Compiling a bunch of labor market data, we have the following picture of the private nonfarm labor sector, which seems to run counter to the argument last made a month ago that a recession occurred in 2022H1.

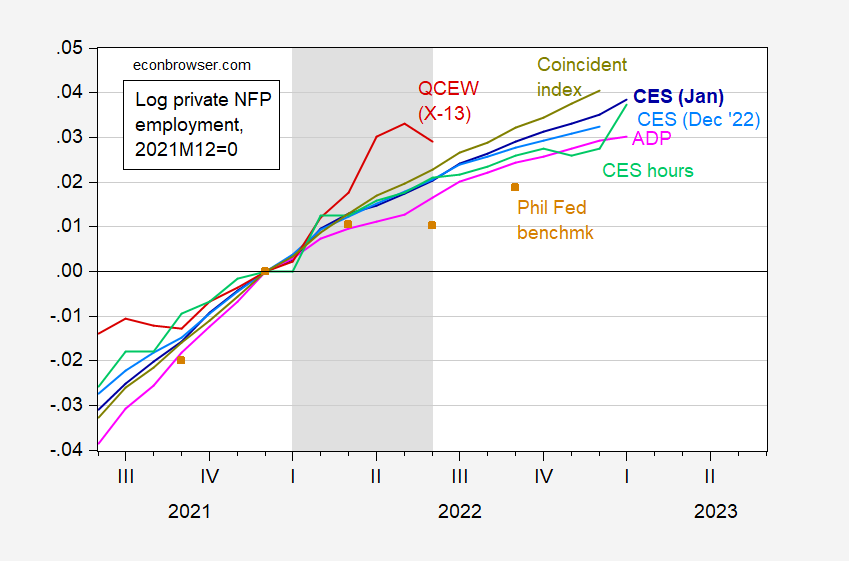

Figure 1: Private nonfarm payroll employment from January 2023 CES release incorporating benchmark revisions (blue), from December 2022 CES release (sky blue), ADP (pink), CES aggregate weekly hours for production and nonsupervisory workers (light green), QCEW private covered workers, seasonally adjusted using log transformed Census X-13 (red), Philadelphia Fed preliminary benchmark minus reported government employment (tan squares), Philadelphia Fed coincident index (chartreuse), all seasonally adjusted, in logs 2022M12=0. A hypothesized recession shaded light gray. Source: BLS (various) via FRED, BLS QCEW, Philadelphia Fed via FRED, and author’s calculations.

Note: January 2023 CES private NFP incorporates benchmark revision to data incorporating March 2023 QCEW data, and new seasonal factors. QCEW is a census which has almost complete coverage, reported up to June 2022 (but will be revised), but has to be seasonally adjusted to make it comparable to the other series. The aggregate weekly hours variable is not independent source from the other CES survey data based estimates — it will in principle equal employment times average weekly hours. The ADP series is based on completely different data than the BLS series. The Philadelphia Fed has a benchmarking process which accesses some of the BLS data but not all, in order to make a more timely estimate. Finally the Philadelphia Fed coincident index uses the Stock-Watson dynamic factor approach to applied to primarily labor market data (including wage and salary disbursements) to infer the level of economic activity.

More By This Author:

The Employment Release And Business Cycle Indicators - Friday, Feb. 3

The Cyclically Adjusted Budget Balance And Federal Debt Held By The Public: Time Series

Recession Probabilities Incorporating Foreign Term Spreads

Comments

Log in or sign up to join the conversation.