming down and other rate-sensitive data. Powell was less forthcoming when presented with hypothetical scenarios about what should happen if inflation remains higher deeper into the year. “We’re committed to getting to a 2% inflation rate over time,” became his answer to a few questions posed during the press conference.

In the FOMC statement, the Fed did remove one rate cut in its dot-plot for 2025, bringing that total down from four to three downward moves. For 2026, the Fed still sees four cuts. Overall, the year-end interest rate levels from Fed participants is now +4.6% for 2024, +3.9% in 2025 and +3.1% in 2026. You’ll note that none of these figures carry a “two-handle.” This suggests the fight against inflation is expected to continue over the medium-term, at least as of current data today...

Finally, Powell also gave little to no expression of concern to the labor market, citing weekly jobless claims numbers coming down in recent months, and jobs totals remaining fairly healthy on monthly employment reports. Wage increases had been strong, Powell said, “but are gradually coming down to sustainable levels.” While allowing that “unexpected things” can happen, Powell suggests the FOMC will “stay… essentially the same.” Good enough for today’s market."

TM contributor Stephen Innes opines Just What Dr Markets Ordered: An Uneventful FOMC.

"In milestone-setting fashion, the S&P 500 surged past the 5,200 mark on speculation that the conclusion of the most aggressive Federal Reserve hiking cycle in a generation will continue to bolster Corporate America's Profit Margin. Notably, the gains were widespread, with laggards in catch-up mode as traders now perceive higher chances of an initial rate cut occurring in June.

Despite the recent uptick in inflation, Fed officials maintained their projection for three rate cuts this year and indicated a shift towards slowing the pace of reducing their bond holdings. This suggests that officials interpret seasonal factors driving this year’s inflationary pressures. While Jerome Powell reiterated the Fed's desire to see more evidence of price decreases, he also noted that it would be appropriate to begin easing policy "at some point this year.”

While the economic projections released after the meeting appeared slightly more hawkish than those from December, the adjustments were not overly alarming as both investors and the Fed still generally agreed on the “right” amount of marginal easing for this year.

Indeed, this scenario likely results in the Federal Reserve implementing its first quarter-point cut at the June meeting, followed by cuts at every other meeting over the remainder of the year.

So, the absence of any particularly hawkish news provided a green light for the market to continue its upward trajectory. And why not as a sturdy economy plus rate cuts are the best possible scenario, and it’s fair to suggest that it’s now the consensus.

The main concern is that inflation might take longer to reach the Fed's 2% target. This could happen if services inflation remains stubbornly high and slow to decline or demand for goods rebounds, leading to higher prices. However, rather than resorting to any policy pivot, the central bank will delay rate cuts in response to this dynamic."

Contributor Haresh Menghani looks at the action in gold in response to the FOMC announcements, Gold Price Sticks To Gains Above $2,200 Mark, Bulls Take A Brief Pause Amid Risk-On.

"Gold price (XAU) retreats from a fresh record high touched earlier this Thursday, albeit manages to hold its neck above the $2,200 mark heading into the European session. The Federal Reserve (Fed) on Wednesday projected a 75 basis point rate cut by end-2024, keeping the US Dollar (USD) depressed near a one-week trough and pushing the non-yielding yellow metal higher for the second straight day. That said, elevated US Treasury bond yields help limit the downside for the Greenback.

Apart from this, the prevalent risk-on environment – as depicted by an extension of the recent bullish run across the global equity markets – caps the upside for the safe-haven Gold price amid slightly overbought conditions on the daily chart...

From a technical perspective, the overnight strong positive move confirmed a breakout through a bullish flag chart pattern and validated the positive outlook for the Gold price. That said, the Relative Strength Index (RSI) has moved back above the 70 mark, making it prudent to wait for some near-term consolidation or a modest pullback before traders start positioning for any further appreciating move."

Looking at commodities, TalkMarkets contributors Warren Patterson and Ewa Manthey find that the Oil Rally Runs Out Of Steam.

"The rally in oil has started to fade with the market in overbought territory and little in the way of a fresh catalyst to keep the upward momentum going. ICE Brent settled a little more than 1.6% lower on the day - the largest daily decline in almost a month, leading to Brent (BNO) closing just below US$86/bbl. The market has recouped some of these losses in early morning trading today. The Fed’s decision to leave policy rates unchanged at its meeting yesterday was no surprise. And while the Fed maintained a forecast for three cuts this year, it lowered its forecast from four to three cuts for 2025. The prospect of rates staying higher for longer should provide some headwinds to risk assets, including oil. That said, looking at broader price action (gold, equities, USD and treasuries) following yesterday’s meeting, the market appears to be more focused on what the Fed may do this year.

The EIA’s weekly inventory report contained little in the way of surprises, showing US commercial crude oil inventories falling by 1.95m barrels over the week, which was similar to what the API reported the day before. While refiners increased utilisation rates by 1pp over the week, the draw was predominantly driven by stronger crude exports, which grew by 1.73m b/d WoW to 4.88m b/d. This left US net exports of crude and products at 4.05m b/d over the week - the highest level since November last year and only the second time that net exports have crossed the 4m b/d barrier.

For refined products, distillate stocks were little changed, increasing by just 624k barrels. However, gasoline inventories fell by 3.31m barrels, which is the seventh consecutive week of decline, leaving US gasoline inventories at just under 231m barrels - 2.1% below the 5-year average. The fall in US gasoline inventories in recent weeks has boosted gasoline, and the RBOB crack is now trading above US$30/bbl, up from around US$15/bbl at the beginning of the year. Gasoline cracks will remain well supported as we head into the summer driving season.

BP’s Whiting refinery has ramped up operations to nearly maximum rates following an outage after a power loss in February. It is believed that the refinery is operating near its nameplate capacity of around 435k b/d. Canadian heavy crude is a key feedstock for the refinery and its return should provide some support to the WCS differential, which has already strengthened considerably since mid-February.

US LNG exporter, Freeport LNG, said that it will increase LNG production following ongoing repairs that are scheduled to be completed by early May. This maintenance is estimated to increase the facility’s capacity to 16.5mt/year, up from the current capacity of 15mt/year. The three-train plant has been undergoing maintenance since late January due to damage from freezing weather conditions earlier in the year. Feedgas to the terminal suggests that only one train is currently online."

That's a wrap for today.

Onwards, markets!

Have a good one.

Peace.

More By This Author:

Tuesday Talk: Still Talk Of The Town - Inflation

Thoughts For Thursday: 5,000 And Beyond

Thoughts For Thursday: Traders Have A Short Term Grail Quest

Comments

Log in or sign up to join the conversation.