Blue Owl Capital spooked AI investors on Wednesday when the Financial Times reported that the firm, one of Oracle’s larger financing partners for major U.S. data centers, decided not to provide equity backing for a $10 billion data center Oracle is building in Michigan. This planned facility is part of Oracle’s collaboration with OpenAI under their Stargate AI infrastructure initiative. Blue Owl reversed course on concerns about less favorable lease and debt terms compared with prior deals. Moreover, Blue Owl is worried about potential delays from local politics.

Maybe, of most concern to Blue Owl, Oracle’s debt is increasing rapidly. For example, Oracle has over $127 billion in debt, of which about 20% matures within three years. Furthermore, over the past 12 months, Oracle reported negative free cash flow. Analysts do not expect it turn positive for at least two more years. As shown below, credit default swaps on Oracle have increased rapidly. For more on Oracle CDS, check out our Commentary from November.

Oracle disputed the implications of losing Blue Owl financing. They claim it has multiple funding sources, including Blackstone and Bank of America, which will allow it to move forward with the Michigan project. To wit, please see the Tweet of the Day. However, and of importance to the broader market, it further raises investor concerns about financing massive AI data center expansions. While the power grid has been a primary concern for investors, rapidly rising debt levels and the financing of large infrastructure projects may be a close second.

What To Watch Today

Earnings

(Click on image to enlarge)

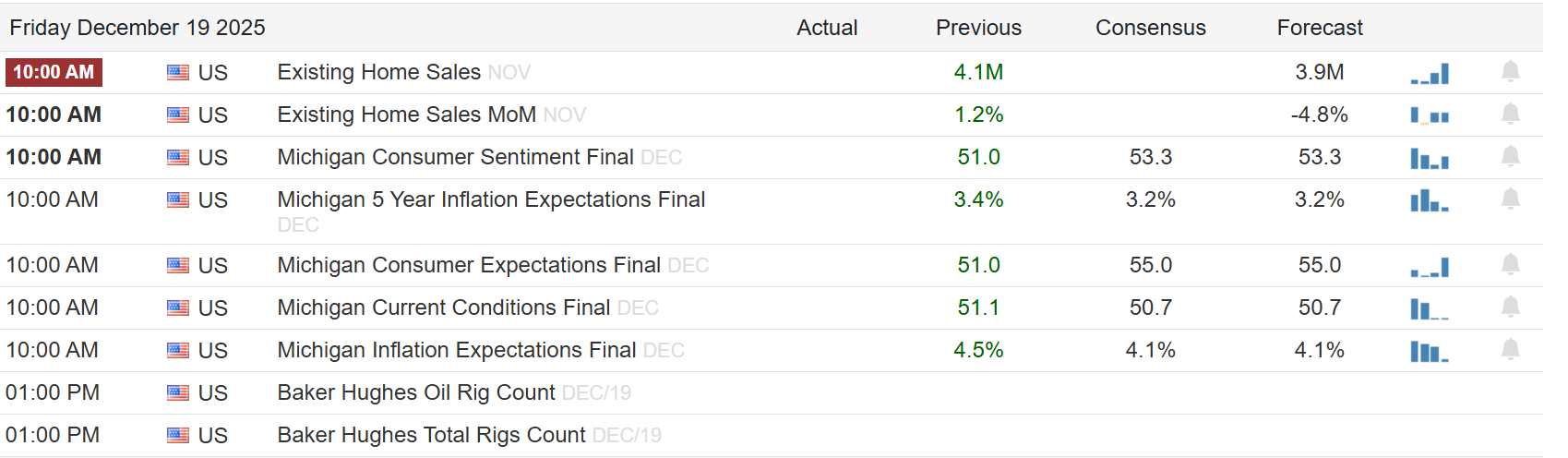

Economy

(Click on image to enlarge)

Market Trading Update

Yesterday, we discussed the weekly technical backdrop, which suggests a “recalibration” in the overall market. I wanted to turn our attention to oil today.

As shown, oil prices have declined sharply this year amid persistent oversupply, falling from $80/bbl in January to below $60 today.

(Click on image to enlarge)

Wholesale and retail fuel prices have dropped, hitting levels not seen since the pandemic, even as demand for holiday travel increases. As oversupply builds across major benchmarks, such pushes sellers to offload cargoes, weighing further on prices. Producers with weaker balance sheets, such as mid‑sized E&P firms, are experiencing share price pressure tied to the market downturn. Furthermore, industry surveys show that both current and expected activity remains subdued with price expectations for 2026 below breakeven levels for many producers.

That isn’t a strong backdrop for a strong rally in energy prices. However, the big question for investors is whether they should build energy positions today, anticipating a future resurgence of demand. So, what could cause oil prices to rise in 2026? Some of the reasons are obvious, others are not.

1. A Reversal in OPEC+ Policy: If OPEC+ decides to cut production further or maintain existing cuts longer than expected, supply would tighten. With inventories already low in some regions, this would put immediate upward pressure on prices. If U.S. shale production also continues to slow, that would compound the impact.

2. A Weaker U.S. Dollar: Oil is priced in dollars globally. If the dollar weakens due to Federal Reserve rate cuts or U.S. fiscal imbalances, oil becomes cheaper in foreign currencies. This can boost global demand and push prices higher, even if supply remains constant.

3. Faster-Than-Expected Global Economic Growth: If global growth re-accelerates—especially in China, India, and Southeast Asia—oil demand could rise meaningfully. A synchronized rebound in industrial activity, freight movement, and consumer travel could tilt the supply-demand balance.

4. A Resurgence in Transportation Demand: Despite the EV push, most of the global fleet remains fossil-fuel based. Any delay in EV penetration or resurgence in gasoline and diesel vehicle use could surprise to the upside on demand.

5. Artificial Intelligence and Data Centers: While data centers consume vast amounts of power, they don’t currently run on oil-based fuels. Most draw electricity from the grid, which is generated primarily from natural gas, coal, nuclear, and renewables. If data center buildouts continue to surge, this will lift electricity demand, but the spillover into oil markets would be minimal unless grid shortages force backup diesel generation. That’s plausible in regions with poor infrastructure or unstable grids.

If you assume that the risk of higher oil prices in 2026 is likely, how should you consider positioning your portfolio today? Crucially, this is not a “trade” but requires a longer‑term, selective positioning for an eventual reversal.

1. Prioritize Cash‑Flow Strong Producers: Large integrated oil majors with lower production costs, diversified assets, and strong cash flows are better positioned to withstand lower price environments. These firms tend to maintain dividends and buybacks even when crude oil prices trade lower, providing a cushion for shareholders.

2. Avoid Highly Leveraged E&P Names: Smaller exploration and production companies often require oil prices above $60–$65 per barrel to fund growth and service debt. With forecasts clustering below those levels, those stocks carry a higher risk.

3. Use Sector ETFs for Broad Exposure: Energy sector ETFs provide diversified exposure to multiple names, reducing single‑company risk. These can serve as core holdings for investors seeking to capitalize on any rebound in commodity pricing or sector re-rating.

4. Dividend Yield Matters in Lower Price Environments: Energy stocks with strong dividend yields offer income even in flat price environments. Reinvesting dividends improves total return potential when prices are subdued.

5. Monitor Leading Indicators and Manage Risk Actively: Oil inventories, OPEC policy changes, rig counts, and global demand data should inform trade timing. Hedging strategies such as protective puts or covered calls help manage downside risks in a volatile market.

6. Time Horizons Must Reflect Weak Price Trends: Given forecasts for lower prices, short‑term traders should use dollar‑cost averaging to enter positions gradually and avoid single‑point market timing. Long‑term holders should focus on structural factors such as production discipline, capital spending discipline, and dividend sustainability.

The energy sector remains relevant for diversified portfolios, but the market environment is currently bearish on oil prices through 2026. Positioning should favor quality, cash flow, balance sheet strength, and diversified exposure, rather than speculative bets. Even in weak price cycles, disciplined energy companies generate shareholder returns through dividends and operational efficiencies.

Trade accordingly.

CPI Was Lower Than Expected

The BLS released a blended October-November CPI report to cover the period of the government shutdown. CPI was well below the 3.1% expectation at 2.7%. Core CPI was also 0.4 percentage points below consensus at 2.6%. Rent prices, i.e., shelter costs, which account for 40% of CPI, were 1.6% annualized, less than half the 3.8% rate in the three months prior. While the inflation data were undoubtedly excellent news, the market will likely doubt them and raise questions about specific adjustments the BLS made to account for the October data void.

Evidence of market doubt was evident in the muted bond market reaction to the news. The graph below, courtesy of FinViz, shows the price of ten-year Treasury note futures. At 8:30 ET, when the data was released, the price spiked by about 50 cents, but after about half an hour, it returned to its pre-release level. Similarly, Fed Funds futures barely budged, indicating that the odds of a rate cut at the January 28th meeting were not affected by the CPI release. Bond investors may dismiss the CPI report but place heavy emphasis on the following report. If that, too, confirms the recent slowdown in inflation, bonds could exhibit a much larger rally. Stay tuned!

(Click on image to enlarge)

Tweet of the Day

More By This Author:

Fannie And Freddie Add Billions To The Bond Market

Kevin Warsh Or Kevin Hassett?

Warsh Is In The Race: Fed Chair Odds In Flux

Comments

Log in or sign up to join the conversation.