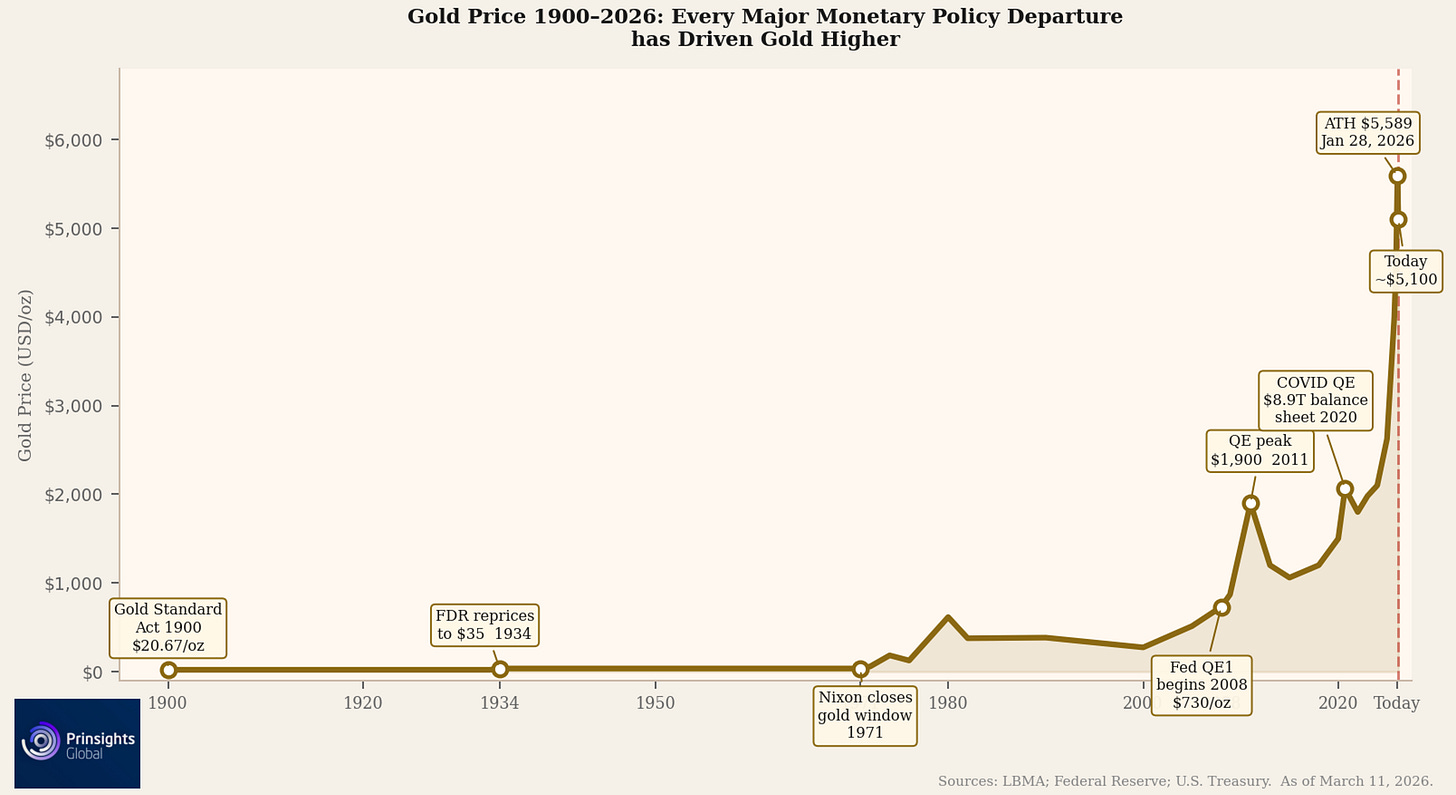

At this time, 126 years ago, President William McKinley, the 25th President of the United States signed the Gold Standard Act into law. The Act fixed the value of one U.S. dollar at 25.8 grains of gold, set the price at $20.67 per troy ounce, and required the Treasury to redeem paper currency in gold on demand.

Gold has been trading at roughly over $5,000 today. That means we have a lot of history to unpack and a lot of policy decisions to account for within that gap.

The Politics Behind the Act

I’ve been deep in the research phase for my forthcoming book, Commodity Wars. The book traces how commodities have underpinned global power structures from the mid-1800s through today. It tells the story of why the geopolitical, economic, and financial moves today all have touchpoints in the commodities sector – and will continue to in the future.

The Gold Standard Act of 1900 is one of the pivotal cornerstones in that history. It is the moment American monetary, currency, and trade policy locked into a framework that defined the next century of global finance.

William Jennings Bryan ran for president in 1896 on a platform of free silver. Farmers across the Midwest and South back then were drowning in debt. At the time, silver was more abundant than gold, and a silver-backed currency would have expanded U.S. money supply and made those debts easier to carry.

Bryan’s Cross of Gold speech to the public went so far as to claim that a tight money supply built on gold was a policy that crushed farmers and enriched creditors. McKinley beat him, meaning that gold won on at the ballot box as well.

The Act that followed fixed gold as the sole basis for the dollar. That meant that every paper note had to be backed by real gold in reserve. The Treasury had to redeem currency in gold coin on demand. That constraint held for 33 years.

In April 1933, President Franklin Roosevelt ordered Americans to surrender their gold at $20.67 an ounce. The Gold Reserve Act of January 1934 then repriced gold to $35, effectively devaluing the dollar by 40% overnight. President Richard Nixon would eventually close the international gold window in 1971. The Fed launched QE after 2008 and again during the COVID-19 pandemic.

Gold rallied on every one of those decisions.

$20.67 to $5,000+

Every major expansion of the Federal Reserve balance sheet since 2008 has corresponded with a sustained gold rally. The Fed’s policy of quantitative easing, what’s known as QE, started in late 2008. Gold ran from $730 to $1,900 by 2011. Turning to the next era, the COVID-driven expansion took the balance sheet above $8.9 trillion and gold crossed a $2,000 threshold.

Gold started 2025 at roughly $2,625. It crossed $4,000 for the first time in October 2025. It would go on to close the year near $4,550. On Jan. 28, 2026, it hit an all-time high of $5,589. It has since pulled back to around $5,100.

The Fed has been reducing the size of its balance sheet through this entire run. Yet gold continued to rally for many reasons.

Foreign holders have pulled back from the U.S. Treasury market, dropping from around 40% of outstanding debt to just above 30%, and since the Iran war began, Treasury selling has only increased. The CBO added $2 trillion to the deficit outlook over the next decade.

Meanwhile, Treasury Secretary Scott Bessent’s plan to pay down the national debt with tariff revenue has run into a Supreme Court ruling, a federal court refund order of up to $175 billion, and a 24-state lawsuit against the backup tariff authority.

The bottom line for the present and continued long-term upside with gold and gold-related companies is that gold is trading as a diversification asset. That’s because it offers stability against the direction of U.S. fiscal policy, debt, uncertainty, and the long-term credibility of the dollar.

What Gold is Telling Investors Now

The structural forces behind this recent period of gold accumulation and price trajectory are a result of conflict-driven uncertainty, fiscal deficits, geopolitical realignment, central bank accumulation, and a Treasury market with less reliable demand than it once had. Those forces are not abating.

As we noted last week, that is why gold has reached its recent levels and why it is only moving up.

Comments

Log in or sign up to join the conversation.