ECB Preview: Just Can’t Get Enough

A 75bp hike looks like a done deal but the European Central Bank has a lot on its plate at its October meeting. Quantitative Tightening talks are premature but it will seek to mop up bank liquidity. Rates, sovereign and money market spread upside dominates with the 10Y Bund set to test 2.5%. None of this should be enough to support the EUR.

President of the European Central Bank (ECB) Christine Lagarde

Too optimistic growth forecast no obstacle to a 75bp hike

When the ECB meets again next week, it looks as if the entire Governing Council could start humming the old Depeche Mode song “I just can’t get enough” as a choir. The hawks have clearly convinced the few doves left of the necessity to go big on rate hikes again. Contrary to the run-ups to the July and September meetings, there hasn’t been any publicly debated controversy on the size of the rate hike. In fact, ECB President Christine Lagarde seems to have succeeded in disciplining a sometimes very heterogeneously vocal club.

The economic backdrop of next week’s meeting has hardly changed from September. Confidence indicators have continued to drop, while hard data points at a very mild contraction of the eurozone economy in the third quarter. If anything, the ECB’s September growth projections that looked already very optimistic six weeks ago have become even less likely. Needless to say that the outlook for the eurozone economy is surrounded by an extremely high degree of uncertainty. The precise pass-through of higher energy and commodity prices on growth and inflation and the precise fiscal policy reaction are crucial but also very unclear determinants of eurozone growth and inflation in the coming months.

A lot on the ECB's plate besides hikes

At the current juncture, the ECB has turned a blind eye on recession risks but is highly determined to bring down inflation and inflation expectations. To this end, it is hard to see how the ECB cannot move again by 75bp at next week’s meeting. As the 75bp rate hike looks like a done deal, all eyes will also be on other, more open, issues: excess liquidity, quantitative tightening and the terminal interest rate.

- As regards excess liquidity, this seems to be the most pressing topic for the ECB and a solution could already be announced next week. Basically there are two possible options: reinstating a tiering multiplier or an ex post change of the terms of the targeted longer-term refinancing operations (TLTROs) in order to trigger early repayments. We think that reinstating a tiering multiplier would be the easiest option. Changing the TLTRO terms could hit the ECB’s credibility and would lead to reluctance of banks to ever make use of the TLTROs in the future again.

- As regards quantitative tightening, we think that markets have got ahead of themselves. Even if the discussion might have started at the ECB, with current financial stability risks, the recent UK experience and a very uncertain macro outlook, QT is still some way out. Christine Lagarde mentioned several times that interest rates would first have to be brought to their normal or neutral levels before any QT could start. Any QT would rather be an end to reinvestments than actively selling bonds. As we still see that end of the ECB’s rate hike cycle in the first quarter of next year, a gradual phasing out of the reinvestments under the Asset Purchase Programme (APP) could start in Spring 2023, at the earliest.

- As regards the level of the terminal rate, French central bank governor Francois Villeroy de Galhau said in an interview with the Financial Times that the ECB could “go quickly” to a deposit rate of 2% by year-end. ECB chief economist Philip Lane made similar comments, indicating that the ECB currently sees the neutral interest rate slightly above the common range of between 1% and 2%. We don’t expect a clear communication on where the terminal interest rate could be but see a growing consensus at the ECB that at least the neutral rate is currently a deposit rate of around 2%. This fits into our ECB call of another 50bp rate hike in December and 25bp in February before pausing as there is a high likelihood that already at the December meeting the ECB’s inflation forecasts for 2024 and 2025 will point to a return to price stability.

Interestingly, since the start of the year, the ECB surprised to the hawkish side at every single meeting. Next week’s meeting could be the first one without such a surprise as the ECB has finally managed to guide market expectations. A 75bp rate hike looks like a done deal and the reinstatement of a tiering multiplier could be the first answer to tackle excess liquidity. The ECB can simply not get enough of hiking rates aggressively.

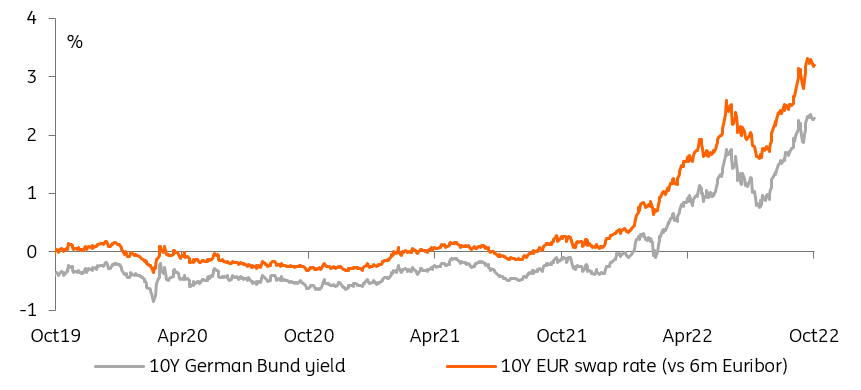

10Y Bund and swap rates won't turn before inflation starts declining

Source: Refinitiv, ING

Rates: upside risk dominates for now

High rates volatility, and the underlying uncertainty about the growth and inflation outlooks, don’t allow investors to focus on the long-term picture. We think there is sympathy with the view that the ECB’s hiking cycle will be stopped in its tracks by the looming recession, we doubt many market participants are able to position for it. All this is to say, near-term upside risk dominates and will dominate as long as investors haven’t seen tangible evidence of a downtrend in inflation. This puts 10Y Bund and EUR swaps within touching distance of 2.5% and 3.4% respectively before year-end.

With talk of QT, withdrawing bank liquidity, and front-loaded hikes, the ECB is piling risks on financial markets. The debacle in the gilt market in recent weeks should serve as a cautionary tale and is another reason for investor caution. Sovereign spreads have remained relatively stable in a context of elevated rates volatility and QT chatter, all this as Pandemic Emergency Purchase Programme (PEPP) bi-monthly data showed minimal market intervention in August and September. An accelerated timetable for QT would provide the impetus needed for the 10Y Italy-Germany spread to break above the fateful 250bp line.

Even with all that’s going on in long-dated interest rates, the action will probably be in money markets after the meeting. Whatever option the ECB retains to cause a repayment of TLTRO loans, the result will at least be a reduction in liquidity and greater sensitivity of money market rates to credit and sovereign spreads. Tiering, the most likely of these options, could have longer-lasting effects, ranging from easing collateral pressure in the best of cases, to differentiated pass-through of interest rates if not designed properly.

Money market and sovereign spreads aren't pricing ECB balance sheet reduction yet

Source: Refinitiv, ING

A strong euro is a welcome – but unlikely – development

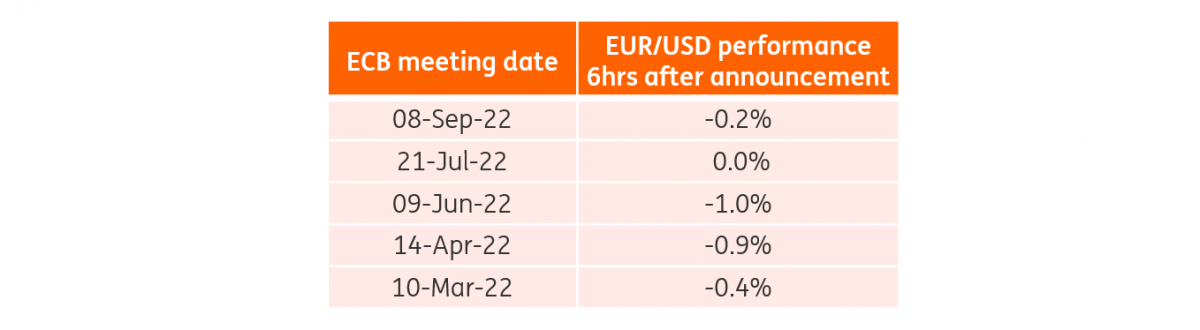

While it’s true that the ECB has consistently surprised on the hawkish side in the past few meetings, the positive impact on the euro have been null. As shown in the table below, EUR/USD mostly weakened in the six hours following the last five ECB announcements.

(Click on image to enlarge)

Source: ING, Refinitiv

We doubt there will be much support to the euro after the October announcement, even if the ECB attaches a hawkish message to a 75bp rate hike, as: 1) EUR/USD beta to short-term rate differentials has remained low; 2) markets have remained structurally pessimistic on the eurozone’s domestic outlook despite the recent drop in gas prices; and 3) the Fed’s hawkishness continues to fuel a strong dollar.

Attempts by the ECB to lift the euro through more tightening should still be unsuccessful in the near term and we continue to target 0.92 as a year-end value in EUR/USD, with any upside correction proving only temporary.

More By This Author:

Aluminum Market Braces For Supply DisruptionsUK Inflation Back In Double-Digits But Close To The Peak

The Commodities Feed: Further US SPR Releases

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more