Image Source: Pexels

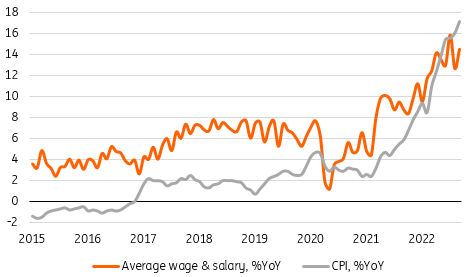

Average wages in the corporate sector rose by 14.5% YoY in September, significantly higher than the consensus (13.1% YoY) and the August print (12.7% YoY). In our view, the high minimum wage increase in 2023 will yield a wage-price spiral regardless of the market structure.

Employment in September increased by 2.3% YoY, against the consensus and the previous month's reading of 2.4% YoY. The Central Statistics Office has not yet released details, but it can be expected that, as in previous months, the increase in employment is mainly driven by services (retail trade, accommodation, and catering). This is also where a large portion of refugees from Ukraine, who at least partially do not appear in the statistics (they are not employed under a standard labor contract), most likely found work. According to ministerial data, more than 400,000 Ukrainian refugees who have arrived in Poland since the start of the war have already found employment. This shows that the demand for labor remains strong.

Wage growth falls behind price growth

Image Source: GUS.

The labor market is persistently tight. National Bank of Poland surveys indicate some slide in the percentage of companies planning to raise wages, but it still remains at a very high level. Companies also declared that wage increases will be very broad and apply to more than half of employees. Other surveys also indicate that the job search period is shortening. On top of that, there will be a very generous increase in the minimum wage from the beginning of 2023. Given the tight labor market, this should spur a wave of wage increases, maintaining double-digit wage growth in the business sector for most of next year. In our view, the high minimum wage increase in 2023 will yield a wage-price spiral regardless of the market structure.

The condition of the labor market is an argument for further tightening by the central bank, possibly with a hike in November.

More By This Author:

The Commodities Feed: Biden Confirms SPR Release

FX Daily: Steadier Price Action Belies Ongoing Nervousness

ECB Preview: Just Can’t Get Enough

Comments

Log in or sign up to join the conversation.