Inflation doesn't seem to be moving higher, but its downward trajectory seems to have slowed to a crawl, around 3.2%, which is keeping interest rates higher than anticipated, but also keeping the brakes on runaway inflation.

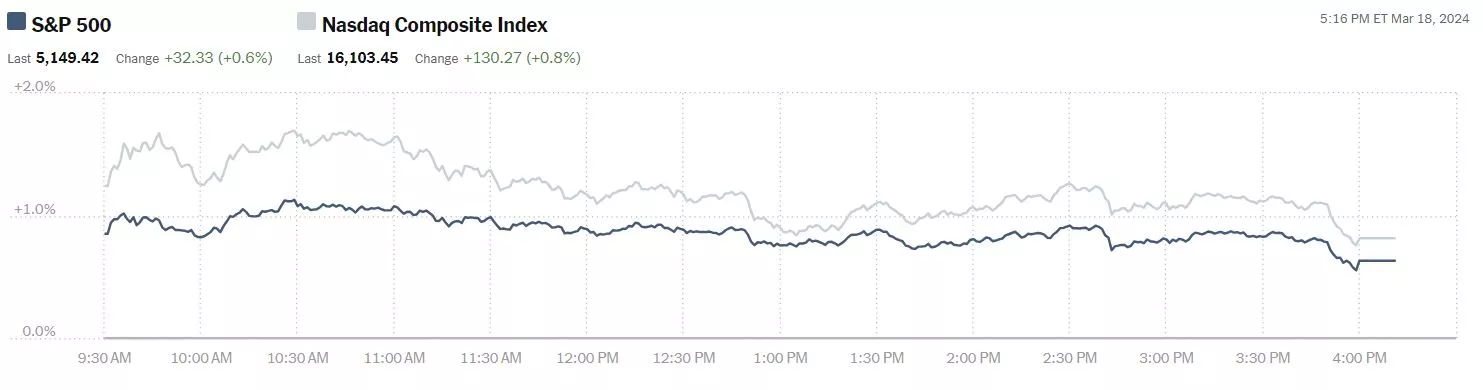

On Monday the S&P 500 closed at 5,149, up 32 points, the Dow closed at 38,790, up 76 points and the Nasdaq Composite closed up 130 points.

In options trading currently, S&P 500 market options are down 21 points, Dow market options are down 84 points and Nasdaq 100 options are down 104 points.

Chart: The New York Times

Most actives on Monday were Tesla, up 6.3%, followed by Apple (AAPL), up 0.6% and Alphabet (GOOGL), up 4.6%.

Chart: The New York Times

TM contributor Patrick Munnelly in his Daily Market Outlook - Tuesday, March 19 notes:

"Despite positive cues from Wall Street overnight, Asian stock markets are predominantly lower on Tuesday as traders adopt a cautious stance after monetary policy announcements from the Reserve Bank of Australia and the Bank of Japan. Additionally, anticipation surrounds the US Fed's monetary policy announcement on Wednesday, with investors keen for insights into the outlook for interest rates. Although Asian markets closed mostly higher on Monday, ongoing uncertainty prevails in the current session. The Fed is widely anticipated to maintain interest rates unchanged following recent inflation readings that have tempered optimism regarding a rate cut in June. However, market attention will be directed towards the central bank's accompanying statements and economic projections, which hold the potential to significantly influence rate expectations. Looking ahead, the Bank of England and the Swiss National Bank are also scheduled to announce their monetary policy decisions later in the week, adding to the market's anticipation and volatility.

The Bank of Japan (BoJ) has increased its interest rates for the first time in almost 20 years, making it the last central bank in the world to end negative rates as indications of strengthening inflation emerge..."

Contributor Stephen Innes notes US Stocks Rally Into Higher Yield Headwinds.

"Despite facing headwinds from higher US yields, Wall Street's main indexes made gains on Monday. Mega-cap growth stocks, including Alphabet (GOOG) and Tesla (TSLA), supported the rebound, which helped lift the technology-heavy Nasdaq.

Investors are currently focusing on the Federal Reserve's upcoming meeting, where they hope that the Fed will successfully thread the needle through a mixed bag of data and keep the rally rolling. Still, traders are grappling with a competing narrative. On one hand, there is enthusiasm surrounding the potential of artificial intelligence (AI) and its impact on the technology sector. On the other, there is palpable apprehension ahead of the Federal Reserve's statement and commentary expected on Wednesday. This balancing act reflects the broader uncertainty as investors weigh the bullish impulse from the transformative potential of AI against the backdrop of evolving monetary policy and its implications for asset prices.

The crux of the matter lies in the Federal Reserve's assessment of recent inflation overshoots in January and February. If the Fed interprets these overshoots as indicative of a rekindled price growth impulse, it may adjust its projections accordingly. This could result in the new dot plot reflecting only two rate cuts in 2024. Conversely, if the Fed views the inflation overshoots as seasonal, the dot plot might still show three rate cuts

The market reaction hinges on this distinction. If the dot plot indicates two rate cuts, stocks will flinch...

There's no denying the significance of the dot plot's implications, and it’s a squeaker. A closer look at the dispersion of the dots reveals that just two participants shifting from projecting three cuts to two would be sufficient for the median dot to move to a total of two cuts for the year.

This scenario poses the main downside risk for stocks, as it could further encourage the US rate market to scale back expectations for Federal Reserve rate cuts. Any indication from the FOMC meeting that supports a less dovish stance than previously anticipated could lead to a reassessment of rate cut expectations, sending yields soaring and stocks tanking."

Contributor Ironman says U.S. Recession Probability Nears A Double-Top.

"The odds the U.S. economy will see a recession start at some time in the next twelve months continued to rise during the past six weeks. Since our previous update, that probability has risen a couple of notches to just over 76%. This resurgence began after the recession probability bottomed at 67% at the end of November 2023 after having previously peaked at 81% in July 2023. The rebound in the odds of recession is nearing what might be described as a double top.

These probabilities are based on a recession forecasting method developed for the Federal Reserve Board in 2006. As such, they reflect the kind of real data that Federal Reserve officials will be weighing as they meet from 19-20 March 2024 to discuss how they will be setting short-term interest rates in the United States.

The prospect for a recession has ticked up since bottoming largely because the inversion of the U.S. Treasury curve deepened since December 2023, with longer-term interest rates falling further below the level of short-term rates. That change has coincided with reports of higher-than-expected inflation prompting Fed officials to delay the beginning of expected interest rate cuts by at least three months.

The following chart presents the latest update of the Recession Probability Track, capturing how that probability appears going into the Federal Reserve's second two-day meeting of 2024. The Fed's Federal Open Market Committee is expected to continue holding the Federal Funds Rate steady at this meeting.

The Recession Probability Track indicates the probability a recession will someday be officially determined to have begun sometime in the next 12 months. For this update, that applies to the dates between 18 March 2024 and 18 March 2025."

Bitcoin which seems to be having a resurgence of late, is still a hot asset to handle. TalkMarkets contributor James Harte has the latest Bitcoin Commentary - Tuesday, March 19.

"The Bitcoin rout continues to deepen on Tuesday with BTC futures now down around 14% from the YTD highs. Following the breakout to fresh record highs last week, BTC has come under sustained selling pressure with futures currently on track to record their fourth consecutive losing day. There has been plenty of chatter recently around whether the current run up in Bitcoin constitutes a bubble, with many commentators warning of an impending crash...

The sell off has many questioning whether the BTC rally is over and if a 2021/2022 style sell-off is coming? Looking ahead, there are still plenty of reasons to remain bullish on BTC...

Looking ahead this week, the focus will be on the FOMC tomorrow with the current pullback likely reflecting some profit taking and position adjustment ahead of the event. Put simply, BTC bulls need to hear the Fed signaling expected easing in coming months which should weaken USD and drive risk assets higher. If we hear further pushback from the Fed this is likely to dampen BTC further near-term...

The failure at 74325 has seen the market breaking down below the bull channel lows and back under the 69355 level. Price is now testing the 64540 support and with momentum studies bearish, risks of a downside break are growing. If we do turn lower, 60275 will be next support to note."

_638464419907544456.webp)

Closing out the column for today we have some suggestions in the "Where To Invest Department" from contributor Shaun Pruitt who writes Time To Buy These Top-Rated Basic Materials Stocks Amid An Uptick In Inflationary Data.

"Markets have remained resilient despite February’s CPI and PPI data coming in hotter than anticipated but it may be time to consider buying several highly ranked basic materials stocks and here are a few to consider.

Balchem (BCPC - Free Report)

Boasting a Zacks Rank #1 (Strong Buy) Balchem Corporation provides solutions and products for a variety of industries including specialty-packed chemicals for healthcare and agricultural markets along with derivatives for use in industrial applications.

Balchem’s top and bottom line expansion is intriguing with total sales projected to rise 6% this year and pop another 5% in fiscal 2025 to $1.03 billion. More impressive, annual earnings are forecasted to soar 23% in FY24 and jump another 12% next year to $4.64 per share. Furthermore, Balchem’s stock is up +23% in the last year and there could be more upside ahead as FY24 earnings estimate revisions have climbed 14% over the last 60 days with FY25 EPS estimates soaring 18%.

Hawkins (HWKN - Free Report)

Substantial growth prospects are reason to consider Hawkins’ stock which sports a Zacks Rank #2 (Buy). Hawkins distributes special chemicals and ingredients used in water treatment along with health and nutrition products.

Most enticing is that Hawkins’ EPS is expected to leap 26% in FY24 to $3.61 versus $2.86 a share last year. Plus, FY25 EPS is expected to rise another 1%. Total sales are projected to dip -2% in FY24 but rebound and jump 8% in FY25 to $984.42 million.

Notably, Hawkins’ stock has soared +81% over the last year and has continued to rally with the company now surpassing earnings expectations for nine consecutive quarters.

L.B. Foster (FSTR - Free Report)

Also sporting a Zacks Rank #2 (Buy) is L.B. Foster, a distributor of rail and trackwork, piling, highway, and tubular products. Trading just under $25, L.B. Foster’s stock has skyrocketed over +100% in the last year.

Correlating with its stellar price performance, annual earnings are forecasted to catapult to $1.07 per share in FY24 compared to $0.13 a share in 2023. Even better, FY25 earnings are expected to climb another 52% to $1.63 per share.

L.B. Foster’s stock trades at 22X forward earnings and just 0.48X sales with its top line expected to dip -1% this year but rebound and rise 7% in FY25 to $577.93 million."

As always, caveat emptor.

Have a good one.

Peace.

More By This Author:

Thoughts For Thursday: 5,000 And Beyond

Thoughts For Thursday: Traders Have A Short Term Grail Quest

Tuesday Talk: A Good Month - Two Days To Go

Comments

Log in or sign up to join the conversation.