Image Source: Unsplash

History takes its course. In this period of change, when the elements of rupture are multiplying, American monetary hegemony is weakening. One de-dollarization announcement follows another, sending out a strong signal on the international stage.

Today more than ever, central bank dollar reserves are shrinking, as is the US currency's share of international trade. Trade in raw materials, and oil in particular, is no exception. Many countries, misaligned with American unipolarity, are seeking to trade more in other currencies. One example is Saudi Arabia, the originator of petrodollars, whose trade in yuan is on the increase, despite its strong, historic ties with the United States.

While a global movement has thus been set in motion, the transition from one monetary dominance to another is a very long process. It implies new geopolitical alliances, changes in monetary and fiscal policies, reorientation of investments... These conditions have been met, but to date, neither the euro nor the yen, and even less the yuan, can take up the baton. As the dollar-denominated oil trade shrinks, and with it the dominance of the US currency, gold is once again emerging as a safe haven.

The history of petrodollars

A bit of history is in order. The history of petrodollars began in the aftermath of the Second World War. After the dominance of the pound sterling, it was in 1944 at the Bretton Woods conference that the United States, the world's leading military power, imposed the dollar as the reserve currency par excellence. In a period marked by economic and financial instability, this system temporarily facilitated international trade, but above all laid the foundations for the American superpower. For decades, only the dollar was convertible into gold, until 1971. With massive financing needs and the need to issue more dollars to maintain supremacy, US President Richard Nixon put an end to this convertibility, thereby introducing floating exchange rates. Since that day, the world has entered a new phase, neither fully understood nor elucidated, in which all currency is detached from the real value of goods and services.

Once this system was in place, the United States sought to anchor the dollar to something other than gold in order to maintain its confidence. Faced with the massive devaluation of the US currency after 1971, and the loss of profits by dollar-holding countries, the first oil crisis occurred. In 1973, the OPEC countries imposed an oil embargo, officially in response to American support for Israel during the Yom Kippur War. The importance of oil as one of the foundations of the economy was now widely recognized. In addition to the fact that this crisis caused energy prices to soar and geopolitical alliances to be turned upside down, the central idea was added that the economy is nothing more than transformed energy.

Barely a year later, the United States, represented by Secretary of State Henry Kissinger, and Saudi Arabia, represented by Prince Fahd Ibn Abdel Aziz, signed a crucial agreement. History records that it stabilized the international situation at a time when gas pumps were running dry and unemployment was rising. But above all, it served to strengthen the partnership signed between the two countries in the 1945 Quincy Pact. From then on, the majority of Saudi oil would be traded in dollars, and the profits generated would be recycled in American bonds. In exchange, the United States provided the country with military protection and economic support.

By anchoring the dollar to oil, this system created a constant demand for the American currency. Other oil producers, and then almost the whole world, adopted this system. Central banks naturally began to accumulate dollar reserves, especially as most commodities became quoted in US currency. For the United States, it was a historic victory to continue the "exorbitant privilege" of the American currency after the abandonment of the gold standard. Under these arrangements, the country could maintain low interest rates, and increase its deficit and debt to support its economy, without its currency depreciating. This definitively strengthened the United States' position as a financial superpower. The greenback became the sole currency of reference, on par with the hegemonic countries that preceded the United States. This was the case in the United Kingdom with the pound sterling in the 19th century, in the Netherlands with the Dutch guilder in the 18th century, and so on.

Towards the definitive end of petrodollars?

When the dollar is tied to raw materials, its hegemony can last indefinitely. After all, you need dollars to acquire these essential resources. Conversely, if it ceases to be linked to real value, its superpower declines, unless the United States uses its military might to maintain this influence. The United States has 700 military bases abroad in nearly 80 countries...

Such a scenario has been observed for decades in terms of American involvement in geopolitical conflicts. And even today, in the face of the desire of the so-called "Global South" to organize the creation of a multipolar world.

But this is a completely new period. In the wake of multiple American sanctions against Iran and Russia in particular, as well as the abusive use of the extraterritoriality of American law in many other countries, one announcement followed another. And the balance of power began to shift. The creation of the BRICS, despite all its internal contradictions, has created the conditions for real change. While 80% of the world's oil sales are still denominated in dollars, the member countries of the organization have begun to freely exchange their raw materials in currencies other than the dollar and to evoke "de-dollarization" as a real concept. This trend is all the more noteworthy given their stranglehold on strategic resources, including oil.

China plays a central role here. In 2018, it launched oil futures contracts, settled in yuan, and backed by gold. This initiative earned it sanctions from the United States, notably against the oil company Zhuhai Zhenrong, after its transactions with Iran in yuan. Nevertheless, in the face of domestic political challenges such as massive indebtedness, the real estate bubble, and aging demographics, China does not have the capacity to dethrone the dollar in either the short or long term. It is simply in a position to accelerate the process of global de-dollarization. Especially as Russia, Iran, and Venezuela (which together account for 40% of the world's oil reserves) already use the euro or yuan for their oil transactions.

In this respect, Russia is a staunch ally of the Xi Jinping government. There is no longer any doubt that the Russian economy has completely moved away from the dollar, not only of its own volition (remember that in the space of a decade, Russian hydrocarbon sales to the BRICS have fallen from 95% dollar transactions in 2013 to less than 10% in 2022) but also as a result of American and European sanctions, including the freezing of central bank assets. At the recent Sino-Russian summit in April, the use of the yuan for oil settlements was mentioned on numerous occasions. And the yuan was named as the currency of choice for their trade, ahead of the euro. A partnership between the world's second-largest economy and its biggest energy exporter sends out a strong signal to many countries. India, for example, has taken advantage of this to follow suit and trade some of its oil imports in its national currency or in yuan (and sometimes even in dirham, whose value is pegged to that of the US currency).

Saudi Arabia, the originator of petrodollars, is trading more in other currencies, despite its strong ties with the United States. In particular, it is in talks with China to trade in yuan. This is not a separation between the USA and the Gulf monarchy - far from it, contrary to rumors - but a strategic position taken by Mohammed Bin Salman. In recent months, Saudi Arabia's ARAMCO, one of the world's largest oil companies, has been steadily increasing the number of yuan-denominated transactions with China. As part of its domestic transformation and "Vision 2030" program, Saudi Arabia's main aim is to enhance its position on the international stage. This implies new partners and a shift away from US policy.

For its part, Europe has no pretensions to substituting itself for the petrodollar system, given its alliance with and dependence on the American system. Of course, Europe is one of the world's most dollar-rich regions and countries, thanks to its banking system. The 2008 crisis, like the banking crisis of 2023 (which led to the collapse of banking giant Crédit Suisse), demonstrated the need for European banks to receive dollars in the event of a crisis, thanks to the abundant distribution of dollars by the US Federal Reserve. As a result, the euro does not appear to be a credible alternative to petrodollars either. This is all the more true given the member states' blatant foreign dependence on raw materials.

Consequences for the US and global economy

In the USA, as elsewhere, this long-term trend is likely to have major financial repercussions. The use of currencies other than the dollar for the exchange of raw materials reduces global demand for the US currency. It also leads to high US interest rates for a long time to come, as the Fed must continue to make the dollar attractive. This it is already doing, against the grain of the ECB's policy and their diverging interests.

In the long term, this situation would accelerate the unsustainability of American private debt, but above all of the public debt, which is now estimated at over $34.5 trillion, forcing the government to spend more on servicing its debt than on its military-industrial complex...

High interest rates also mean a weaker U.S. bond market. This market is by far the world's largest in terms of volume traded. The repercussions would be felt not only by US regional banks, which are heavily exposed to government bonds but more generally through the depreciation of securities held by investors. To date, foreign investors, including central banks, hold nearly $8 trillion in US government debt. All other things being equal, readjustments in the world's financial markets, affecting exchange rates, commodity prices, and the dynamics of international trade, are to be expected.

Gold, a historic metal for an alternative solution?

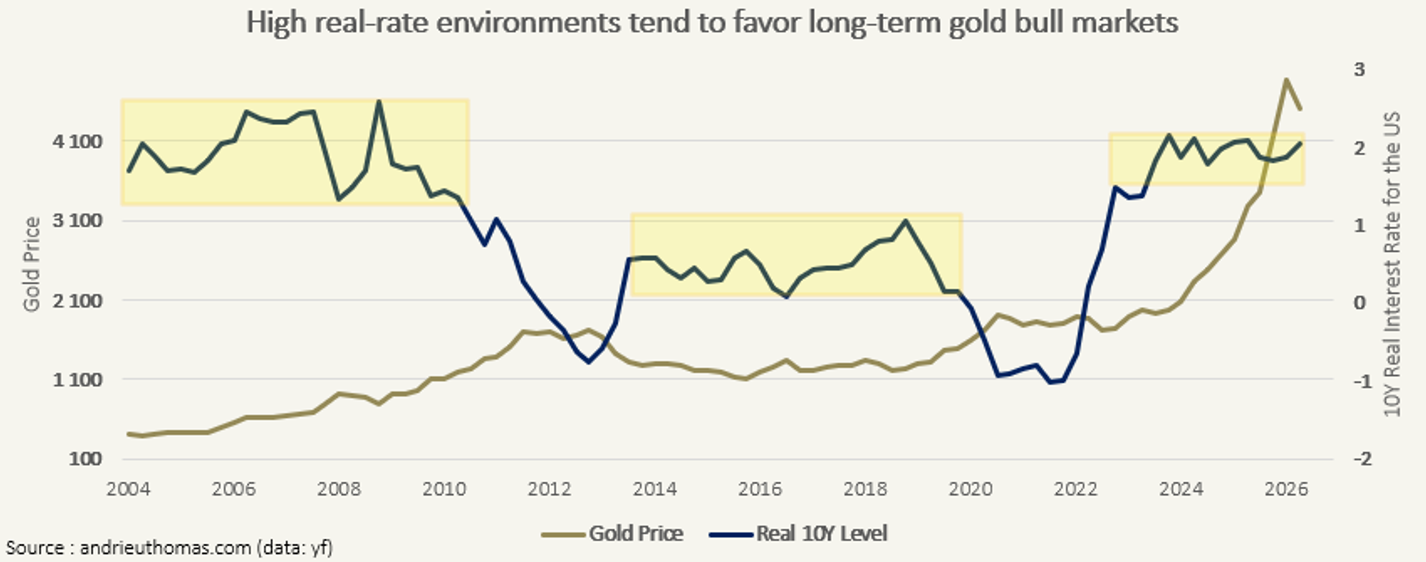

As gold is no longer accepted as a means of payment, it cannot replace petrodollars. On the other hand, the historical trend is likely to create a catalytic effect, leading to increased demand for gold.

As much as gold has broken its historical link with the dollar, oil no longer moves so much in line with the US currency. In the past, when the dollar gained in value, the price of oil tended to weaken. But today, this link has largely disappeared, to the benefit of countries that are de-dollarizing. These countries not only pay more in currencies other than the dollar but also buy oil at prices that do not fluctuate according to the value of the US currency.

While the consequences for the dollar's dominance are therefore equivocal, this scenario creates all the conditions for another currency to take over. Given that no country is really ready to take on the United States, and will not be tomorrow, gold's independence makes it the safe-haven currency par excellence.

More By This Author:

Silver Quarterly And 6-Month Closes Confirm Upward TrendAcceleration Of The Silver Price Rise In The Short Term

We Can Dissolve The National Assembly, But Not The Debt

Comments

Log in or sign up to join the conversation.