Photo by Michelle Spollen on Unsplash

Banks are often the first to sniff out any economic weakness, as they begin to put aside funds to cover expected losses in the coming year. One of the big reasons the Big Six missed profit expectations can be traced to those funds funneled directly to loan loss provisions (PCL). Banks set aside a certain amount of earnings to cover future shortfalls affecting their capital when customers are not able to service or repay loans. Collectively, the majors are looking at putting aside about $3 billion, but more importantly this provision is a big step up from provisions set aside a year ago. PCL for the majors for the quarter are:

- TD, set aside a total of C$599 million;

- BMO, set aside a total of $492 million, compared to $136 million a year ago;

- CIBC provided for $438 million, an increase from $303 million, a year ago;

- Scotiabank allocated $709 million, a dramatic increase from $219 million last year;

- National Bank doubled its provisions from last year to $111 millions; and,

- RBC, Canada’s largest bank, recorded $600 million in expected loan losses, compared to $342 a year ago.

Conceptually, these provisions are considered as insurance to cover bad loans and hence are taken out of current earnings. By the same token, should a bank’s loan book not deteriorate to the full extent of the PCL, the difference is reinstated in earnings.

For bank investors, the betting when to purchase shares resides in the outlook for the economy. Did the banks put aside too much or too little to cover losses and what does that mean for bank profitability? An early sign regarding the outlook was delivered this week when the GDP second-quarter results became available, and the news was not comforting at all.

The Canadian contracted by 0.2%, in contrast to the Bank of Canada’s most recent forecast of 1.5% expansion. Clearly, the Bank’s forecasting team got it wrong. Given the low level of growth to begin with, this forecasting error is quite large.

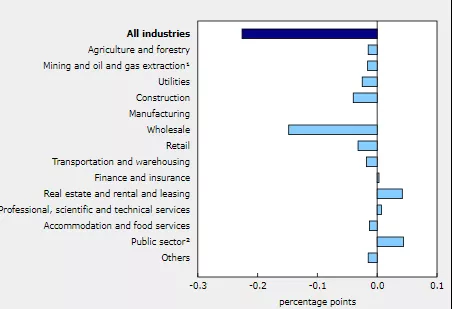

Components Contribution to GDP

One of the most important sectors contributing to this decline is residential investment---- no surprise there, considering the Bank of Canada’s relentless rate hikes. Construction expenditures falling off at a time when house prices are firming up, sets up for more stress in the housing market as supply issues dominate the industry. The consumer sector, wholesale and retail, shrunk, strongly suggesting that the conventional wisdom that nothing can stop the consumer is misplaced. Ironically, the Bank of Canada argued that the consumer resilience continues to support the Bank’s need to hold firm on its rate policy. Economists are now focusing on the poor GDP results for July as further evidence the economy is probably has entered a recession.

Since the Bank of Canada’s decision-making process is shrouded in secrecy, we can hope that it recognizes that the economy is not on a good trajectory and that the banks are signaling the further trouble lies ahead.

More By This Author:

Waiting For The Anticipated Recession Is Very Tiresome

Why The Bank Of Canada’s Rate Hikes Are Not Working

The Bank Of Canada Has Entered The Realm Of Overkill

Comments

Log in or sign up to join the conversation.