Here we go again. The overnight funding markets are showing signs of stress, and the scent of QE is in the air.

Per New York Fed President John Williams:

Based on recent sustained repo market pressures and other growing signs of reserves moving from abundant to ample, I expect that it will not be long before we reach ample reserves. When that happens, it will then be time to begin the process of gradual purchases of assets.

The question everyone should be asking is: why have the capital markets become so reliant on the Fed’s liquidity? The answer goes back to the 2008 financial crisis.

Before 2008, the private market, not the Fed, was the primary source of liquidity. The Fed was rarely called upon to support liquidity. Since then, the Fed has seemingly constantly tinkered with its policy to manage liquidity. As some correctly say, the Fed has shifted from lender of last resort to the lender of only resort!

Considering the significant impact liquidity has across all asset classes, it’s essential to appreciate this relatively new dynamic and understand why the Fed, rather than the private market, has become the primary liquidity manager of the financial system. Consequently, Fed policy, not free markets, now plays a crucial role in forecasting how today’s speculative excesses might return to their normal levels. Will it be a pop, a slow leak, or will the Fed keep bubbles afloat at any cost?

The New Fed Era

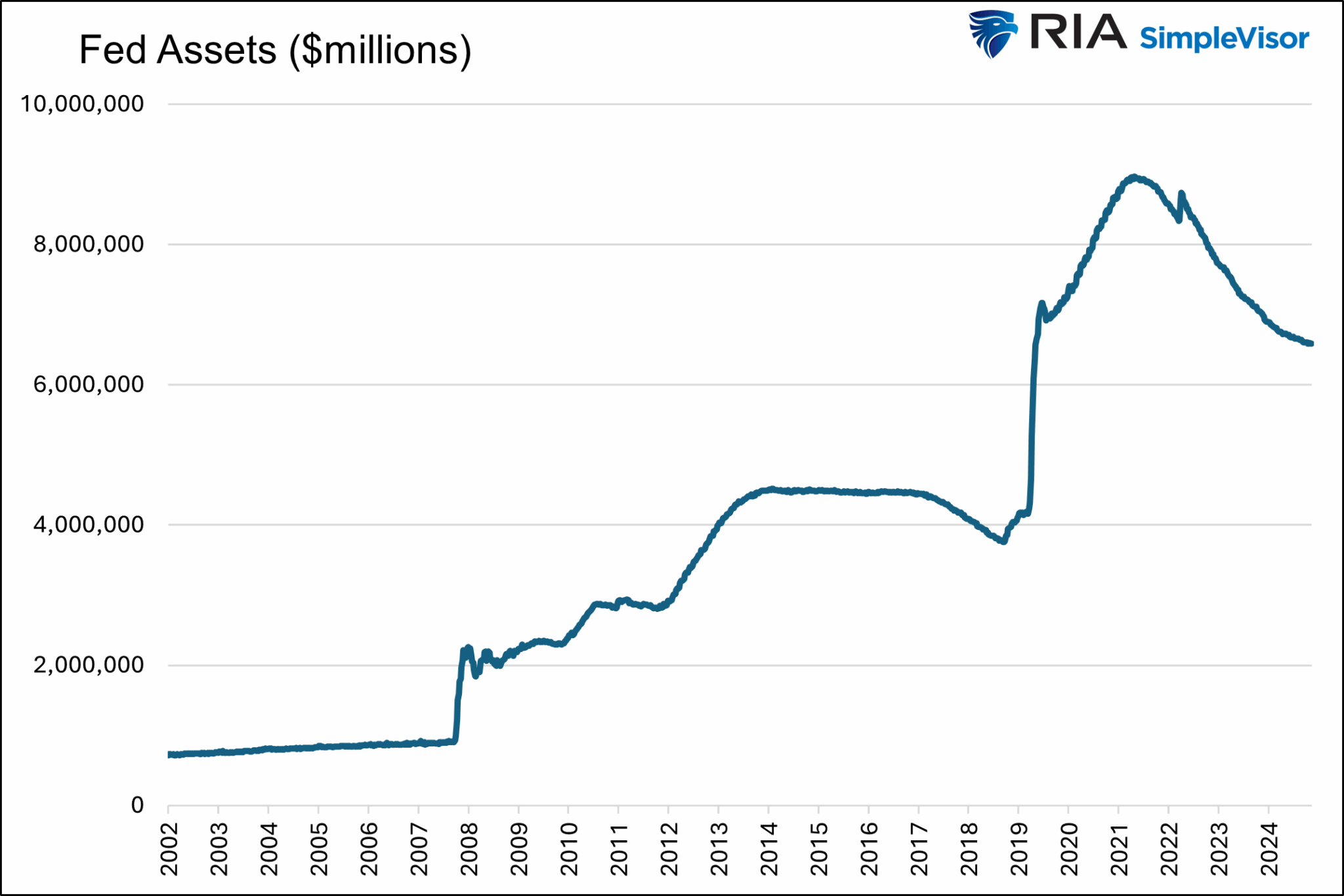

Before explaining how Fed policy has evolved since the financial crisis, we want to highlight two charts that illustrate the difference in Fed policies before and after 2008.

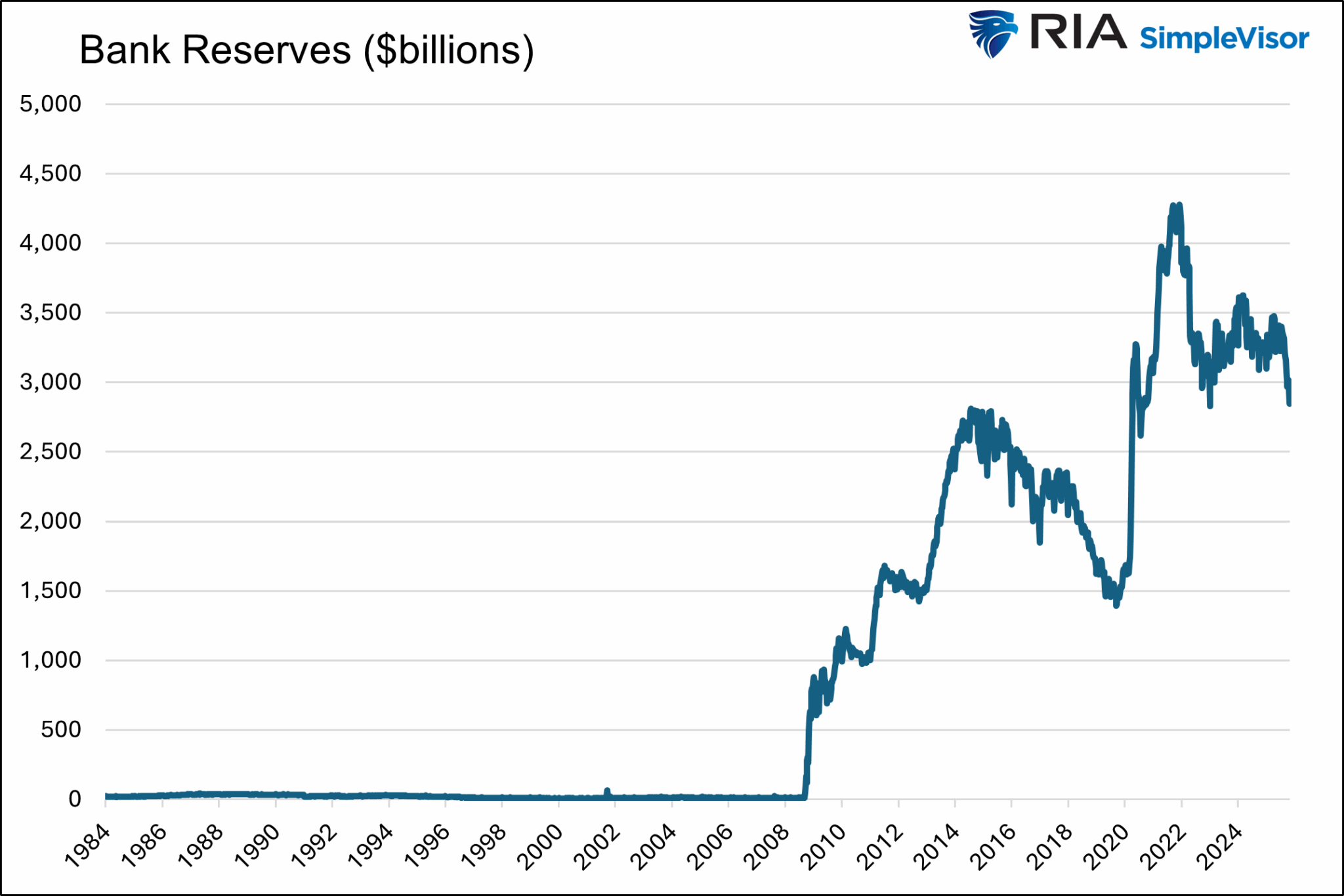

The first graph below charts the size of the Fed’s balance sheet since 2002. Before 2008, the Fed’s assets were growing at a slow and steady 4% pace. Not surprisingly, the 4% growth was roughly in line with economic growth. After 2008, the amount of its assets surged, and the volatility of its holdings increased significantly. The second graph, showing bank reserves held at the Fed, tells a similar story —calm before the crisis, followed by growth and volatility after the crisis.

Clearly, something changed in 2008. Let’s explore what that is, and in doing so, we can better appreciate the Fed’s expanded role and why its policies have become much more closely integrated with the gyrations of financial markets.

Managing Via Reserves Not Fed Funds (Post-QE World)

Before 2008, banks held minimal excess reserves. Instead, they mainly met their liquidity needs by lending and borrowing reserves with other banks. Many of these transactions took place in the overnight Fed Funds market. The Fed did not set the Fed Funds rate back then, nor does it now. However, before the financial crisis, it guided banks toward its target rate through daily purchases and sales of Treasury securities.

In 2008, the Fed introduced Quantitative Easing (QE). QE entails consistently purchasing securities regardless of liquidity conditions. Before QE, buying or selling was based on daily liquidity conditions. Because the Fed buys assets from banks with reserves, total reserves in the banking system have been grossly elevated since 2008.

The impact of QE on the financial markets and economy is two-fold.

- First, the Fed removes securities from the market, allowing the liquidity in those securities to flow to other assets.

- Second, the new reserves on bank balance sheets can be used to support loan growth. The more reserves the banks hold, the more liquidity they can provide. We say “can” because the bank still must be willing and able to provide liquidity.

Today, to maintain control of the overnight financing markets, the Fed pays interest on reserve balances (IORB). The Fed sets the IORB rate, which serves as a floor for the Fed Funds rate because banks will not lend their reserves for less than they can earn risk-free from the Fed.

Thus, in the post-QE world, the level of bank reserves and the Fed’s IORB rate are predominant determinants of overnight liquidity. The graph below shows the stark increase and volatility in reserve balances following the first round of QE in 2008.

Regulations Changed The Overnight Markets

Before 2008, the private sector repo markets were the core plumbing of the short-term funding markets. Fed Funds is unsecured lending between banks, whereas repo is secured (collateralized) funding between all financial institutions. It is estimated that the daily volume of repo transactions was over $10 trillion before the crisis. Money market funds and other large holders of cash would invest their cash balances in repo; thus, private firms provided the capital markets with a steady, dependable stream of liquidity.

Following the near collapse of the entire banking system in 2008, the government and global banking regulatory agencies enacted a series of regulations that made it more expensive for banks and funds to lend short-term cash. Let’s review a few of those that have changed the liquidity landscape.

Basel III (global banking regulations)

Basel III is a set of global banking regulations written by the Basel Committee on Banking Supervision. The Committee is effectively a consortium of the world’s central bankers. While Basel has no legal jurisdiction over US banks, its rules are often fully approved and implemented by the Fed, FDIC, and OCC. In 2013, the Fed finalized Basel III capital rules. Within those rules, the following two changes had significant impacts, limiting and disincentivizing those who could provide the market liquidity.

Liquidity Coverage Ratio (LCR): Banks must hold 30 days of “high-quality liquid assets” (HQLA) to survive outflows. Repo lending counts as an outflow and is penalized. This rule critically disincentivized bank lending in the repo markets.

Supplementary Leverage Ratio (SLR): The rule implements capital charges against all assets, including risk-free US Treasuries and repos. Prior to SLR, there was effectively a zero-capital charge for Treasuries and Repo. Therefore, because repo provides no risk-weighted benefit to meet capital requirements, banks have significantly shrunk their repo books since the SLR became effective.

A report from the New York Fed – Market-Function Asset Purchases, underscores that the SLR has been a key factor limiting dealer repo volumes, especially in liquidity-stressed markets.

Due to SLR and LCR, the liquidity-shock-absorbing role has shifted from private dealers to the Fed.

Proprietary Trading Rules

The post-crisis Volcker rules banned banks from proprietary (prop) trading. Prop trading is when banks trade and manage their own assets. Before 2008, dealer prop desks would absorb cheap securities in stressed markets and provide the market with the liquidity it demanded when overnight rates were abnormally high. After the Volcker Rule took effect, this source of private market liquidity shrank. Per New York Fed data, dealer net repo transactions went from approximately $5.5 trillion to less than half of that today.

Money Market Reforms

Prime money market funds, unlike government money market funds, invest in government securities, as well as corporate and bank securities. Accordingly, they can offer higher yields than government funds, but they also entail a small degree of risk.

The risk of a loss in prime funds never materialized until September 16, 2008. At that time, the Reserve Primary Money Market Fund “broke the buck.” In other words, its net asset value fell below $1.00 or 100% of the shareholders’ money.

To differentiate prime money market funds from government money market funds, the SEC changed the landscape for prime funds. Now, prime funds can stop or slow redemptions if necessary and/or charge redemption fees in times of stress. The SEC also required funds to float their NAVs, essentially telling the public that full repayment of their investment is not guaranteed.

Given that money market funds are considered by many to be a cash equivalent, few money market fund holders had an appetite for risk. Accordingly, the use of prime funds collapsed. Much of the capital within those funds, provided liquidity to the private markets, shifted to government funds that mostly park money at the Fed or in Treasury securities rather than lend privately.

Pick Your Poison- Fed Or Free Market

Before 2008, when free markets largely determined liquidity conditions, speculative bubbles would form and eventually burst when liquidity was no longer sufficient to support highly speculative valuations and high leverage.

Today, those same bubbles form. However, with the Fed at the helm of liquidity, how and when those bubbles burst is not entirely clear. For example, while the Fed is not likely thrilled with the current extreme valuations, it also recognizes that a normalization of valuations and a broad de-risking event could cause economic hardship and potentially harm to the banking system. It will not sign up to preside over that.

Is the Fed capable of letting a bubble slowly leak? Given that this post-pandemic bubble is our first experience under the new Fed regime, we will have to wait and see.

Summary

Knowingly or unknowingly, post-financial crisis rules and regulations have kneecapped many of the old private-market liquidity providers. Without their capital and balance sheets, the Fed has become the primary source of market liquidity. To wit, consider the following quote from Jerome Powell in 2021:

In a stress scenario today, the Federal Reserve is the only entity with the balance sheet to absorb the shock.

While there is limited experience with the new monetary regime, we have learned that the Fed doesn’t have a straightforward way to assess liquidity conditions. For instance, the Fed was caught off guard in 2019 when overnight funding markets froze amid a liquidity squeeze. Conversely, in 2020 and 2021, in reaction to the pandemic, the Fed grossly oversupplied the markets with liquidity. In fact, it had to create the overnight reverse repurchase program to remove the excess reserves from the market. QT was also enacted to help.

As we share below, those excess reserves are now gone, and not surprisingly, liquidity stress is occurring.

In our view, QE or another policy move to increase bank reserves is imminent. The alternative is a deleveraging event, which would cause economic and financial market chaos.

More By This Author:

Nvidia Deals: Round Tripping Or Vendor Financing?CAPE Valuations: Does Nvidia Overstate Its Ominous Warning?

Dollar Debasement: Reality Or A Dangerous Narrative?

Comments

Log in or sign up to join the conversation.