TM Editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

Image Source: Pixabay

When planning for retirement, you want to be sure you’ll generate enough retirement income from your portfolio. As you retire, you still have plenty of years ahead of you. Let’s make sure you don’t outlive your portfolio, shall we? There are two ways to generate income from your portfolio if you are a dividend investor. Let’s take a close look at both.

Dividend-Only

Get your income entirely in dividends received from your investments. If you have $800,000 invested and need $30,000 per year, it's easy. Just ensure your portfolio averages 3.75% in dividend yield, and you’re done.

If all you need is a 3% to 4% yield, you won’t have much to worry about. Unfortunately, many retirees face entirely different situations, like needing $50,000 per year while having $600,00 invested. While there are smart ways to improve your dividend yield up to a point, generating a consistent 8.3% yield is not easy.

How About High-Income Products?

There are generous Master Limited Partnerships (MLPs) or split share products generating 8%+ yield. However, a glance at their long-term returns show they might not be the best income strategy. For example, here is a look at Canoe Income Fund (ENDTF) and Financial 15 Split Corp. (FNNCF).

(Click on image to enlarge)

Over 10 years, Canoe’s dividend income was flat most of the time, eaten up by inflation year after year, while the price slowly but surely declined. Meanwhile, Financial 15 Split Corp. investors also had flat dividend income, as the dividend was cut 2020 and flatlined, and the stock price dropped 60%.

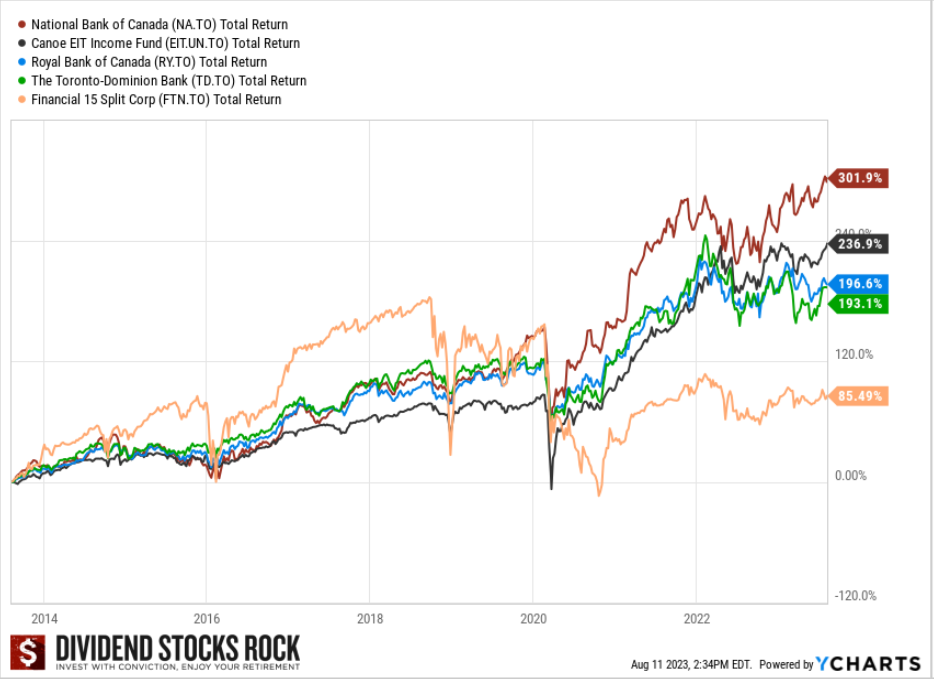

Financial 15 Split Corp. was described as a “high-quality portfolio consisting of 15 financial services companies made up of Canadian and U.S. issuers.” This next graph clearly shows that buying stocks from three Canadian banks would have saved Financial 15 Split Corp. investors a lot of money, not to mention a lot of grief.

(Click on image to enlarge)

What About High-Yield Stocks, Then?

Many dividend investors think that capital gains don’t count until you cash them, while an 8% dividend yield is real and more secure.

They’re wrong to assume their 8% dividend yield is more secure than a total return of 8% consisting of 3% yield and 5% capital gain. Sure, the 8% yield is easier to calculate and looks more stable. You pocket your dividends and move on. However, how many 8% yielders eventually cut their dividend and suffer massive capital loss? Enough to kill your retirement portfolio.

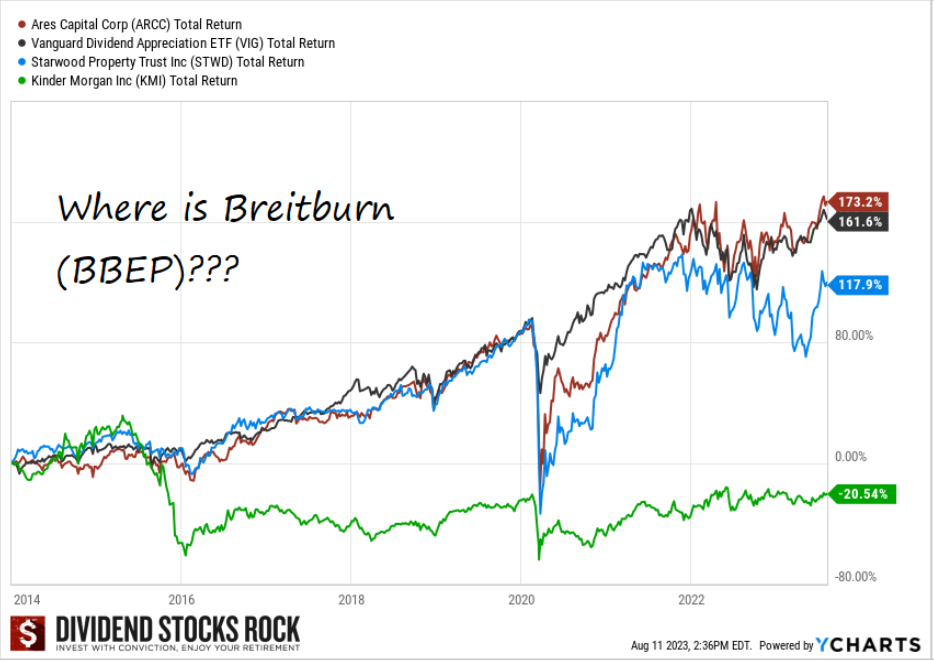

Look at the total returns over 10 years of four high-yield stocks that you may have seen investors raving about in 2014 (ARCC, STWD, KMI, and BBEP) along with a classic dividend growth ETF (VIG).

(Click on image to enlarge)

Are you looking for BBEP? Don’t bother, it went bankrupt in 2018. Of these four “safe” high-yield stocks:

- ARCC kept pace with the ETF

- STWD performed decently

- KMI generated a loss (-20% including the dividend since Jan. 1, 2014)

- BBEP wiped out investor’s money completely

Choosing stocks with high yields is like skating at full speed without knowing how to turn. If not high-income products or high-yield stocks, then what’s the solution? Make your own dividend with a blended portfolio.

Blended Portfolio

With a blended portfolio, you can make your own dividend by focusing on total return rather than dividend alone. I recently had a chat with an income-seeking investor who was comparing these to companies:

|

Canadian Utilities |

Alimentation Couche-Tard |

|

Utility with limited growth potential |

Growth-oriented company |

|

50 years of dividend growth |

Impressive dividend growth rate |

|

5.6% yield |

Mediocre yield of 0.8% |

At 0.80% yield, it’ll take Couche-Tard forever to reach Canadian Utilities’ yield. So, should you pick Canadian Utilities and forget Couche-Tard? Not so fast.

Total Returns, Remember?

Couche-Tard offers a low yield because the company uses most of its money to grow the business, adding value for shareholders. Rather than assessing revenue from Couche-Tard on its dividend alone, ask yourself this: will Couche-Tard’s stock price appreciation, combined with its dividend, surpass total returns for Canadian Utilities?

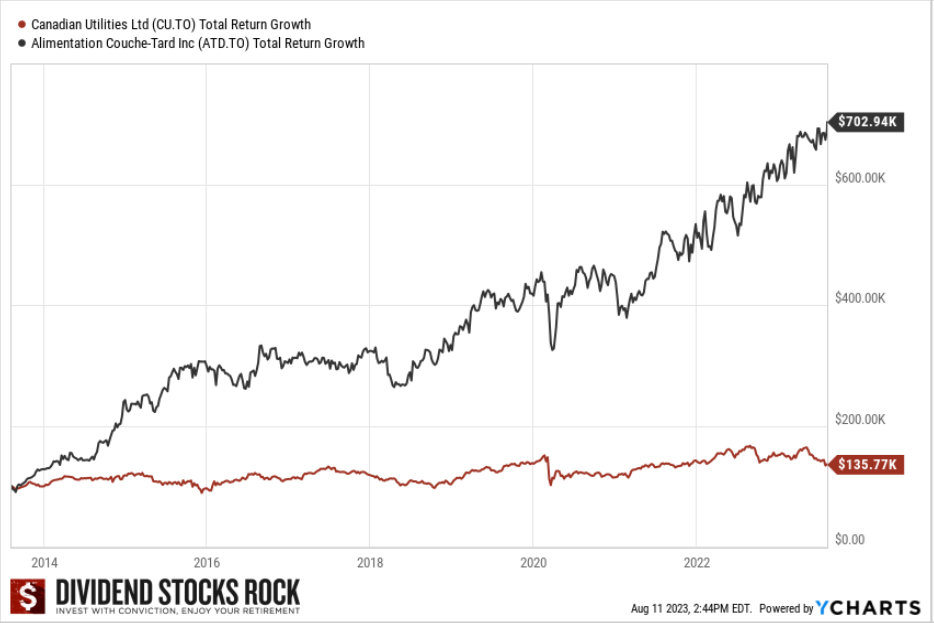

Compare $100,000 invested in Couche-Tard and $100,000 in Canadian Utilities ten years ago, with the dividends reinvested along the way.

(Click on image to enlarge)

That’s right, over the past 10 years, Couche-Tard surged more than 600%. Canadian Utilities didn’t even hit 40%. Which of these stocks generated the most income? Note that I didn’t cherry-pick Couche-Tard and Canadian Utilities to manufacture an extreme example; it’s a comparison I've seen a real investor make, and it clearly shows the impact of considering total returns rather than only dividends.

So, How to Generate Enough Retirement Income?

I’m not saying that you should invest everything in low-yield high-growth stocks like Couche-Tard and ignore the others. In retirement, we want some “sure shots” like Canadian Utilities in our portfolio. They bring stability, a decent expectation of a good income year after year, and they make it a lot easier to budget.

There are smart ways to increase a low portfolio yield of 2% to a better 3%-3.5%. For example, replace some low yield stocks with higher yield companies in the same sector. Or adjust your sector allocation to increase holdings in sectors that are more generous such as utilities, REITs, telcos, or Canadian banks.

The idea here is to strike a balance between low yield, high growth stocks, and classic retirement stocks, such as utilities and REITs. This creates the perfect blended retirement portfolio rather than one focused solely on dividend yield. When retired, it’s easy to sell a few shares of your high growth investments, as needed, and create your own dividend.

Value is value, whether it’s the dividend or in the stock price. Build a portfolio filled with amazing dividend growers, and you won’t have to worry about your average dividend yield.

More By This Author:

Market Review – August Dividend Income Report

Retirement Withdrawal Strategy: Avoid Panic, Enjoy Life

Do Down Markets Affect Retirement?

Comments

Log in or sign up to join the conversation.