Last Friday, Treasury Secretary Scott Bessent went on Fox Business and said Iran is trying to create economic chaos. He said that the US may “unsanction” hundreds of millions of barrels of Russian crude to stabilize oil markets, in a new policy twist wrinkle on energy dependence and a geopolitical adversary. He also said he strongly believes that tariff rates will return to their old levels within five months.

Now, that is a lot to unpack over the course of just one interview – yet it is what he didn’t say that is more interesting.

Let’s step back and look at what is actually happening in the bigger economic and debt picture, and what it means for US Treasury, debt and gold.

Now, Bessent is simultaneously managing an oil shock from a war that has shut down the Strait of Hormuz, a legal collapse of the tariff framework that was supposed to fund his debt paydown plan, a federal court order to refund up to $175 billion to importers, a new lawsuit from 24 states against the replacement tariff authority – and a stock market that just had its worst week of the year.

And with oil jumping to more than $100 a barrel for the first time since 2022, when Russia invaded Ukraine, and now up well over 30% since the conflict started, the inflation the U.S. Treasury Secretary didn’t want to talk about, and that the White House hope would go away before the mid-term elections, is back at the center of the kitchen table.

Each of those conundrums on its own may be manageable for the White House from a communications strategy standpoint. But for investors, when viewed together, they point in one direction for the dollar and for gold – upward. That’s especially the case if you consider gold’s trajectory since last summer when Bessant spoke about tariff revenue capture and debt paydown. Without those possibilities, gold is an even more meaningful value asset.

What Bessent Was Saying Before This Week and Gold’s Reaction

Last August, Bessent told CNBC the administration was laser focused on paying down the national debt with tariff revenue. At the time, he projected $300 billion a year coming in. The plan was to bring deficits down as a share of GDP and eventually return money directly to Americans.

As we now know, it didn’t quite work out that way – and for a number of reasons.

The Supreme Court struck down those International Emergency Economic Powers Act (IEEPA) tariffs deployed by Trump on February 20th. In that aftermath, Bessent said revenue would be virtually unchanged because of backup authorities. Then a judge ordered that the tariffs collected be refunded and 24 states sued to kill the backup authority, too.

Meanwhile, the Congressional Budget Office (CBO) tabulated the sobering financial standing of the U.S. Primary deficits are now $1.6 trillion higher over the next decade than they were projected to be before the ruling. Add to that $400 billion in additional related interest costs. Throw in the $1 trillion of current annual debt interest payments and this is fiscal quicksand at its most potent.

The near $39 trillion and counting debt paydown story is far from over. Today, the question is how Treasury funds the gap as oil pricing now adds an inflationary layer on top of an already complicated Federal Reserve position. But, in the ongoing fallout, the Fed will have to do something to cover for the Treasury and U.S. debt – leaving it at question whether the central bank holds off on raising rates now. But the Fed still has the ability to try to finesse a backdoor QE. That’s exactly what we are watching for now and specifically why we are monitoring how gold will react.

Why Gold Is The Superior Investment

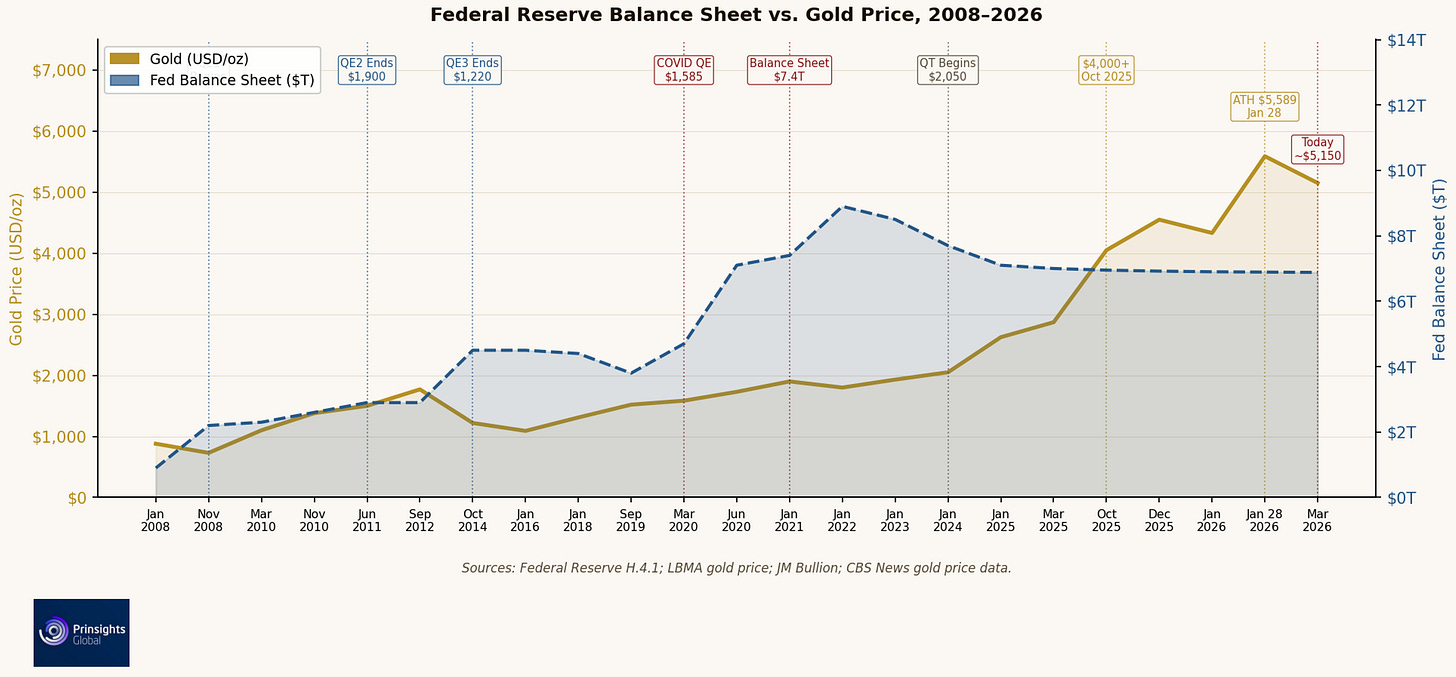

Check out the chart below.

Fed Balance Sheet vs. Gold Price, 2008 through 2026. Sources: Federal Reserve H.4.1; LBMA; JM Bullion; CBS News.

Since 2008 every major expansion of the Fed balance sheet has corresponded with a sustained gold rally. QE1 started in late 2008 and gold rallied from $730 to $1,900 by 2011. The COVID era expansion took the balance sheet above $8.9 trillion and gold above $2,000.

Enter the last year plus and turning to the right side of the chart, we can see what matters now. Gold started 2025 around $2,625. By October, it had crossed $4,000 for the first time. It closed 2025 near $4,550, then ran to an all-time high of $5,589 on January 28th, 2026, driven by the Iran conflict and fiscal deterioration. It has pulled back to around $5,100 as oil and inflation fears create short-term headwinds.

The latest leg of gold’s rally happened during a period of quantitative tightening, not easing, meaning the Fed has been shrinking its balance sheet. Plus, foreign holders have pulled back from the U.S. Treasury market, dropping from around 40% of outstanding debt to just above 30%. That means the Treasury has to issue more debt than projected into a market with less reliable demand than it had before.

What This Means for Investors

Now, the Fed won’t cut into an oil shock. But gold is not trading on the basis of the next Fed meeting. If you’ve been following our analysis of gold’s indifference to recent Fed policy moves, here at Prinsights, you’ll be able to explain why at any dinner party.

Instead, gold is trading against American fiscal and geopolitical policy, and right now that policy direction is pointing toward more debt, more uncertainty and a government managing a tangle of crises all at once.

That is why gold is where it is – and why it’s only moving up over the long-term.

Comments

Log in or sign up to join the conversation.