TM Editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

OS Therapies (Nasdaq: OSTX) is a microcap biotech company with an immunotherapy platform technology initially targeting osteosarcoma, a rare aggressive cancer that affects children’s bones and requires bone resection or amputation in all cases. The company has a unique value proposition in that its lead candidate, OST-HER2 is already proven in canine osteosarcoma (a common dog bone cancer), and that it will potentially be granted one of the few FDA Priority Review Vouchers upon OST-HER2 FDA approval—these vouchers have recently been sold for nearly $200 million each. With the company’s market cap around $70 million, an FDA approval and granted PRV should completely re-rate the stock, and it would likely be a rapid multibagger. The company is pursuing an Accelerated Approval pathway, and with the final clinical module of the Biologics License Application (BLA) completed in March, an accelerated approval is possible this year.

Background

OS Therapies has developed a very unorthodox way of treating cancer. They take a highly pathogenic bacterium with a 20-30% mortality rate and inject it into the cancer patient with the idea that it's going to jumpstart their immune system into overdrive. On the surface, this sounds like a horrible idea, but there’s a twist that could revolutionize how we treat cancer. The treatment regimen calls for delivering antibiotics 4 hours after administration, which kills off the bacteria before it harms the patient, but after the immune system goes into a vigilant overdrive, ready to seek and destroy the cancer. They do this every 3 weeks for a year. While it sounds extreme/radical, it's one of the most promising targeted therapies developed for pediatric osteosarcoma in the past 40 years without the broad side effects of chemo.

OST-HER2 is actually FDA-approved for dog osteosarcoma, which is similar in many ways to human osteosarcoma, a rare disease often diagnosed in children. The drug is highly effective, with one study showing an increase in median disease-free survival time (time to metastasis) from 123–257 days for standard-of-care (amputation + carboplatin) to 956 days. One and two-year survival rates were drastically improved over the historical standard of care, increasing from 35.4% and 10% to 77.8% and 67%, respectively. This astounding canine data serves as robust preclinical data supporting OS Therapies’ endeavors in moving this therapy through human clinical trials for FDA approval, to bring these life-changing benefits to human children.

OSTX is bringing a radical new rare disease oncology drug through development for FDA approval, and is expected to bring in $500 million in peak sales with OST-HER2 in humans and $150 million from canines, with the listeria immne-stimulating platform paving the way to a broader cancer franchise. With the company bouncing off a technical bottom and headed toward a potential early approval in 2026, OSTX shares are attractive.

There is also an approval tailwind supported by a strong osteosarcoma advocacy group and the new FDA commissioner, Marty Makary, who continues to push for faster approvals in orphan drugs and who pushed even harder for approvals for therapies treating deadly pediatric cancers. The rising tide in Priority Review Vouchers (PRV), estimated to each be worth over $200 million, is also helping push the valuation higher. The icing on the cake could be label expansion to treat other diseases, as HER2 is a common cancer target.

OST-HER2: Antigen Supercharger

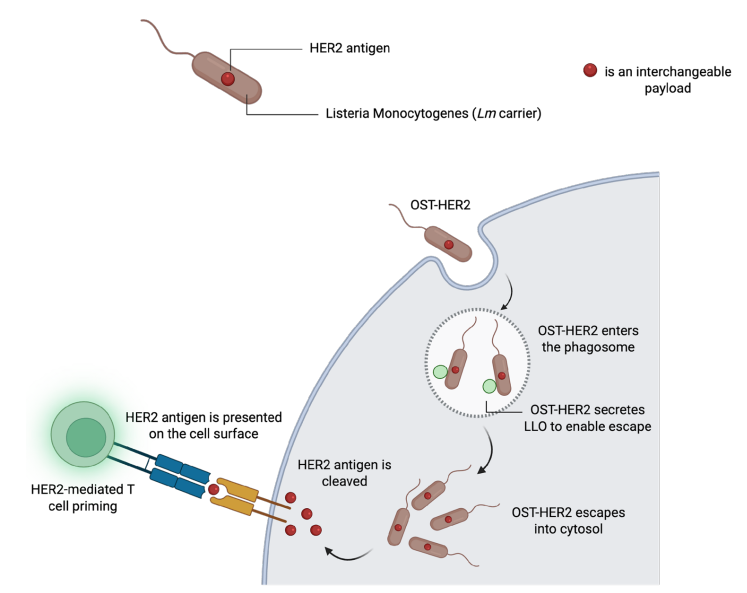

OST-HER2 is an immunotherapy targeting the HER2 marker. However, in contrast to targeted therapies, it does two things at once: it stimulates the immune system and it forces immune cells to recognize HER2 antigens.

The treatment delivers HER2 to immune cells using a weakened and modified version of the bacterium Listeria that is naturally attracted to macrophages, which are known for engulfing pathogens and destroying them. The modified bacteria carry the HER2 protein into the macrophages. Once inside, the HER2 pieces get broken down and then presented on the cell surface so other immune cells can see and be activated against HER2. Basically, the Listeria is used to create a robust HER2 antigen presentation (showing other immune cells what they should react to—HER2), and to simultaneously wake up the rest of the immune system, to create a fully-fledged immune response.

Source: OS Therapies Investor Presentation

After the shot, immune cells show the HER2 pieces (i.e. antigens) to T cells, which then start a chain reaction that helps kill HER2+ tumor cells and can reveal other cancer targets/antigens. In studies with dogs (118 animals), the treatment was safe and showed immune signs linked with long disease-free periods. Human phase 2b results also matched those immune signs. There are no FDA-approved immunotherapies for pediatric osteosarcoma (pOS), so OST-HER2 could not only be a great step forward in pOS treatment—it would also be a new first-in-class option.

The Listeria delivery mechanism that OST-HER2 is based on is also a platform technology, meaning the same approach can be used to deliver other tumor markers besides HER2. For example, the company’s OST-504 program, which targets PSA and some other antigens for treating prostate cancer has Phase 1b data due this quarter; a good result there would strengthen the platform’s value and could attract partners or buyers from bigger drug companies.

Compelling Clinical Data

The key to a successful cancer trial is to show a survival benefit. In October 2025, Phase 2b results showed a 75% survival rate at 2 years compared to the 40% historical rate (p< .0001) in recurrent, resected pulmonary metastatic osteosarcoma. In the trial, there was a subgroup of patients who completed their therapy and then for a period of 12 months didn’t show any signs that the cancer came back. This is called 12-month Event Free Survival (EFS) and 100% of this subgroup achieved 2-year overall survival. These data show the durability of the response and earned them a Rare Pediatric Disease Designation (RPDD), Orphan Drug, and Fast Track designations and demonstrated a statistically significant survival benefit in a Phase 2b clinical trial.

According to OS Therapies, comparative oncology studies have shown that there is a 96% genetic homology between canine osteosarcoma and human osteosarcoma. This means that canine osteosarcoma is an excellent predictor of human osteosarcoma. The Canine precursor trials (118 dogs) validated the drug’s immunogenicity with the best survivors showing elevated IL-6/TNF-α responses. These results informed human biomarkers, and also due to these results, OST-HER2 holds USDA conditional approval for veterinary use.

For 40 years, there have been no advancements in treatment for a rare pediatric disease called osteosarcoma that has been affecting children. This is the poster child of new treatments the FDA appears willing to approve under a more accommodating FDA with respect to orphan drugs approval. This therapy targets diseases with great unmet medical et medical needs to patients, like pediatric orphan drugs, and even more recently, groundbreaking psychedelic drugs for devastating, difficult to treat, and complex psychiatric conditions. The FDA has also recently indicated it will pursue real-time clinical trials and Bayesian methodology to help accelerate drug development. This change in momentum at the FDA underscores its open-minded and practical new approach to drug development and approval.

As a side note, the safety profile is excellent, with the company’s phase 1/2b trials reporting no severe (grade 4 or 5) toxicities.

Historical Context: OST-HER2 Versus Prior HER2-Targeting Approaches

You might be wondering why this listeria-based approach is used instead of well known HER2-targeted monoclonal antibody therapies such as the widely used trastuzumab, sold by Roche (OTCMKTS: RHHBY) or trastuzumab deruxtecan sold by AstraZeneca (NYSE: AZN). The answer is that this approach must be more robust as the former monoclonal antibody HER2 therapies have largely failed in osteosarcoma. This is probably due to biological and technical mismatches with how HER2 works in osteosarcoma versus breast/gastric cancer where these monoclonal antibodies have worked successfully.

HER2 expression in osteosarcoma is typically low-level without the gene amplification and surface expression common in HER2+ breast cancer. This reduces physical accessibility for antibody-based drugs that rely on binding to the extracellular membrane-bound HER2. As an example, trastuzumab in combination with standard chemo failed to show a meaningful benefit in a phase 2 trial, consistent with the fact that trastuzumab does not strongly inhibit HER2+ osteosarcoma cell lines. In pOS, HER2 is simply not a strong driver or easily druggable surface target compared to other cancers. This is why a robust immunotherapy that initiates a full immune response against HER2, not just the initial targeting, is a much better approach.

OST-HER2 aims to stimulate a broad, durable immune response (stimulating a more diverse range of immune cells—T-cells, NK cells, dendritic cells etc.) against HER2-expressing cells rather than an antibody directly binding to oran antibody drug conjugate (ADC) delivering toxin to HER2. Higher T-cell/NK infiltration correlates with better outcomes in osteosarcoma. OST-HER2 may also therefore address micrometastases and prevent/delay recurrence better than direct HER2-binding drugs. OS Therapies’ biomarker data (e.g., seroconversion/immune response) correlated with clinical benefit, thereby supporting a plausible mechanism for the Accelerated Approval pathway. In short, past HER2 approaches and existing commercially available HER2 drugs probably can’t target direct surface HER2 in osteosarcoma well, since there just isn’t enough of it expressed. OST-HER2 drives fully activated immunogenicity against HER2, resulting in a more robust clinical response.

Increasing Value of Priority Review Vouchers (PRV)

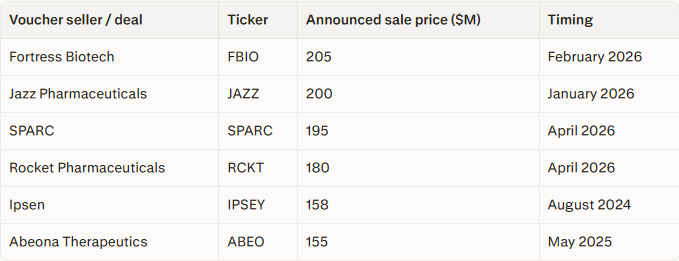

OSTX was awarded the Rare Pediatric Disease Designation (RPDD) for OST-HER2 for the treatment of fully resected, pulmonary metastatic osteosarcoma on November 3. 2021. With that designation came a Priority Review Voucher (PRV), but there was a “sunset” provision that required the designation by December 20, 2024, which they easily met, and an FDA approval by September 30,2026. On February 3, 2026 the Consolidated Appropriations Act, 2026 (CAA) extended the vouchers requirement of an FDA approval for another 3 years.

The expiration of the program has created a scarcity of vouchers and that’s a big factor given the high demand for these vouchers. The vouchers were put in place to allow big pharma to skip ahead in the approval process. Instead of waiting the standard 10 months for FDA review they could have an answer in 6 months. Getting the drug to market 4 months earlier could be worth hundreds of millions depending on the drug. This allows smaller companies like OSTX to sell the voucher to recoup their development costs.

Valuations have moved over the $200 million mark and that has created a potential windfall for OSTX. Sales started rising in late 2024, beginning at $158 million and rising to a peak of $205 million in February 2026. This backdrop is the setup for a large non-dilutive cash infusion upon approval of OST-HER2.

Favorable Regulatory Climate

Recent FDA reforms have been very favorable for both orphan drugs and pediatric oncology therapies, resulting in a record rate of approvals. FDA initiatives like the National Priority Voucher program have delivered oncology approvals in under 60 days for strategic priorities. Over the course of the past year, 67 new therapeutics were greenlit, many of which were for rare diseases via plausible mechanism pathways.

The FDA’s new "Plausible Mechanism" doctrine is the most significant tailwind for OSTX. The FDA’s recent willingness to approve orphan drugs based on strong biomarker data and Phase 2b survival signals (as seen with the 75% two-year overall survival in pediatric osteosarcoma) suggests that the May 2026 Pre-BLA meeting is a low-hurdle catalyst.

Regulatory momentum for OST-HER2’s therapy was bolstered by the FDA decision to grant a Type B meeting. It can be considered a signal of a high-priority review status.

Recent oncology approvals illustrate this new paradigm:

Bayer's (OTCMKTS: BAYRY) Sevabertinib (November 2025): Accelerated approval was granted for HER2-mutant NSCLC, based on strong efficacy and safety data in an orphan setting.

BMS’s (NYSE: BMY) Opdivo Quantig (November 2025): Subcutaneous formulation was approved, leveraging data extrapolation.

Merck’s (NYSE: MRK) Keytruda Qlex was approved (September 2025) for adjuvant melanoma and MSI-H solid tumors in pediatric patients (≥12 years), reflecting RACE Act-driven emphasis on molecular targets and expedited pediatric access.

These swift actions, along with new FDA review timelines from years to months, expand the number of rare disease incentives. This has created a potent tailwind for OST-HER2's orphan pediatric osteosarcoma BLA. While 2025-2026 saw 67 new therapeutics greenlit, many were for rare diseases via the plausible mechanism pathway.

Leadership Team Expansion

As OS Therapies submits early market access regulatory filings in several countries, Dr. Craig Eagle joined the leadership team as Chief Medical Advisor. He previously served as Chief Medical Officer at Guardant Health (Nasdaq: GH), a $12 billion precision oncology and liquid biopsy company. Before that, he served as VP of Medical Affairs Oncology at Genentech (OTCMKTS: RHHBY), where he oversaw oncology programs and drug trials. Previously, at Pfizer (NYSE: PFE), he worked in multiple senior oncology roles, including global medical leadership, U.S. oncology business oversight, and strategic alliances. Importantly, Dr. Eagle helped develop and commercialize multiple oncology drugs.

Therefore, he has extensive experience across clinical development and biomarkers, regulatory interactions, medical affairs, and commercialization. This oncology experience is exactly what a late-stage clinical company like OS Therapies needs when nearing a potential FDA approval. Dr. Eagle's appointment strengthens credibility and execution capability right as the company navigates these high-stakes regulatory steps, including commercialization/reimbursement planning and potential partnerships. Dr. Eagle’s quote in the company’s press release shows he's already deeply engaged with the data and platform:

"'Having become significantly more acquainted with the OST-HER2 asset in recent weeks, the potential pivotal nature of the clinical and biomarker data generated from the Phase 2b Metastatic Osteosarcoma Program that is now in the long-term follow-up phase, as well as OS Therapies' broader listeria monocytogenes cancer immunotherapy ("Listeria") platform, I have strong conviction that this technology has found its initial commercial niche from which it can expand into treating not only other settings in osteosarcoma, but many other metastatic and primary solid tumors," said Dr. Craig Eagle, Chief Medical Advisor at OS Therapies. "With Advanced Therapy Medicinal Products (ATMP) designation already granted in Europe and the U.K., I am working closely and rapidly with our regulatory team on U.K. and European commercialization and reimbursement preparations. We have upcoming meetings with FDA and MHRA to align upon the confirmatory Phase 3 protocol required to commence prior to the granting of early market access decisions in the U.S., U.K., and Europe. We have already aligned with EMA and ATGA on the key components of the confirmatory Phase 3 protocol design.'

Dr. Eagle continued, 'We are also preparing for the upcoming FDA Pre-BLA meeting to align on primary and surrogate clinical efficacy endpoints to provide the basis for a positive BLA decision under the Accelerated Approval program. This alignment will provide the basis to decide on our outstanding Regenerative Medicine Advanced Therapy (RMAT) designation request. It is encouraging that FDA has already aligned that OST-HER2 meets the biological definition of a gene-edited product that is required for RMAT.'"

Risks

The standard risk of a preclinical stage biotech is dilution. The company currently has an S-3 shelf offering of $100 million. Should they need to use this, it could lead to increased volatility in the price. The company also has several planned clinical trials ongoing or planned, and while positive outcomes could derisk the stock, failures in the design, execution, or drug performance could reflect negatively on the company.

Overall, the risk of dilution to OSTX shares is high as the company has an anticipated cash runway into 2027, and will almost undoubtedly need to raise more cash around the turn of the year, unless they are able to garner and sell a PRV within that time. Because of this, regulatory delays and potential BLA rejection of phase 3 prerequisites also pose an implied dilution threat in addition to potentially delayed commercialization.

Financial Analysis

For OS Therapies, 2025 was a transition year. They spent $8 million to acquire the rights to the Listeria monocytogenes immunotherapy platform tech from Ayala Pharmaceuticals. This investment gave them full control to develop the pipeline beyond Osteosarcoma into over 30 cancer types including large ones like Non-Small Cell Lung Cancer (NSCLC) and Prostate Cancer. This left the company with cash of $270k and $9.9m in accounts payable as of their 2025 10-K filing. In 2026 they completed a direct offering of $5.25m in April. They are also expecting a total of $4.0 million in non-dilutive financing split between VAT refunds from their UK subsidiary along with R&D tax credits.

In the first half of 2025 their burn rate was running at approximately $1.0 million per month and then increased to $1.5 million per month in the final half as they were prepping their phase 3 sites in Australia and the U.K. (expected to commence in Q3 2026), manufacturing scale-up, and initiation of their EMA rolling review. This year they lowered their burn to about $400K per month which covers the phase 2b data monitoring. Based on the cash on hand along with the funds from their UK subsidiary they are expected to extend their financial runway into 2027.

Their burn rate will start to scale higher in Q3 2026 as they move forward with their confirmatory Phase 3 in Osteosarcoma which will initially start in Australia. There are indications of a Conditional Marketing Authorization (CMA) in the EMA, U.K., USA, and Australia which would translate into $50 million in European sales in 2027 and be able to finance their other initiatives without further dilution. A USA approval would likely translate into a PRV currently selling for around $200 million. While the company is not extremely well-capitalized, it has enough cash runway to reach a number of milestones each of which would be transformative from a financial and stock perspective.

Catalysts

OS Therapies has a busy catalyst calendar for the rest of 2026:

Q2 2026 - Type B Pre-BLA meeting results: The Type D meeting was elevated to a Type B in March, and all available data was submitted at the end of Q1. Meeting/results are still pending, with Q2 meeting planned to align with EMA and Australia TGA on 3-year overall survival as the prospective clinical endpoint with biomarker seroconversion data as the key surrogate efficacy endpoint.

Q2 2026 - Potential alignment of regulatory agencies regarding a confirmatory phase 3 trial design: phase 3 protocol meetings with FDA, MHRA, EMA, and Australia TGA are intended to support a 3-year overall survival primary endpoint.

Q2 2026 - FDA Rolling Review was granted and initiated, with non-clinical and CMC FDA BLA modules submitted in January 2026, and with the most up-to-date clinical module submitted at the end of March 2026. The rolling review does not appear to be officially complete yet, and an announcement confirming full BLA submission could serve as a catalyst.

Q2 2026 - OS Animal Health spinoff: The OSAH subsidiary was formed in 2025, with an S-1 filed in January 2026, for an IPO/listing on the NYSE American/Nasdaq, intended for H1 2026.

Q3 2026 - MHRA and Australia TGA Rolling review decision.

Q4 2026 - US, UK, Europe and Australia Accelerated/Conditional Approvals.

Q4 2026 - US Priority Review Voucher sale: OST-HER2 has had Orphan and Fast Track Designation granted by the FDA and EMA, and OST-HER2 has also received Rare Pediatric Disease Designation (RPDD) from the FDA. Accelerated Approval appears likely and would result in being granted a PRV.

OS Therapies has a lot of potential catalysts in the near term (the rest of 2026). The company has FDA Pre-BLA meetings anticipated in May 2026 with additional Q2 regulatory discussions regarding their clinical data and biomarkers with MHRA, EMA, and TGA in Q2. The company intends to initiate a Phase 3 in Australia in Q3, and there are three potential 2026 approvals in the USA (Accelerated Approval) and Europe/UK (Conditional Marketing Authorizations). Accelerated Approval is an achievable goal with Orphan, Fast Track, and Rare Pediatric Disease Designations. The company also stated that they had “confirmed immune biomarkers' suitability to establish surrogate clinical efficacy that could support BLA under Accelerated Approval Pathway” with the FDA in a December 2025 Type C meeting.

Investment Summary

OS Therapies is undervalued on multiple counts. The current market cap is $75 million. The company is clinically derisked as it is eyeing multiple regulatory approvals across Europe and the United States and has several special designations for OST-HER2. Peak sales across EU and US could reach $700 million, including $50 million in 2027, so the company’s requirement for developmental cash may be coming to an end soon. With approved drugs typically worth a low multiple of peak sales estimates, the company could command a billion dollar valuation. Nonetheless, with a PRV in its sights, OSTX may soon have its hands on an asset worth ~3x its current market capitalization, giving it a conservative price target upon approval of roughly $4-5, versus ~$1.70 that it is currently trading at. If OSTX has a successful approval and rapid drug launch, the stock could re-rate towards ~$10. On the other hand, regulatory delays or poor feedback would require use of the company’s shelf offering or another financial mechanism while putting the company’s commercial future in doubt, and shares could quickly lose support. Overall, the risk-reward on OSTX looks positive with robust regulatory support, strong clinical data, and a pending approval with a $200 million gift attached.

Comments

Log in or sign up to join the conversation.