Image Source: Coya Therapeutics

Introduction

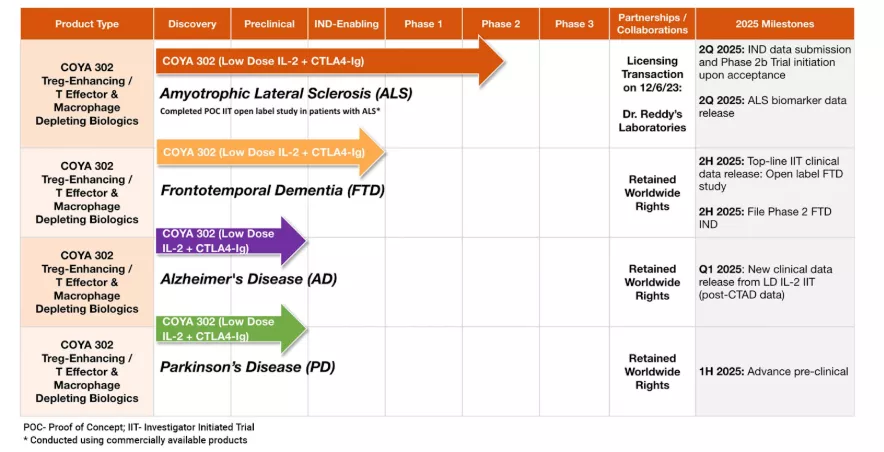

Coya Therapeutics (COYA) is a clinical-stage biotechnology company developing biologic therapeutics for the treatment of neurodegenerative diseases. The company is advancing a pipeline of therapies built on the backbone of Treg-bolstering low-dose interleukin-2 (LDIL-2), which is designed to reduce destructive inflammation both systemically and in the brain, and to restore immune homeostasis. The company’s lead candidate is the combination biologic, COYA 302, which is comprised of LDIL-2 and CTLA4-Ig. This drug is primarily being tested in amyotrophic lateral sclerosis (ALS), with an ongoing phase 2, and in frontotemporal dementia (FTD), both rare neurodegenerative diseases.

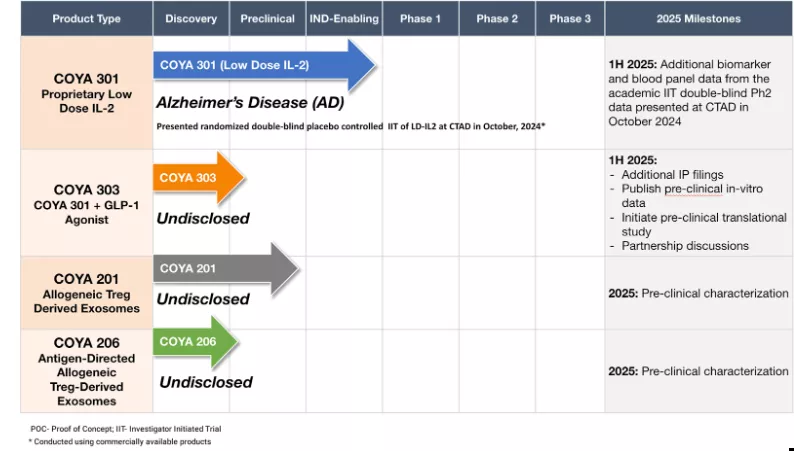

Coya is also building IP to support a combination of LDIL-2 and a GLP-1 agonist (COYA 303), with promising preclinical work supporting this drug cocktail’s potential for neuroinflammatory degenerative disease, which is notable given the rise in popularity of GLP-1 agonists, and obesity and diabetes being comorbid risk factors for Alzheimer’s. Market leading GLP-1’s include Novo Nordisk’s (NYSE: NVO) Wegovy and Ozempic, and Eli Lilly’s (NYSE: LLY) Mounjaro and Zepbound, along with the upcoming retatrutide. To have a chance at competing with these market leaders, companies like Amgen (Nasdaq: AMGN), Pfizer (NYSE: PFE), Roche (OTCMKTS: RHHBY), and AstraZeneca (NYSE: AZN) may look for ways to be a cat in the dogfight—approaching GLP-1s with a differentiated strategy such as combining with LDIL-2 and targeting inflammatory conditions rather than just weight loss.

The company has an active partnership in place with Dr. Reddy’s Laboratories (NYSE: RDY) for the advancement and commercialization of COYA 302 in ALS, and has notable shareholders, including David Einhorn’s Greenlight Capital. Einhorn is notoriously bearish on equities, and his participation as a long-term COYA shareholder is immediately interesting, considering COYA’s relatively small market cap of around $100 million. Both Dr. Reddy’s and Greenlight Capital now have a 5% stake in the company after a recent private placement, where they doubled down after remaining patient shareholders for several years.

I previously outlined how I believe Coya is significantly undervalued, but the investment thesis warrants an update due to notable events in the ALS competitive landscape and recent impactful changes at the U.S. FDA. Before diving into the new details, I’ll summarize the thesis on Coya and what has happened since the last time I covered the company. The bottom line is that the company’s shares remain attractive, and catalysts for a re-rate are increasingly imminent.

Timeline

I last wrote about Coya in early 2024, where I highlighted their potential short path to a potential FDA approval, citing inferior data from competitors that had been able to snag approval. Shortly after I first wrote, the company had inked a partnership deal with Dr. Reddy’s (NYSE: RDY) for COYA 302 (LDIL IL-2 + CTLA-4 Ig), which included a $7.5 million upfront payment and other significant payments upon IND acceptance and trial milestones. Coya subsequently aligned with the FDA on requirements for a Phase 2 trial in ALS and expanded COYA 302’s disease applications to include Frontotemporal Dementia (FTD) and Parkinson’s Disease due to shared immunological dysfunction mechanisms.

In August 2025, the FDA accepted Coya’s long-awaited IND application for COYA 302 in ALS, and the next month, the Phase 2 ALSTARS trial was launched. The submission took well over a year, likely because Coya was generating and submitting required additional non-clinical data (e.g., toxicology, manufacturing, or CMC details for COYA 302) for submission (June 2025) to support their IND. To my understanding, these steps often take longer for combination biologics, as regulators scrutinize safety, dosing, and stability.

The ALSTARS study is a randomized, double-blind, placebo-controlled study (24 weeks, ~120 patients, ~25 centers in US/Canada) evaluating efficacy/safety (ClinicalTrials.gov: NCT07161999). It was accepted as a NEALS-affiliated trial—NEALS is a major ALS research consortium. This helps Coya and its ALSTARS trial via access to NEALS experts/leading ALS investigators and study sites, and the trial visibility.

On January 20th, 2026, CEO Arun Swarminathan communicated in a recent letter to shareholders that the company is targeting full enrollment in the second half of 2026, with a topline readout expected in Q1 2027. Coya’s cash runway has been extended into 2H 2027, positioning the company and stock strongly for future business development opportunities and a potentially positive stock reaction to top-line phase 2 results.

Also in January the company released positive results from an investigator-initiated open-label study of nine FTD patients, showing Treg enhancement and cognitive stability over 6 months. The FDA also accepted an IND for COYA 302 in FTD, opening the door for Coya to plan a phase 2 trial.

About COYA 302

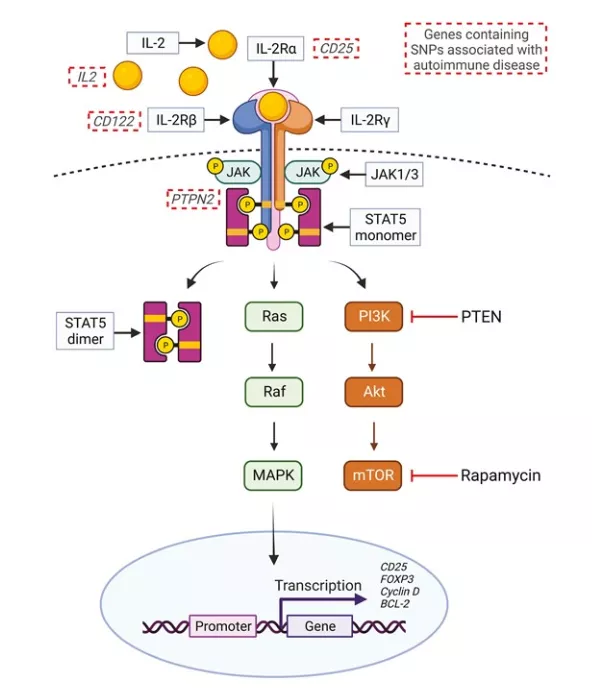

Coya’s lead therapeutic candidate, COYA 302, consists of low-dose interleukin-2 (LDIL-2) and CTLA4-Ig (abatacept). In this section, I’ll dive a bit deeper into the drug mechanisms to explain why I believe these drugs should work well together.

The LDIL-2 component promotes the expansion and survival of regulatory T cells (Tregs), which help maintain immune tolerance to self-antigens and balance inflammatory interactions. Practically, this should translate to preventing autoimmunity, allergies, and chronic inflammation.

The CTLA4-Ig component of COYA 302 suppresses systemic inflammation by targeting activated monocytes, macrophages, effector T cells, and pro-inflammatory cytokines. This also presumably helps maintain an in vivo environment with less proinflammatory signals where Treg expansion is not relatively impaired.

These two mechanisms were combined to work synergistically to induce immune homeostasis and reduce chronic neuroinflammation. Specifically, the drugs together 1) limit microglial/macrophage damage to neurons while 2) improving Treg immunosuppressive capacity.

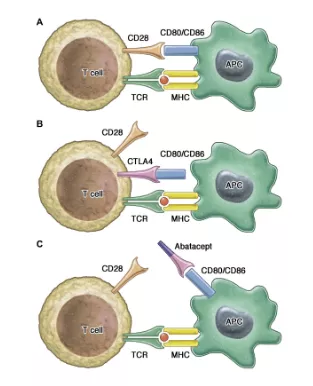

CTLA4-Ig

CTLA4-Ig selectively binds to CD80/CD86 on antigen-presenting cells (APCs, including macrophages) and prevents CD80/CD86 from binding to CD28 on T-cells, which is necessary for full T-cell activation. Additionally, CTLA4-Ig promotes an M2-phenotype (anti-inflammatory, reparative) macrophage. The T cell interaction is shown below.

The new quest in CTLA-4 insufficiency: How to immune modulate effectively?

It is also possible that abatacept’s immunosuppressive capacity fosters an environment where LDIL-2 can more robustly expand Tregs, due to the reduction in inflammatory cytokines and signaling, allowing Tregs to grow in number and increase their suppressive capacity, all while avoiding Teff expansion through CD80/86 blockade.

LDIL-2

IL-2 expands Treg and Teff cell populations. Tregs have a much higher affinity for IL-2 compared to Teff (i.e., a 100x lower threshold to respond to IL-2), so low doses of IL-2 selectively expand Tregs and induce an immune-tolerant state.

The Synergy

However, inflammatory signaling (IL-6, IL-12, IL-1-b, and TNF-a) promotes differentiation of Teff (or Th17 Tconvs) over Tregs, so CTLA4-Ig helps reduce the already-existing chronic inflammation (in the case of ALS, or other diseases with chronic inflammation or autoinflammation), covering LDIL-2’s theoretical “weak spot.” Interestingly enough, CTLA4-Ig reduces Treg activity in addition to Teff activity, but IL-2 can sustain Tregs (STAT5 signaling) even in the context of CTLA4-Ig, covering CTLA4-Ig’s theoretical “weak spot.”

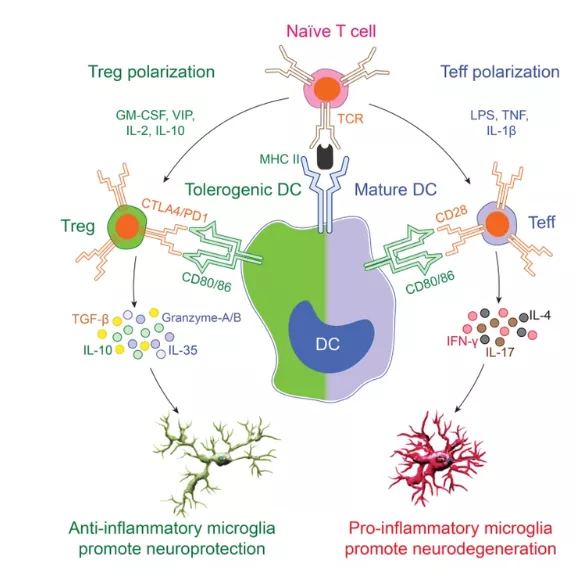

The Pivotal Role of Regulatory T Cells in the Regulation of Innate Immune Cells

(Abatacept reduces the promotion of right side polarization, and IL-2 promotes left side polarization.)

Notably, costimulation blockade (CTLA4-Ig, which blocks CD28 to CD80/CD86 interaction) plus IL-2 has been shown to sustain Tregs, but not Tconv/Teff.

“The detrimental effect of CTLA-4-Ig on Treg homeostasis reflects the importance of CD28 signaling for the maintenance of this population10,19. Treg homeostasis is also controlled by IL-2 signaling, however the relationship between CD28 and IL-2 in maintaining Treg populations has not been fully explored. In this study, we tested whether provision of low dose IL-2 could prevent the Treg impairment associated with blockade of the CD28 pathway. We show that provision of IL-2 can compensate for costimulation blockade in Treg, but not Tconv”

In other words, CTLA-4-Ig can negatively affect both Teff/Tconv and Tregs, and the LDIL-2 compensates for and overcomes the negative impact of CTLA-4-Ig on Treg proliferation, specifically. CTLA-4-Ig alone would reduce both Teff and Treg populations, but IL-2 reverses this and preserves and amplifies Tregs.

IL-2-based approaches to Treg enhancement

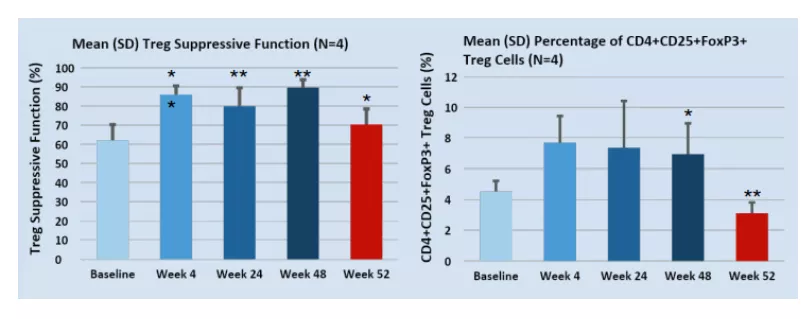

Since IL-2 is required for Tregs' sustenance, it is unlikely that terminating COYA 302 therapy will result in long-term disease stabilization. This is consistent with what has been measured in Coya’s initial LD IL-2 + CTLA4-Ig Investigator-Initiated Clinical Trial in ALS, where, after dosing was terminated at 48 weeks, Treg suppressive function and population fraction decreased.

ALS Etiology and Immune Dysfunction

ALS is a neurodegenerative disease that typically leads to deadly paralysis in 2-3 years after the onset of symptoms, due to the cumulative loss of motor neurons. The precise pathophysiological mechanisms that cause ALS have not yet been determined; however, mechanistic theories include immune disorder, redox imbalance (oxidative stress), glutamate excitotoxicity, disordered iron homeostasis, and dysfunction of autophagy. Several theories postulate dysfunction within the central nervous system, while others propose dysfunction at the CNS periphery, where the immune system attacks motor neurons.

Only two drugs are fully FDA-approved for the treatment of ALS. Sanofi’s (Nasdaq: SNY) riluzole inhibits glutamate and has been shown to extend survival by just 2–3 months in clinical trials, though real-world evidence has shown this life extension benefit to be 19 months or more. Mitsubishi Tanabe Pharma’s (OTCMKTS: MTZPY) edaravone is an antioxidant that does not extend lifespan (or perhaps it extends lifespan minimally), but it reduces ALS symptoms. Both drugs come with significant side effects.

The immune dysfunction theory in ALS is particularly interesting because it intersects or overlaps mechanistically with other ALS theories, including oxidative stress and glutamate toxicity. Notably, chronic inflammation causes chronic increased oxidative stress due to the production of reactive oxygen (and nitrogen) species (ROS) by immune cells such as macrophages and neutrophils. ROS produced from the immune system are intended to kill pathogens but also damage tissue, eventually overwhelming the body’s antioxidant capacity. On the other hand, chronic inflammation can initiate or exacerbate glutamate excitotoxicity by stimulating glial cells to release excess glutamate while simultaneously impairing its clearance.

The main genetic mutations associated with ALS also appear to relate to inflammation:

- SOD1 is responsible for processing free radicals (which are produced during an inflammatory response, among other sources).

- C9orf72 is essential for immune homeostasis.

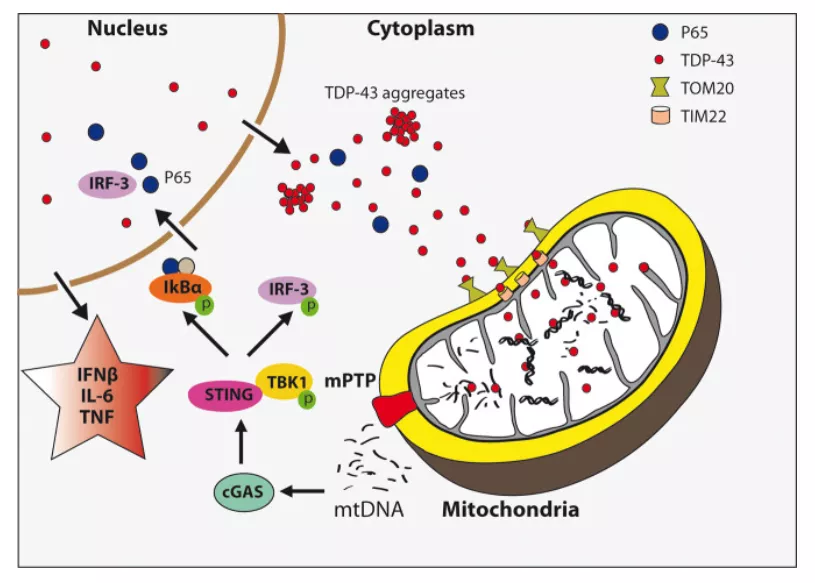

- TARDBP (TDP-43) and FUS is a bit more: when TDP-43 misfolds and enters mitochondria, it forces open a pore (mPTP) that allows mitochondrial DNA (mtDNA) to leak into the cell's cytoplasm. The cell mistakes its own leaked mtDNA for a viral infection, activating the cGAS/STING pathway. This triggers a type I interferon response. TDP-43 aggregates can also be internalized by immune cells and treated as foreign antigens, activating both innate (e.g. macrophages/microglia) and adaptive immune cells (e.g. T-cells). Notably, TDP-43 aggregation is observed in 97% of ALS cases and links mitochondrial dysfunction, aggregated proteins, oxidative stress, and inflammation.

Inflammation is present in sporadic and familial ALS cases.

TDP-43 triggers immune response via mitochondrial DNA release

In my prior article, I noted that:

Increasing evidence supports autoimmune mechanisms driving pathogenesis in ALS, including but not limited to T-lymphocytic infiltration in the anterior horn of the spinal cord (where the motor neurons that die are located), circulating immune complexes, association with other autoimmune conditions, and high frequency of specific MHC types. Additionally, immunoglobulins from ALS patients have been shown to cause apoptosis of motor neurons in vitro as well as cause degeneration of motor neurons in vivo [suggesting an autoimmune component]. In ALS, Treg effectiveness is impaired, with greater Treg function correlating with disease burden and rapidity of progression. These studies at the very least show the contribution of inflammation in ALS. Therefore, it's no surprise that COYA 302 could compare favorably to existing marketed drugs.

As riluzole and edaravone are often prescribed together, COYA 302 represents a new drug mechanism that may either synergize with these existing drugs or act on its own.

Comparing COYA 302 to FDA-Approved Qalsody

COYA 302 may be able to garner accelerated approval (for SOD1 mutant cases only) due to precedent set by Biogen’s (Nasdaq: BIIB) Qalsody, which gained accelerated approval in 2023, as well as new FDA initiatives, which I’ll cover in a subsequent section.

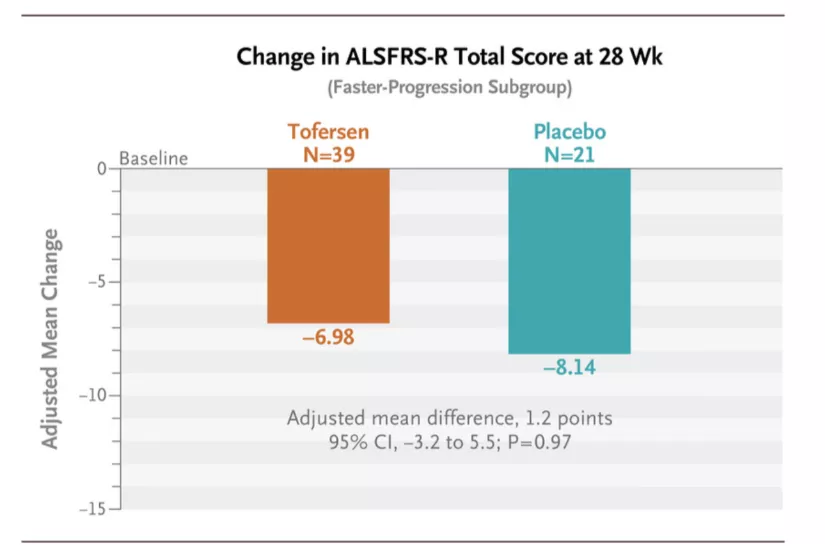

Qalsody (tofersen) is a genetic therapy that targets SOD1, one of the most common mutations in ALS, was approved based on neurofilament chain light (NfL) reductions, a biomarker for axonal injury and neuronal degeneration. As a side note, Coya expects to publish longitudinal ALS biomarker NfL and oxidative stress markers in Q1 2026. As for Qalsody, the drug managed to slow the disease modestly, which was not statistically significant, but since high NfL is considered a leading indicator for symptoms that manifest before disease progression, there may be a future measurable difference between drug and placebo arms in ALSFRS-R scoring. While price estimates vary, the drug was expected to sell for less than $200,000 annually, with peak sales estimated around $300 million despite SOD1 mutations causing about 2% of ALS cases.

Trial of Antisense Oligonucleotide Tofersen for SOD1 ALS | NEJM

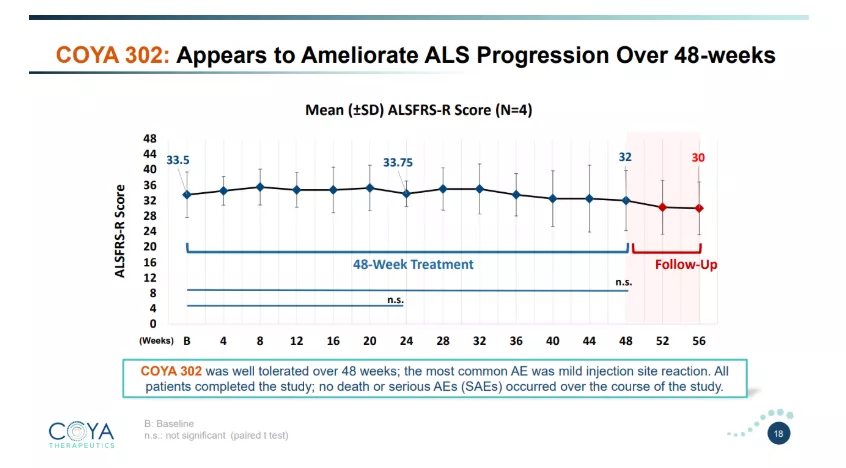

Coya’s clinical data, while only a very small sample size at this time, is considerably better than Biogen/Ionis’ (Nasdaq: IONS) Qalsody data. The average patient’s ALSFRS-R score fell by only 1.5 points over the course of almost 12 months (48 weeks), while the average ALS patient is known to decline at 1.02 points per month. For reference, patients on Qalsody experienced a decline of 6.98 points in 24 weeks, of about 5.5 months. Coya’s data in comparison is nearly a halt in disease progression. Adding to the promising evidence was that patients started normally declining in function immediately after stopping COYA 302 therapy, and that these improvements correlated well with measured Treg numbers, suppressive function, and other biomarkers.

Coya Investor Presentation

If clinical results are near-replicated in the upcoming phase 2 readout, along with promising biomarkers (potentially NfL), I speculate that COYA 302 may appear to be a far superior drug than any of the competition and could be heading for accelerated approval.

Adding to Coya’s clinical evidence is Alzheimer’s data published in 2024, which also showed stabilization of cognitive decline as measured by ADAS-Cog and CDR-SBr. While the initial data and reductions of key cytokine biomarkers look promising, the duration of this Alzheimer’s study arguably falls within a placebo response treatment duration window. The company also gathered some data suggesting that IL-2 cycling less often (or with lower dose) may improve responses.

The company also has promising data in yet another neurodegenerative disease: frontotemporal dementia (FTD), with 22 weeks of COYA 302 therapy resulting in unchanged MoCA and CDR-FTLD scores, which is consistent with disease stabilization observed in both ALS and Alzheimer’s patients.

The totality of data Coya has generated is consistent and positions COYA 302 to be significantly superior to existing ALS therapies, in my opinion.

Competition Dwindles

Sadly for patients, the competitive landscape has also withered away. While Amylyx Pharmaceuticals’ (Nasdaq: AMLX) ALS treatment, Relyvrio, was granted FDA approval in 2022, in 2024, the drug failed a phase 3 trial. The company’s market cap lost $1 billion when the news broke. As I covered in my prior article, the company’s drug, Relyvrio, had a very modest efficacy as measured by phase 2, which later proved to be equivalent to placebo in the phase 3 PHOENIX trial. As such, one leading competitor has fallen away from the landscape. This example serves to show the value of an ALS drug that was approved (but still under question, and with a mechanism that was never fully understood). This stands in stark contrast to COYA 302, which has a well-defined mechanism of action targeting understood cellular and molecular dysfunction in ALS.

Regulatory Changes at the FDA May Benefit Coya

This contrast in well-defined disease mechanisms is relevant to the recent changes in approach at the FDA regarding rare diseases and significant unmet medical needs, since the new presidential administration has taken the reins.

FDA Commissioner Marty Makary's reforms are intended to result in faster approvals, reduced regulatory burdens, and leverage real-world evidence and innovative development and analysis methods. Several of these reforms have potential implications for COYA 302.

First, in December 2025, Makary announced the formation of a new standard requiring one pivotal clinical trial by default for most drugs and medical products to pursue FDA approval, with two trials required only in select cases. Updates to actual policies/guidance are expected in 2026.

Additionally, the FDA’s Plausible Mechanism Pathway was launched in November 2025 for ultra-rare diseases and is designed to allows drug approvals for rare and serious diseases where populations are so small that they can’t be feasibly studied in clinical trials. This new pathway requires a therapy's direct targeting of a known biological abnormality, supported by mechanistic data, biomarkers, and/or small datasets rather than large randomized controlled trials for. While ALS may or may not fit into this category given its a rare disease but there are thousands of cases per year in the United States, it shows FDA/CDER’s break from old school rigidity that was in some cases not serving patients’ needs, while also not necessarily protecting them from needless risks. BioPharmaDive notes that “the new framework could also apply to common conditions with no’proven alternative treatments’ or in cases where new therapies are sorely needed.” While initially focused on ultra-rare or personalized genetic therapies, its principles align with broader FDA reforms for orphan diseases like ALS.

Key requirements and how COYA 302 may fulfill these criteria are as follows:

1) A clear causal link between the disease's abnormality and the therapy's action:

ALS etiology involves dysfunctional regulatory T cells that fail to suppress chronic neuroinflammation, leading to oxidative stress, microglial activation, and motor neuron degeneration. This impairment is a multifactorial driver in both sporadic and familial ALS cases, with reduced Treg numbers and suppressive function directly contributing to disease progression. COYA 302 addresses this head-on, establishing the required "plausible" and direct mechanistic connection.

2) Direct targeting of the abnormality:

The therapy's dual immunomodulatory approach restores and sustains immune balance. This isn't indirect symptom management or therapy with a poorly characterized therapeutic mechanism; it is a targeted intervention for Treg dysfunction, aligning with pathway demands for therapies that act on the root molecular/cellular issue. Since ALS doesn’t have a singular known cause, this is about as good as it gets for targeting a root cause.

3) Supporting evidence from preclinical models, biomarkers, pharmacodynamic data, or small clinical datasets:

Coya has demonstrated COYA 302's efficacy through preclinical and early clinical studies, including proof-of-concept data showing Treg suppressive function improving over the therapy duration, alongside reduced oxidative stress markers, and these biomarkers accompanied a clinical outcome: reduced ALSFRS-R decline. Biomarkers like neurofilament levels and cytokine profiles in ALS specifically may further validate the Treg-based mechanism.

4) Applicability to conditions where traditional trials are infeasible due to small patient populations:

ALS qualifies as a rare, fatal, and debilitating neurodegenerative disease with no cure and high unmet need, prioritizing it under the pathway's focus on severe conditions, even though, compared to some ultra-rare diseases, ALS is more common. Additionally, Coya’s early data show meaningful clinical improvement above expected variability despite such a small sample size.

Overall, this mechanistic foundation positions COYA 302 for potential accelerated review with robust post-approval data collection to confirm long-term benefits (where Amylyx failed). Regardless of whether accelerated approval becomes an option, the regulatory landscape is evolving in a direction that could benefit Coya.

Company Finances

Coya had $28.1 million in cash as of September 30, 2025, and just raised $11.1 million from the aforementioned private placement (Dr. Reddy’s, Greenlight Capital). With the company spending $12.1 million in the trailing twelve months (Cash from Operations), they have a robust balance sheet to fund the company well past the ALS phase 2 readout, and potentially the cash to plan and start phase 2 trials in FTD or Alzheimer’s, especially if they can ink another partnership deal to help fund these efforts.

Approximate Valuation

Relyvrio was forecast to reach peak sales of over $1 billion, and achieved first full year sales of $380 million before it was pulled off the market. This remains the best comparison of what a new ALS therapy can achieve, and in this case, despite just accelerated approval and questionable efficacy. I believe COYA 302 will prove to be a more robust therapy and will assign a greater peak sales figure. Roughly 30,000 people have ALS at any given time in the United States, and about 5,000 cases are diagnosed every year. A robust therapy such as COYA 302 could easily garner a 30% market penetration given the direness of the disease and a possible market-leading efficacy profile. At a $100,000 annual treatment cost, this translates to $900 million in revenue. The thing is, COYA 302 has been shown to nearly halt ALS progression in early studies. If this holds in the phase 2 readout, the number of people with ALS could grow significantly, as death could be delayed significantly. In this case, would the peak sales figure double? It’s hard to say, but a better treatment should have a higher peak sales estimate.

Settling on just $1.2 billion and assuming a 30% chance of phase 2 success and a scenario of 50% chance of accelerated approval with a 13% overall royalty rate, I arrive at revenues of $23.4 million. Using a P/S ratio of 15 (high margins), I arrive at a valuation of $351 million for Coya’s royalties. Adding in the $677.25 million in sales-based milestone payments (also risk-discounted) brings the value up to $453 million. This appears reasonable given Amylyx lost $1 billion in value after its drug was voluntarily pulled from the market.

For reference, Coya had 20,924,456 shares outstanding as of their Q3 2025 report, with 814,444 warrants and 3,021,238 options outstanding. Since then, the company sold 2,522,727 shares in its private placement. This should bring the fully diluted share count to 27.28 million.

Using a fully diluted share count, my valuation estimate would be $16.60 per share. This happens to be in line with current analyst target prices. There are a range of outcomes for the stock based on clinical results, future endeavors (e.g. FTD) gaining traction, and potential additional partnerships, along with regulatory unknowns.

Risks

Coya is a developmental stage biotechnology company, which always includes the risks of dilution and funding concerns (which have been minimized near-term), clinical study disappointments, and various regulatory risks. Optimism surrounding Coya’s promising ALS program is based on two very small clinical studies with robust results. While there aren’t a lot of risks specifically with Coya compared to other pre-revenue biotech companies, risks like clinical trial results can be practically binary outcomes for biotech stocks and investors should be aware of these potential abrupt moves.

Conclusion

Overall, I believe Coya’s stock is drastically undervalued and that potential catalysts for the stock are not only phase 2 data, but also additional business developments or clarity on a regulatory path that will enable people to envision what the future looks like for the company. The company has been a good steward of shareholder capital, and they appear to have a good partners and investors. Early data is excellent, and the potential for their pipeline to grow is great with additional partnership interests or capital infusions. It is no wonder legendary investors such as Einhorn are involved here. I would not be surprised to see the stock much higher than it is now at the end of 2026 due to business development activities or as investors anticipate the upcoming phase 2 results expected in early 2027.

More By This Author:

5E Advanced Materials Poised For Rerated Valuation As Critical Mineral Producer

Groundbreaking Early Readout For Gain Therapeutics Gives It A Shot At First Disease-Modifying Drug For Parkinson’s

ZenaTech Poised For Growth With String Of Acquisitions And Regulatory Clarification

Comments

Log in or sign up to join the conversation.