Image Source: Pexels

Prior to the European Central Bank’s hiking cycle, one thing was certain: demand for housing exceeded supply, giving sellers significant pricing power and limiting buyers’ ability to negotiate. Over the past two years, supply and demand pressures have eased against a backdrop of higher mortgage rates. However, they are likely to make a comeback.

Demographics and prosperity are key drivers of increase in housing demand

One of the key reasons why Eurozone house prices rose sharply in the decade prior to the ECB's recent rate hike cycle is that demand for housing surged on the back of various structural factors. The disproportionately strong increase in the number of households compared to population growth played a decisive role here. Between 2013 and 2023, the Eurozone population grew by around 3%, while the number of households increased by 7%. As a result, the number of people sharing a household decreased. In 2023, the average household in the Eurozone consisted of 2.2 persons. Just 10 years ago, an average of 2.3 persons shared a household. In Germany, the average household consisted of 2 people as of late, and in the Netherlands and Belgium, 2.1 and 2.3 people shared a household, respectively, on average. As a result, the type of housing in demand is changing in line with developments in the size and type of households. It also means that some homes still on the market no longer meet demand.

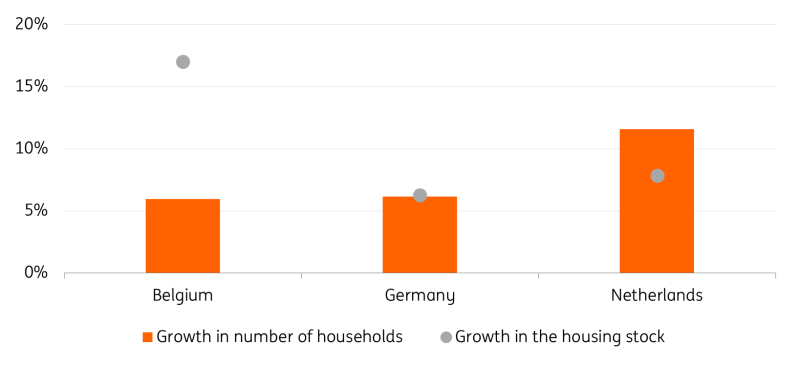

In some countries, the number of households has grown significantly faster than the housing stock, which has significantly exacerbated the structural housing shortage. The situation is most tense in the Netherlands, where the number of households has risen significantly faster than the housing stock. In Germany, the number of households and the housing stock have grown at roughly the same rate, whereas in Belgium, housing stock growth has outstripped the increase in the number of households.

Change in number of households and the housing stock*

Source: OECD (Change between 2020 and 2010 for Belgium, between 2021 and 2011 for Germany and between 2021 and 2012 for the Netherlands); Eurostat

*In the case of Belgium, the sharp increase in housing stock can probably be explained in part by the high level of construction activity for vacation homes on the Belgian coast, which is likely to overestimate the number of dwellings actually available as main homes

In addition, prosperity has risen significantly in many Eurozone countries over the past 10 years. In 2023, real gross disposable income per capita in the Eurozone was around 11% higher than in 2013. The increase in purchasing power has had a positive impact on the affordability of housing in the past. In combination with favourable financing rates, the idea of owning a home has become more feasible for many people.

Supply is not keeping up with demand for housing

This strong increase in demand could not be met in recent years, however, which is why strong excess demand has built up over time. Between 2013 and 2023, the building of 3.2 million newly built homes was permitted in Germany. At the same time, only 2.7 million homes were completed. In Belgium, the situation is similar: while some 545,000 apartments were approved for construction over the past 10 years, the actual number of apartments increased by only 515,000. A look at new construction activity in the Netherlands initially gives the impression that the situation is more relaxed than in Germany and Belgium. Over the past 10 years, the construction of some 640,000 newly built homes has been permitted and approximately the same number of newly built homes were completed in the same period. Nevertheless, according to ABF Research, it is estimated that the Dutch housing market is lacking some 390,000 homes to meet the number of home seekers.

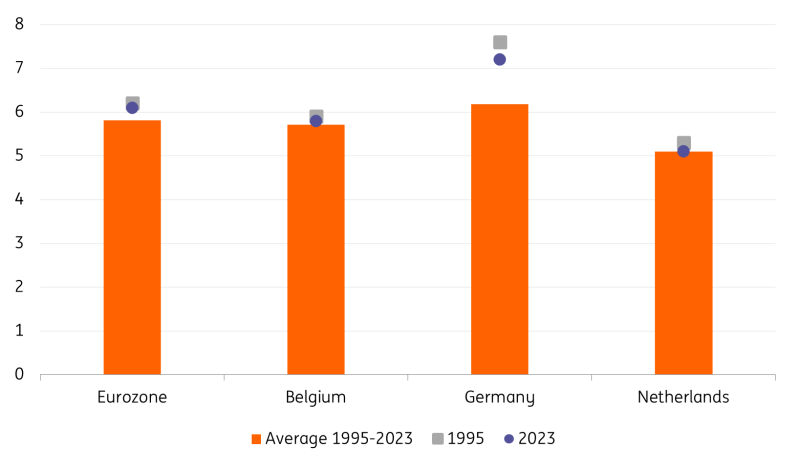

That construction activity was unable to keep pace with high demand in recent years can, on the one hand, be explained by structural factors. Between 2013 and 2023, on average 15% of construction companies in the Eurozone stated that a shortage of labour would limit activity, compared to only 10% in the previous 10 years. Furthermore, investment activity in residential construction has remained broadly unchanged over the past 30 years and is therefore also lagging the increase in demand for housing.

Investment in housing

(% of GDP)

Source: Eurostat; ING

Gradual housing market recovery to fuel demand again, while supply remains limited

Looking ahead, we do not expect much of a significant improvement in the supply of housing. Both economic and political uncertainty remain elevated, weighing on investment activity. In April, the EU adopted the revised Energy Performance of Buildings Directive (EPBD). The aim of the directive is to increase the renovation rate of properties, especially of energy-inefficient ones. Member states will have to transpose the directive into national law within two years. However, it is not yet clear how the national plans for the green transition of the housing market will look in detail. Especially since many EU member states are likely to adopt tighter fiscal policies in the coming years, uncertainty regarding any potential support for the greening of the housing market is growing. Yet planning security is essential to meet this challenge. Furthermore, increasingly strict regulations are slowing the development of new property projects. Building standards are high, increasing complexity, digitisation is lagging behind, preventing accelerated processes and, at the same time, there is also a shortage of skilled workers in public authorities. And while the economic recovery in the Eurozone will be only a gradual one overall, it will take even longer for activity in the construction sector to pick up steam again.

At the same time, as the cyclical improvement in the economy continues, the Eurozone housing market will eventually find a new equilibrium over the course of the year and the lack of new housing is likely to exert upward pressure on prices. In the first quarter, house price development across Eurozone countries was still mixed.

- In the Netherlands, house prices recently surpassed their previous peak level of mid-2022. After having fallen by some 6% between July 2022 and May 2023, house prices began to rise rapidly in June last year. In April 2024, house prices were 7.5% higher than they were in the same month a year ago.

- In Belgium, where wage indexation had helped to keep the housing market much more stable than in many other Eurozone countries last year, median home prices rose by 1% YoY in the first quarter of 2024.

- In Germany, on the other hand, the bottoming out of the housing market has proved to be lengthier than expected with house prices falling by 1.1 % quarter-on-quarter in the first quarter of 2024.

Nevertheless, there have already been initial signs of a tentative recovery in the Eurozone housing market, with improved affordability being the main driver. At the beginning of the year, mortgage rates had fallen significantly. At the same time, house prices had fallen below their 2022 levels and wages in the Eurozone rose by 5.3% in the first quarter of 2024. Although affordability has only improved from extremely low levels and the potential for further improvement remains limited, demand is expected to pick up gradually over the course of the year.

Excess demand too large to ease significantly, exerting upward pressure on prices

Looking ahead, we expect the mismatch between supply and demand to intensify again. Demand for housing will gradually recover, while the construction sector remains under pressure from high material costs and a shortage of skilled workers. This does not bode well for the supply of affordable housing in particular. While the strengthening of the mismatch will probably be reflected in the general development of house prices, prices for newly completed buildings, in particular, are expected to be significantly higher in the future than in the past.

More By This Author:

The Commodities Feed: Oil Rises On Supply WoesEurozone Inflation Ticks Down In June

FX Daily: Trump Bets Drive Dollar Higher

Comments

Log in or sign up to join the conversation.