Image Source: Pixabay

It has been a while since I covered Gain Therapeutics (Nasdaq: GANX), currently one of my favorite picks in the small biotech market, along with Galectin Therapeutics (Nasdaq: GALT), which I covered several months ago. Both companies are developing what I believe to be significant medical breakthroughs with multi-billion-dollar commercial opportunities.

Since I last covered Gain, the stock has struggled through the end of the worst biotech bear market ever (~2021-2023) and several painful financing rounds, but has continued to generate impressive preclinical and clinical data that, in my opinion, has far exceeded expectations. As such, I have never been more confident that Gain has caught “lightning in a bottle”... at least I am as optimistic as one can be in any pre-revenue microcap biotech company. I believe that Gain Therapeutics is easily worth an order of magnitude more than its current market capitalization and represents a compelling investment opportunity, albeit not without significant risks associated with being a mid-early clinical-stage biotech company.

Summary of Gain Therapeutics

Gain Therapeutics is a clinical stage biotechnology company developing therapies for unmet medical needs, particularly drugs that are allosteric small molecules developed by its Magellan (formerly SEE-Tx) physics-based and AI-enhanced drug discovery engine. Its lead drug candidate, GT-02287, is being developed as potentially the first disease modifying drug for Parkinson’s Disease, and the company has several other promising allosteric drugs in its pipeline that were also discovered through the Magellan platform. Parkinson’s Disease is a multi-billion dollar market with great commercial potential for any company that can develop a disease-modifying drug that can significantly impact patients’ lives above and beyond the drugs that are prescribed today that only help manage symptoms, and hardly even delay the inevitable cognitive and systematic decline that plagues so many patients.

The History of Gain Therapeutics’ Journey

Gain initially focused on lysosomal and rare diseases, and the company went public several years ago just before the biotech and small-cap markets spectacularly collapsed, which was a double whammy for fundraising-dependent pre-revenue biotech companies. However, the development of GT-02287 through this difficult time has been incredibly positive.

About GT-02287

GT-02287 is an allosteric modulator of the enzyme glucocerebrosidase (GCase) that is designed to stabilize GCase during its translation and to essentially enhance or fix deficient endogenous GCase—in other words, to make GCase work when it does, such as when one has a genetic mutation rendering one’s GCase ineffective.

Initial Focus - Genetic Lysosomal Disease

The compound was initially designed for Gaucher’s disease, a genetic lysosomal disease caused by GBA1 mutation (which encodes GCase) with a significant unmet medical need. However, as GCase became a focus in Parkinson’s disease (PD) with GBA1 as a leading genetic risk factor for Parkinson’s, the company shifted its focus, rightly so, towards the much greater commercial opportunity of Parkinson’s disease—a market with billions in commercial opportunity and more likely to attract investor interest.

A Pivot to Parkinson’s—Greater Risk… but Far Greater Reward

The main risk that could mute the potentially massive upside of developing a disease-modifyig PD drug was that there was a chance this drug would only work really well in Parkinson’s patients with the GBA1 mutation (approximately ~10-14% of the Parkinson’s population). This logic lies in the fact that its more likely that GBA1 mutant PD patients had disease driven by GCase defieciency versus idiopathic PD patients' disease driven by other factors, and only resulting in less severe GCase deficiency. However, there was a chance this genetic-focused therapy would work as GCase deficiency forms a feedback loop with 𝛼-syn oligomers, the hallmark of PD.

In a normal scenario, soluble alpha synuclein is degraded by a cell’s lysosomes. In Parkinson’s (and Gaucher’s Disease), 𝛼-syn oligomers form as a result of a dysfunctional lysosome (GCase deficiency), and these oligomers further impair GCase production and delivery (to mitochondria and lysosome), leading to an amplified dysfunctional state. Thus, there was hope that GT-02278 might show efficacy in idiopathic PD by correcting this disease feedback loop.

Gaucher Disease Glucocerebrosidase and α-Synuclein Form a Bidirectional Pathogenic Loop in Synucleinopathies (Cell. July 5, 2011.)

Since GCase is understood to be deficient in idiopathic PD patients, too, this approach was promising. However, it remained to be seen if active GCase levels could be restored in idiopathic PD patients, and if that restoration would translate into a clinical effect—there were significant of unknowns. However, the logic behind the theory that this drug could work across the PD common genetic variants, including idiopathic PD patients, was relatively solid.

Gain’s Data Repeatedly Surpasses Expectations

Gain has released several rounds of preclinical study data and clinical data in the past few years that has, at every turn, exceeded my expectations. In my opinion, since writing about Gain in 2023, the company has continued to knock it out of the park with every new dataset it has generated.

Several preclinical studies that Gain conducted showed immense promise, but these studies were essentially PD models induced by GCase impairment (either genetically (GBA1) induced, or Conduritol-β-epoxide (CBE) induced, as CBE irreversibly binds GCase at its active site). In my opinion, correcting the exact problem created in a preclinical model shows that the drug (in this case, GT-02287) does what it was designed to do (rescue GCase from a dysfunctional state), but does not answer the pathophysiological question of whether correcting GCase activity can have a clinical impact on Parkinson’s, which may or may not be primarily driven by GCase impairment in actual humans.

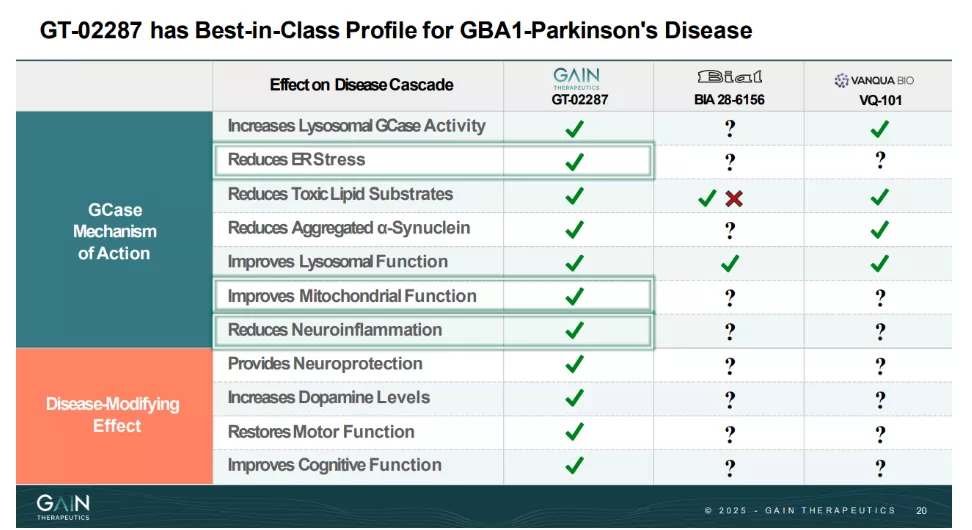

However, two PD preclinical models mimic PD primarily by impairing the mitochondria, the rotenone-induced model and the MPP+ model. First, Gain had previously published data using the rotenone model and also has provided compelling videos of functional (locomotive) improvement with GT-02287 treatment in rotenone-induced PD rodents. I won’t get into the details as I have covered this previously, but ensuring GCase activity is improved in the mitochondria is one of the things Gain’s competitors don’t appear to be able to do (no data, but theoretically they cannot either), and one of the main reasons I think Gain’s drug is superior.

Gain December 2025 Corporate Presentation

Gain’s New Parkinson’s Data

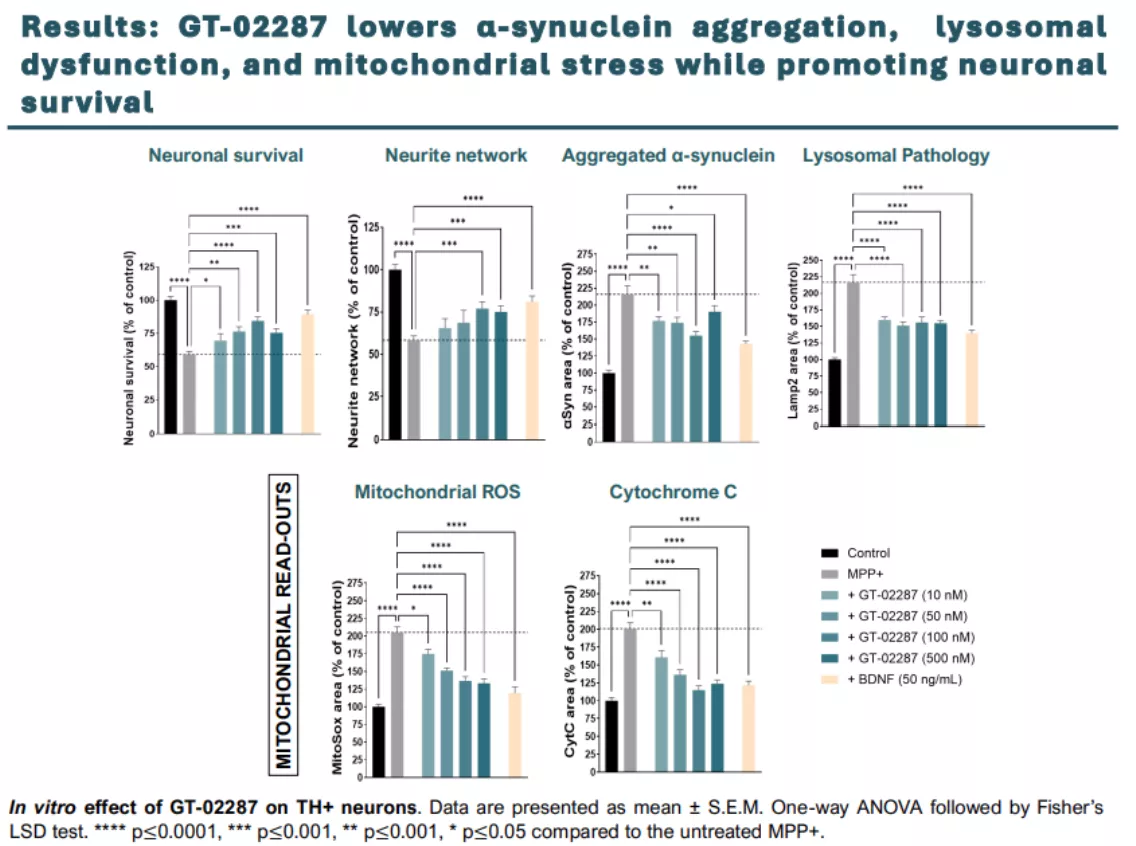

More recently, the company tested GT-02287 in a preclinical model that used cultured rat mesencephalic dopaminergic neurons, impaired with a mitochondrial toxin, MPP+. This is a common PD model, but it isn’t a GCase or GBA1-based model, so any therapeutic effect would lend more credence to GT-02287 addressing underlying PD pathophysiology rather than correcting the exact pathway used to mimic PD (as in fixing GCase after… impairing GCase). The results were noteworthy, with GT-02287 protecting neurons and their mitochondria from the mitochondrial complex 1 impairment induced by MPP+.

GT-02287, a Clinical-State Allosteric GCase Modulator for the Treatment of Parkinson’s Disease, Protects Dopaminergic Neurons Against Mitochondrial Toxin MPP+

These results reinforced the findings of a prior in-vivo study (2024) on C57BL/6 mice where the mice were induced with Parkinson’s using CBE (a potent, irreversible GCase inhibitor) and alpha-synuclein preformed fibrils. Days after inducing Parkinson’s, GT-02287 was administered, and it impressively completely restored motor function as measured by wire hang test (i.e., complete restoration of Parkinson’s).

These results greatly impressed me and were the first hint that this drug could potentially work wonders in real Parkinson’s, but my one small reservation with this study was that it was a GCase/GBA1-induced model. However, the findings of the aforementioned MPP+ model complement this study’s primary shortcoming, and together gave great confidence—as great as preclinical evidence can provide—that the company may have caught “lightning in a bottle.”

These preclinical data still do not fully answer the question of whether GT-02287 would work clinically, especially in idiopathic PD patients. Do these diverse preclinical models, in aggregate, accurately mimic real Parkinson’s disease?

Gain’s Clinical Data

Gain released data from its dose escalation cohorts in its phase 1 trial, where the drug was able to increase GCase by an average of 53% across several healthy volunteers. It was expected that endogenous homeostatic feedback mechanisms would prevent GCase from being increased in those patients where it may not have been impaired, but it appears that even in healthy people, GCase can be “turned up” with this drug.

Gain Therapeutics’ December 2025 Corporate Presentation

Where GT-02287 really gets interesting is where the initial dose escalation findings were followed by a phase 1 interim readout of clinical outcomes, for some of the patients that had completed the 90-day dosing. Many of these patients were of an idiopathic PD genotype—of particular interest to potentially expand the drug’s TAM by a factor of ~8-10x.

Gain Therapeutics MDS-2025 Interim Phase 1b Baseline Demographics

In the interim readout, clinical efficacy was measured via the MDS-UPDRS (Movement Disorder Society Unified Parkinson's Disease Rating Scale). The UPDRS is a 0-4 scoring system (for each question) for Parkinson's Disease motor and non-motor symptoms, and is scored as follows:

- Part I: Mentation, behavior, and mood

- Part II: Activities of Daily Living (ADL)

- Part III: Motor examination”

The company’s readout of MDS-UPDRS scores for nine of the patients included some idiopathic PD patients (highlighted above).

Gain Therapeutics MDS-2025 Interim Phase 1b Data

Considering MDS-UPDRS scores typically increase about 4-5 points per year (studies vary), a decrease of 4.6 points in 90 days represents an obvious treatment effect and what could be a true disease modifying effect, although longer term treatment will be needed to confirm this effect. Additionally, it was mentioned that several patients had their sense of smell return, and it is notable that sense of smell is not a specific item of consideration in MDS-UPDRS, and it is one of the first symptoms of early Parkinson’s, common to a majority of Parkinson’s patients. In my opinion, while keeping in mind that this data is early, it is groundbreaking, especially due to the relative consistency of the clinical responses, with only two patients increasing their scores over the 90 days. One has to ask if these patients simply did not respond to the drug yet, and more time might yield a clinical response.

Every set of data released in the past few years has outperformed my expectations.

Upcoming Data

Gain will release 90-day outcomes data for its full Parkinson’s phase 1b trial in the upcoming weeks/months. Patients with or without GBA1 mutations are being evaluated, and results could fully bridge the gap between all of the impressive preclinical data that has been generated and the clinic. Functional outcomes data will include changes in MDS-UPDRS, a standard physician-reported and self-reported scale for Parkinson’s, and potentially other items like OFF state, and other standard functional scales, including MoCA, ADL, etc. Several biomarkers will be analyzed, including GCase activity, sphingolipids (compounds that GCase breaks down), lysosomal and mitochondrial markers, and inflammatory markers.

GT-02287 is Proof for Magellan Platform

Gain’s potential blockbuster Parkinson’s drug has had impressive performance in the lab and clinic so far. Part of its success is likely attributable to its allosteric design and optimization due to Magellan. Allosteric drugs don’t bind the active site of a protein and, as such, can exhibit better specificity (not binding to similar off-target proteins), translating to better tolerability and potentially better efficacy (allosteric modulators can turn proteins up or down). Several years ago, drug discovery platform companies commanded high market valuations, but these platforms needed to be proven out. Magellan has delivered a potential blockbuster with some of the most impressive preclinical and early clinical data I’ve seen, and so in my mind, Gain’s Magellan platform should command a premium valuation for the company due to its pipeline and that other allosteric drug development companies have been bought for billions (Vividion bought by Bayer (OTCMKTS: BAYRY) for $1.5 billion plus $500 million “biobucks”). Vividion’s most advanced assets are still in phase 1 clinical trials.

Market Potential and Valuation

The company has the potential to generate several billion dollars from a GT-02287. I had previously estimated about $1 billion in peak sales for the drug. However, over the past two years and with the newly generated interim clinical data, I believe that number could now be significantly higher due to pricing power and higher market uptake (Parkinsons population growing from 1 million to 1.2 million by 2030, and a disease-modifying therapy costing tens of thousands annually). During an interview with Lou Basenese, the $5 billion annual sales figure was mentioned.

I assume a $30,000 net price, with a 17% market penetration of the forecast 1.2 million PD patients in the United States. Using a 15% discount rate, 10 years till peak sales, a 3x peak sales multiple, a 20% chance of approval, and 50m shares outstanding, I arrive at a valuation of $18.15 per share. Assuming global sales could approximately double the U.S. peak sales figure, the company would be worth $36.30 per share based on GT-02287 alone. This valuation is roughly 10x the current price, and just shy of a $2 billion market cap, a valuation I don’t believe is an exaggeration.

For comparison, Merck (NYSE: MRK) recently entered into a partnership with Valo Health “to Discover and Develop Novel Treatments for Parkinson’s Disease and Related Disorders,” where “upfront and potential milestone payments [total] up to over 3 billion dollars.” This partnership is simply to generate novel drugs with novel targets (i.e., before the preclinical stage of development). So indeed, this kind of money (<$2 billion) is potentially being spent on simply generating compounds!

Ultimately, I agree with several of the more optimistic analysts covering the stock who have price targets from $8-12/share. As GT-02287 is derisked and more time elapses, my valuation (and even more than my valuation, due to derisking events) could become reality, but this kind of stock rerating is not expected in 12-18 months unless the company is bought out. Given the excellent data, first-to-market potential, a potential groundbreaking step forward for PD patients, and strong economics, I believe a large pharma company will ultimately own the rights to GT-02287, if not Gain, in its entirety. As an aside, CNS/neurology acquisitions overtook oncology's top spot for U.S. M&A this year.

Risk

Despite the excitement with the data, Gain is still a microcap, early-stage, pre-revenue biotech company that requires capital to advance clinical studies. Clinical trials can disappoint, and markets can falter, which could make it hard for the company to raise money. The company doesn’t currently have the money to run a phase 2 trial, but it does have a good amount of cash for overhead for several quarters.

Stock Momentum

I have noticed that Gain is picking up momentum on social media. While its good to maintain a healthy skepticism of social media feuled investing trends (sometimes they’re right, sometimes they’re wrong - notably Elon Musk said during a Tesla (NASDAQ: TSLA) earnings call (January 2020) that retail investors have better insights than institutions), I have noticed that increased awareness on social media for underfollowed companies, particularly ones that I perceive to be undervalued, correlates with chart breakouts and excellent stock performance.

This has been true recently for several companies I own overweight positions in, and have owned positions in years before they became popular. While I’m skeptical of the trendiness of these investments, I have to admit that after these stocks have gained genuine social media traction, many of them are now much more fairly valued than before (ASTS, ONDS, GALT, bought at $3, $1.50, and $4 averages, with approximately 2.5, 3.5, and 8.5 year holding periods, respectively). Thus, while not chasing social media trends, I simply perceive and notice that GANX stock gaining traction on social media may be a sign of price appreciation, if not a direct reason for the stock greatly increasing in value, despite my skepticism of retail investor trends.

For example, Lou Basenese’s interview with Gene Mack was posted on X and has been viewed almost a million times.

Conclusion

The company’s data is excellent and the management team is well respected. Particularly, Chairman of the Board Dr. Khalid Islam has a long track record of successful returns guiding several companies, with the sale of Immunomedics to Gilead (NASDAQ: GILD) for $22 billion and the sale of Gentium to Jazz (NASDAQ: JAZZ) for $1 billion while he was CEO. Gain’s CEO Gene Mack was a successful biotech analyst who understands investors and the capital markets, and especially the value of Gain’s lead program. Oftentimes, with small companies, management is the weak link, but that will not likely be the case with Gain. Management’s dealmaking experience I believe will be exercised in the coming months as additional Parkinson’s data is released and as larger pharmaceutical companies think twice about letting their competitors secure the rights to this potential blockbuster drug.

CEO Gene Mack stated in his interview with Lou Basenese that this is a buy at $10, $15, and $20 per share (paraphrased). With a multibillion-dollar revenue opportunity per year in Parkinson’s, and a potential application in Alzheimer's, as well as Gaucher’s Disease, and Lewy Body Dementia. He was an analyst and knows to always be cautious and never to exaggerate. Although the future is never certain, I don’t believe he is exaggerating.

More By This Author:

ZenaTech Poised For Growth With String Of Acquisitions And Regulatory Clarification

HIVE Digital Technologies: Trading At A Discount To Peers Despite Superior Capital Deployment

Apollo Silver: Two World-Class Silver Assets In One Stock

Comments

Log in or sign up to join the conversation.