Image Source: Unsplash

The outlook for the chemicals industry in the Netherlands may have started to clear up, but patience is set to be tested for producers in 2024. While a robust recovery isn't quite underway yet, the renewed build-up of industrial stocks will provide some first green shoots.

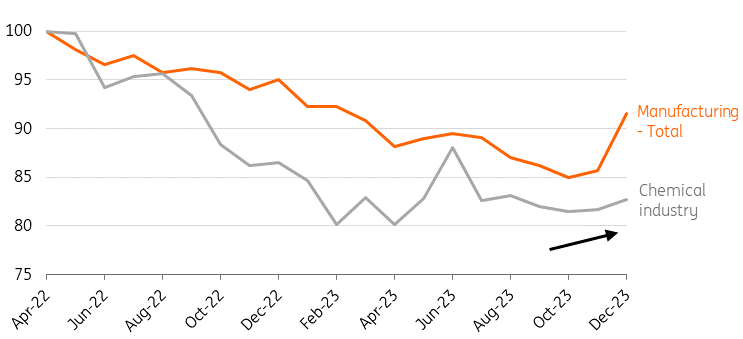

Chemical production stabilised at a very low level in 2023

Just like in 2022, 2023 was a turbulent year for the chemical industry in the Netherlands. Production did not fall any further month-on-month – but there was no recovery either. Production grew slightly in the second quarter (+1.3%), before falling back in the third quarter to the same level seen at the start of the year. Due to the very low starting level and the limited recovery throughout the year, the average annual production was no less than 13% lower than in 2022. This meant that annual production was at its lowest level since 2015.

Production past its low point

Seasonally adjusted production levels, April 2022 = 100

Source: CBS

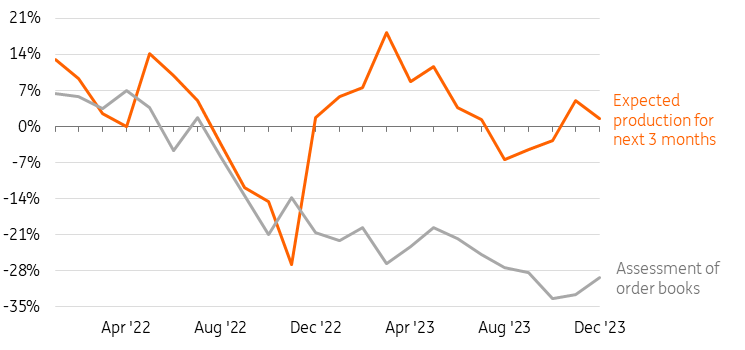

No high expectations for the near future

The mood of Dutch chemical manufacturers has cleared up somewhat in the second half of 2023, and they now have moderately positive production expectations for the near future. As a result of the very low starting point for the production level, however, we'd still caution against too much optimism for the time being. International market conditions are quite depressed and the competitive position is still under pressure. At the same time, dependence on foreign countries is high and chemical manufacturers are still very unhappy with their order books.

Chemical producers pessimistic about order books, slightly positive production expectations

Development of confidence indicators in the Dutch chemical industry

Source: CBS

Slight growth due to renewed stock building

A strong recovery is still pending, but moderate growth can be expected at the start of production chains in 2024 due to renewed stock building. When producers find their inventory levels too low in relation to expected sales, the chemicals industry finds itself at the forefront of increasing production. However, due to increased costs and weak demand, production levels will not return to pre-energy crisis levels anytime soon.

Moderate economic growth in Europe depresses demand for Dutch chemicals

As in 2023, reduced demand in 2024 is a major obstacle to stronger progress. While the inflation peak has largely passed, high interest rates remain an important growth inhibitors in all developed economies. Across the board, industrial products are finding it more difficult to find their way abroad. Made-in-Holland chemicals cannot escape this either. The cooling of the global economy will result in modest export development in 2024. The US continues to surprise so far, but in the Netherlands and the rest of the eurozone, economic growth this year is set to be very modest at best. Substantial growth can be expected in Asia, but on average it is not expected to be much higher than in 2023. It's also less important for the sector. More than 90% of its earnings come from exports and 80% of chemical exports remain within Europe. A flourishing European economy is a prerequisite for substantial growth of Dutch chemistry.

Unrest in the Red Sea could cause new supply disruptions and price increases...

While disruptions in supply chains continued to decline until autumn 2023, the unrest in the Middle East and specifically the Red Sea conflict increases the risk of new supply chain disruptions and price increases. While tanker traffic through the Red Sea held up well in December, (chemical) tankers have also increasingly avoided the sea route since the attacks. This means longer transport times around Africa, which cause delays in the delivery of some of the chemical inputs. The already limited availability of tankers is deteriorating, which could cause transport rates to rise again.

…although the consequences are manageable for the time being

Much depends on the duration of the logistics disruption, but for the time being, the consequences of the unrest appear limited for the chemical sector. A key difference between the pandemic era and the Ever Given blocking of the Suez Canal in 2021 is that international transport chains were much less disrupted prior to the current unrest and demand is now significantly weaker. Also, only a limited portion of chemical inputs imported by sea for domestic use normally pass through the Red Sea. For petroleum products, basic chemical substances and fertilisers together, the share is approximately 10%. If you also add crude oil – part of which is purchased as a petroleum product by the chemical industry after domestic refining – then this amounts to about 13%.

Lower, but still relatively high energy prices come at the expense of international competitiveness

In the first half of 2024, chemical manufacturers in the Netherlands still suffer from structurally higher energy prices and persistent stock reduction in the rest of the industry. While the acute threat from well-stocked gas storages has passed, gas prices in Europe are still three to four times higher than in the US, while this ratio was on average two throughout the five years before 2021. The expectation is that the European gas price will remain higher this year than in the past due to greater dependence on LNG, which will be unfavorable for the intercontinental competitive position and growth prospects of the chemical industry. Additional LNG supply is not expected until 2025, meaning prices remain sensitive to abrupt changes in supply and demand. It's also important to consider a revival of the Chinese economy and a temporary loss of production or transport capacity.

European gas prices are still multiples of American gas prices

Ratio between gas price Europe (Dutch TTF) and America (Henry Hub), forward day ahead, average per month

Source: Macrobond

Investments are under pressure but are desperately needed for a sustainable future

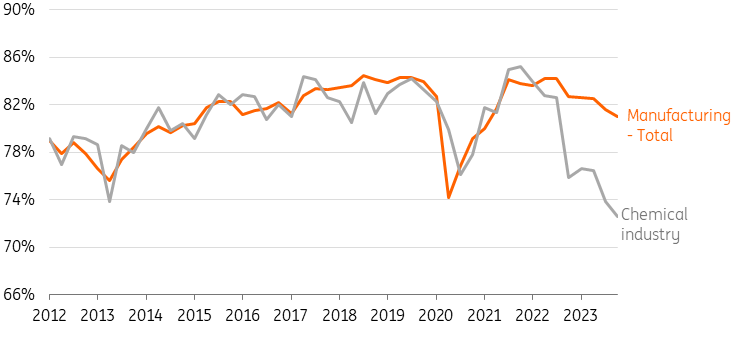

Due to the energy-driven difference in production costs, investments in Dutch and European chemical plants are expected to remain under pressure in the coming years, while the energy transition requires significant investments in these industries. The production contraction has resulted in a very low capacity utilisation rate, which also depresses willingness to invest. It also puts great pressure on productivity and therefore profit margins. For two years now, the majority of Dutch producers have seen profitability decline and investments by chemical multinationals have recently mainly taken place outside Europe.

Dutch chemical industry occupancy rate very low

Source: CBS

Investment environment more challenging

In addition to lagging investment, unequal subsidies and complex regulations around sustainability also put pressure on chemical production in the longer term. The US is promoting large investments in sustainability and national production facilities in an efficient way (through the IRA package), while this process is facing hurdles across Europe. In the Netherlands, a number of potential burdens put further pressure on investments by chemical producers. These include the higher energy tax and the abolition of the exemption from the energy tax for non-energy consumption. In addition, the Netherlands is the only EU Member State to have a CO2 tax in addition to the EU Emissions Trading System (ETS) and nitrogen limitations do not accelerate large-scale investments either.

Customised agreements between government and large chemical companies can trigger necessary investments in decarbonisation

At the same time, the industry is not at a standstill. There are plenty of pilot projects to make chemical production processes more sustainable with green hydrogen. Infrastructure for that is in the making. The Netherlands is also at the forefront of CO2 storage with the Porthos and Aramis projects (Rotterdam port and North Sea). The customised agreements that large chemical companies make with the government can accelerate decarbonisation. Salt producer Nobian is the furthest along in this space, and hopes to conclude an agreement the first quarter of 2024 to advance its CO2 neutrality target from 2040 to 2030 with public support.

More By This Author:

Key Events In Developed Markets For The Week Of Feb. 19Key Events In EMEA For The Week Of Feb. 19

UK Retail Sales Surge After Shock December Plunge

Comments

Log in or sign up to join the conversation.