As we share below, bond market sentiment, known officially as the term premium, has been almost entirely responsible for the recent surge in bond yields. Specifically, behind the move is investor concern regarding another round of inflation stemming from the recent Fed’s rate cuts. The poor sentiment is very apparent when comparing news to a market reaction. Typically, when sentiment is poor, bad news has a more significant negative impact than the positive impact of good news. The opposite holds when sentiment is good.

A great example is the bond market action on Monday. On Monday, the ISM services price paid index was higher than expected. That should warrant some inflation concern. However, ISM is based on a survey and is not hard data. Respondents answered whether prices were up, down, or stable. While more respondents said prices rose in December, they don’t quantify by how much. Actual inflation data in the PCE prices index showed a small gain of 0.1% on December 20, 2024. PCE quantifies the price change and is the Fed’s favorite and most trusted inflation gauge. After initially rallying on the news, yields closed that day relatively flat. The ISM prices survey caused longer-term bond yields to increase by 6-7bps.

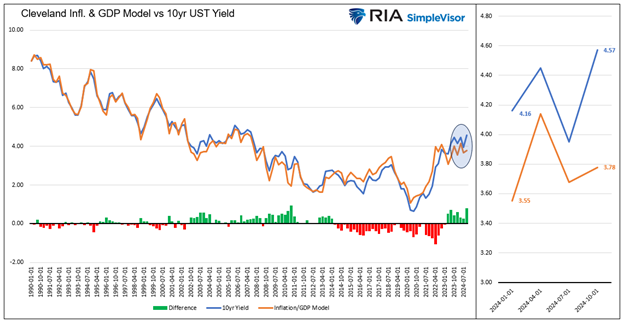

Did the Fed cut rates? And should that spike inflation concerns? Technically, the Fed has reduced the Fed Funds rate by 100bps. However, longer-term yields, which drive economic activity and inflation, have risen significantly. Despite the Fed rate cuts, monetary policy is much more restrictive than when they first cut rates in September, as shown below.

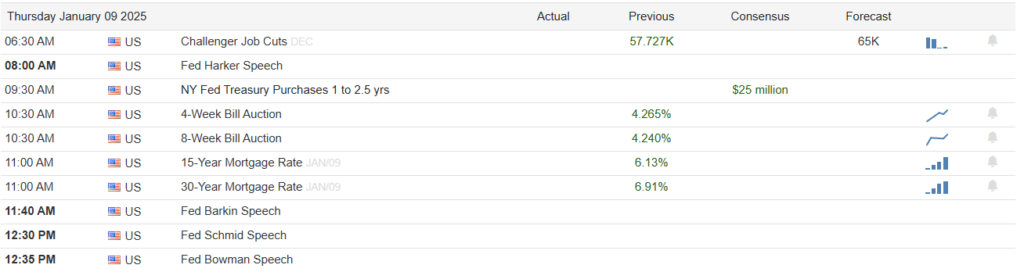

What To Watch Today

Earnings

- No notable earnings releases today

Economy

(Click on image to enlarge)

Market Trading Update

The market is closed today in Memorium for Jimmy Carter. However, yesterday, we discussed the decline in equity fund spreads following the most recent FOMC policy meeting. Since then, bond yields have risen, and asset prices have fallen as expectations for future Fed rate cuts have been reversed. We also discussed the increase in institutional selling pressure as hedge funds have shorted assets across markets, putting downward pressure on prices.

Two things have continued to plague the markets over the last few days that are entirely “sentiment” driven: concerns that “tariffs” could lead to inflationary pressures and valuations. The concern over tariffs has created a feedback loop in the economy. Since the election, producers have been buying products to get ahead of tariffs, which increased demand for those products, pushing prices higher, as seen in recent ISM reports. In other words, the fear of tariffs creating inflation caused inflation by their actions. However, as discussed in this article, tariffs haven’t caused inflation historically.

Secondly, valuations are becoming more of a concern for markets, particularly as the equity risk premium declines. Equity risk premiums (ERP) are also driven by sentiment. As investors expect increased asset prices, they are willing to be “paid less” for the “risk” they are taking to own equities. However, with bond yields now significantly above the ERP, there is an increasing probability that investors, at some point, may opt for being “paid” by owning bonds.

For now, there is a lot of chop in the market as positioning changes continue to run amok over the last few trading days. However, we will be watching closely how the first week of trading wraps up, which historically sets the tone for the month.

Will The Fed Sit On Their Hands?

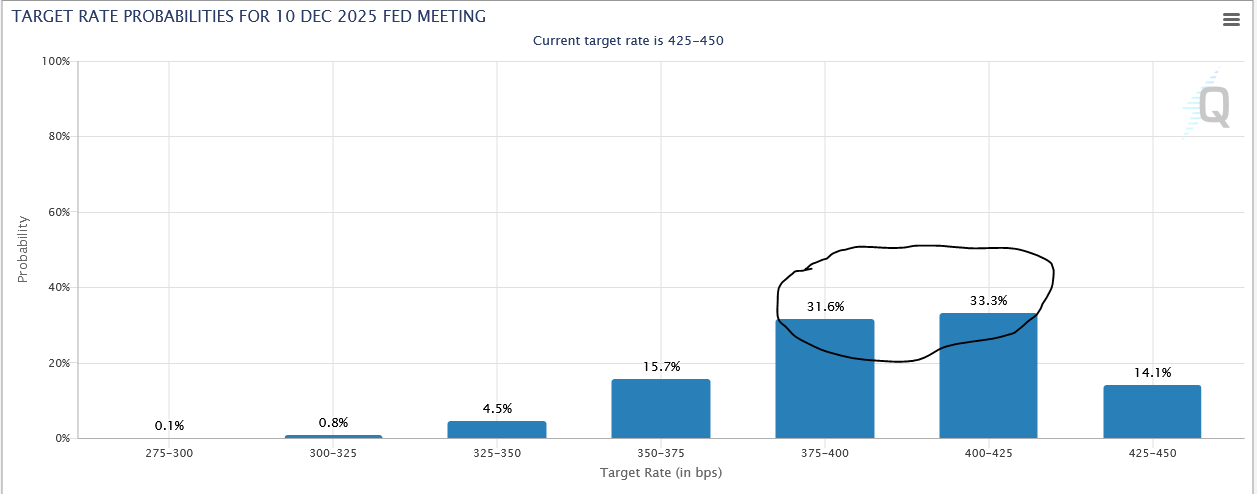

Market expectations for more rate cuts have diminished significantly, as witnessed by rising bond yields. The graph below, courtesy of the CME, shows that the market implies a 50/50 chance the Fed will cut by 25bps or 50bps during the remainder of the year. It assigns a 15% they don’t cut and about 20% they cut by more than 50bps. As a reference, in September, when the Fed initially cut rates by 50 bps, the market thought Fed Funds would end 2025 at 2.80% (100-97.20), as shown in the second graph.

With the market now expecting little from the Fed, the surprise might be that they cut more aggressively than expected. Traditionally, the market has grossly underestimated Fed moves, whether hikes or cuts.

Why Are Bond Yields Rising?

Unlike short- and medium-term gyrations in stock prices, which are often due to changes in investor sentiment, the bond market has a much more fundamental grounding. Interest rates, representing the cost of money, strongly impact economic activity and inflation in a highly leveraged economy like ours. Thus, economic growth, inflation, and Treasury bond yields are highly correlated.

That said, bond investor sentiment does impact yields and can be relatively accurately quantified, unlike the stock market. In bond market parlance sentiment is called the “term premium or discount.”

Quantifying the term premium or discount and, equally important, understanding the market narratives responsible for the premium or discount is valuable. With such knowledge, one can assess whether the narratives make sense. Thus, is the premium or discount likely to be sustained? If the narrative(s) are illogical, there could be an opportunity to profit when the premium or discount normalizes.

With that, let’s better appreciate why bond yields are rising.

Tweet of the Day

More By This Author:

1-8-25 Is the January Barometer Broken?Credit Spreads Send A Warning For Stock Investors

Corporate Executives Are Bullish And Bearish

Comments

Log in or sign up to join the conversation.