Meta and Google recently borrowed a combined $55 billion in the corporate bond market. As we share below, this debt represents a new source of funding for data center expansion. Further, as shown in orange, Oracle tapped the private market for loans to secure the capital needed to sustain AI innovation and the related data center buildout. The graph below shows that borrowing for data centers surged this year, more than three times the amounts in the prior couple of years.

It appears that cash flow and earnings from the hyperscalers are no longer enough to fuel data center growth. Some estimate that the global data center infrastructure buildout could be over $5 trillion, possibly even $7 trillion. This year, the hyperscalers are expected to generate approximately $700 billion in annual operating cash flow, of which about $500 billion has been invested in AI data centers. While a massive investment, the graph below shows it’s not sufficient. The high credit ratings and strong fundamentals of some hyperscalers should allow them to continue issuing debt and using cash flows to meet their investment needs. These companies include Amazon, Microsoft, Google, and Meta. Others may not be so fortunate.

For instance, Oracle, which has negative cash flows and a debt-to-EBITDA ratio of over 4x, borrowed $38 billion in October for data center construction. This loan allows the BBB-rated company to avoid the more turbulent corporate bond market. Regardless of whether they borrow in the public or private markets, the market is noticing. Their credit default swap spreads have doubled this year to 88bps. While the market assigns only a slight chance of default, the trend warrants note. It signals that Oracle’s financial wherewithal to fund data center expansion may hinder its opportunities relative to its larger competitors.

What To Watch Today

Earnings

Economy

- No notable releases today

Market Trading Update

Yesterday, we touched on the dollar and bonds, which continue to show improvement. Interestingly, the last few days have also shown some progress in the “rest of the market” outside of the “Mag 7.” This is a note we previously discussed, using data from SimpleVisor.com, which focused on the market’s relative and absolute performance.

“Secondly, there has been a significant lag in performance between the Equal Weight and Market Cap-weighted index. Again, this is a breadth issue, confirming that a handful of stocks, the most heavily weighted, are driving the index higher. Over the last 6 months, there has been a 12% gap in performance between the two indices. We see the same performance gap when examining the absolute and relative performance of the various market factors. MGK (Mega-cap growth) is grossly overbought, while SPLV (Low-Beta, Low Volatility) stocks are grossly oversold. Such suggests that eventually the market is going to rotate, and given the current deviation in performance, that rotation could be quite volatile.”

That was October 30th.

Here is that same analysis just two weeks later.

In just the last two weeks, Momentum, MegaCap, and Retail Favorites (ARKK) have reversed sharply in terms of relative performance. That rotation is not surprising, as those sectors were previously aggressively overbought, so the reversal to relieve those overbought conditions was unsurprising.

With the Government shutdown set to conclude next Wednesday, this will release a lot of liquidity back into the market, along with buybacks, which will continue to support the current rally into year-end. However, I would expect any rally to be somewhat volatile as markets continue to digest risk. With the Equal Weight Index showing improvement, I would continue to maintain some defensive exposure to offset near-term concern risk with the Megacap stocks.

Trade accordingly.

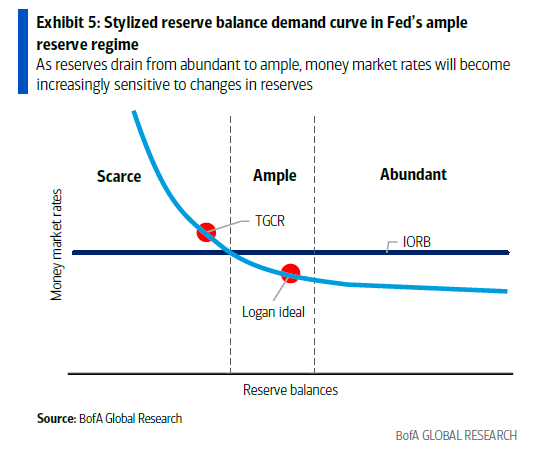

QE Is Coming: The 2008 Roots Of Fed Dominance

Here we go again. The overnight funding markets are showing signs of stress, and the scent of QE is in the air.

Per New York Fed President John Williams:

Based on recent sustained repo market pressures and other growing signs of reserves moving from abundant to ample, I expect that it will not be long before we reach ample reserves. When that happens, it will then be time to begin the process of gradual purchases of assets.

The question everyone should be asking is: why have the capital markets become so reliant on the Fed’s liquidity? The answer goes back to the 2008 financial crisis.

Before 2008, the private market, not the Fed, was the primary source of liquidity. The Fed was rarely called upon to support liquidity. Since then, the Fed has seemingly constantly tinkered with its policy to manage liquidity. As some correctly say, the Fed has shifted from lender of last resort to the lender of only resort!

More On QE

If you have read our article linked above, we urge you to consider the following quote from New York Fed President John Williams (h/t ZeroHedge):

Looking forward, the next step in our balance sheet strategy will be to assess when the level of reserves has reached ample. It will then be time to begin the process of gradual purchases of assets that will maintain an ample level of reserves as the Fed’s other liabilities grow and underlying demand for reserves increases over time. Such reserve management purchases will represent the natural next stage of the implementation of the FOMC’s ample reserves strategy and in no way represent a change in the underlying stance of monetary policy.

Determining when we are at ample reserves is an inexact science. I am closely monitoring a variety of market indicators related to the fed funds market, repo market, and payments to help assess the state of reserve demand conditions. Based on recent sustained repo market pressures and other growing signs of reserves moving from abundant to ample, I expect that it will not be long before we reach ample reserves.

Tweet of the Day

More By This Author:

50 Year Mortgages: Pros And ConsAn Economic Data Flood Is Coming: Does It Matter?

Forward Return And The Importance Of Math

Comments

Log in or sign up to join the conversation.