Image Source: Unsplash

Market Brief – Rally Begins As Dip Buyers Emerge

Markets surged into the Thanksgiving holiday, ending the week with substantial gains across all major U.S. indexes. The S&P 500 rose by approximately 3.7%, marking one of its strongest weeks in the past six months. The catalyst was a combination of falling bond yields and increasing confidence that the Federal Reserve has completed its rate hikes. Currently, Kalshi (prediction market) is projecting an 80% chance of a rate cut in December.

(Click on image to enlarge)

With inflation data continuing to trend lower and growth indicators remaining stable, the markets are starting to price in stronger earnings and economic growth in 2026, particularly as lower Treasury yields boosted duration-sensitive sectors and encouraged risk-on behavior.

Unsurprisingly, despite all of the recent talk of the “Death of the AI Trade,” Technology stocks once again led the charge. The AI narrative regained momentum, pulling mega-cap names higher and lifting the broader Nasdaq. Nvidia’s earnings beat helped reinforce the bull case around AI infrastructure and cloud demand. The “Magnificent Seven” tech leaders contributed outsized returns to index performance, though broader participation remained limited.

Volatility declined as technical indicators turned more supportive after the last few weeks of choppy action, which was also unsurprising. Despite the gains, many risks remain, including concentration in the market-cap-weighted index, valuations, and market breadth. However, those concerns may take a backseat temporarily following the recent correction and reversal in bullish sentiment.

Heading into December, all eyes will turn to the upcoming PCE inflation report, jobs data, and the final round of Fed comments before the blackout period. Until then, momentum favors the bulls, but the foundation remains fragile.

Let’s review the technical backdrop.

Technical Backdrop – Market Rallies As Expected

Over the last few weeks, we discussed the risk of downside pressure in the market and that the correction set up potential for a rally during the holiday-shortened trading week. That occurred with the S&P 500 rising roughly 3.7% from last Friday’s close near 6,849. That rebound recaptured the losses from the prior AI- and rate-cut-wobble selloff and pushed the index back toward its late-October highs. On a bigger picture basis, the index remains up around 16% year-to-date and is now roughly flat for November, reflecting a strong tape that has simply been digesting earlier gains. The rally also triggered a fresh momentum “buy signal” which will be supportive of further gains into next week.

(Click on image to enlarge)

From a trend standpoint, the price remains aligned with the bulls. The S&P is trading above its rising 50- and 100-day moving averages, which sit roughly in the 6,700–6,575 zone, and well north of the 200-day moving average near 6,175. Earlier in November, the index finally broke its streak above the 50-day moving average (DMA) and corrected back to the 100-DMA, working off some of the speculative excess in AI and high-beta names. This week’s bounce off that support pulled the price back into the upper half of its recent trading range, keeping the primary uptrend intact.

Volatility has cooled but not disappeared. After spiking into the upper 20s during the recent tech/AI downdraft, the VIX slid back into the high teens, around 16, by Friday’s close, signaling that the panic bid for protection is fading but that investors are not yet entirely complacent. That’s consistent with a market transitioning from a “shot across the bow” correction to a more typical year-end positioning grind.

(Click on image to enlarge)

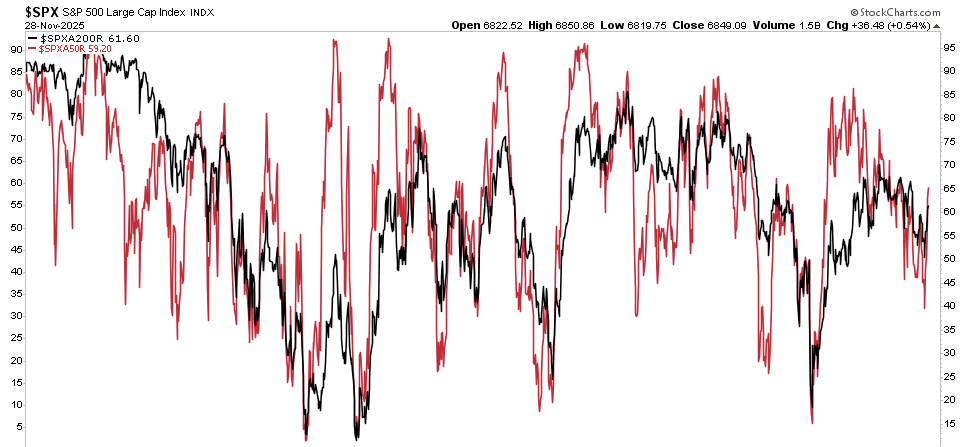

Breadth is improving, but it isn’t a blow-out green light. Roughly 59% of S&P 500 stocks are back above their 50-day moving averages, and just over 61% trade above their 200-day, a solid improvement from the trough earlier in the month but still shy of the 70%+ readings you’d expect in a truly broad-based rally. Participation has also expanded beyond mega-cap tech, with more cyclical and value names stabilizing; however, leadership remains heavily tilted toward large-cap growth and AI-adjacent beneficiaries.

(Click on image to enlarge)

Bullish case heading into December: Seasonality, positioning, and trend still lean in favor of the bulls. December is historically one of the stronger months for equities, particularly when the market is already up by double digits year-to-date. Expectations for a December Fed rate cut, and a gradual cooling of inflation, support the “soft-landing” narrative, while corporate buybacks and under-invested managers create fuel for a “chase into year-end” if resistance gives way. With volatility easing and breadth improving, the path of least resistance near term remains higher if key support zones are maintained.

Bearish case heading into December: The bears will point out that valuations in AI and growth remain stretched, that volatility is still elevated compared to the summer lows, and that breadth, while improved, is not confirming a runaway advance. The recent episode, where AI leaders and other risk assets (including Bitcoin) sold off together, is a reminder that risk appetites can shift quickly when the crowd questions the durability of earnings or the timing of Fed cuts. Delayed economic releases from the earlier government shutdown create an additional wildcard: a batch of weaker-than-expected data hitting all at once could challenge the soft-landing narrative just as liquidity gets thinner into year-end.

Support and Resistance Levels

- Near-term support:

- ~6,725–6,750: cluster of short-term support at the 20 and 50-DMA

- ~6,569: last week’s support at the 100-DMA.

- Deeper support: ~6,175 (200-DMA) on any more serious risk-off move,

- Resistance:

- 6,867–6,909: Previous market tops in mid-October and early November.

- 7,000: psychological round-number magnet if momentum accelerates

- Volatility “line in the sand”:

- VIX back above ~22–23 would signal a renewed risk-off phase; sustained readings in the mid-teens would confirm a constructive backdrop for a “Santa Rally” push.

Bottom line: the primary trend remains bullish, but the margin for error is narrowing. As we enter the final month of the year, the bulls remain in control as long as the index holds above the 50-day moving average and breadth continues to improve. A failure back below the 6,600 area, especially if accompanied by a renewed spike in volatility and renewed AI/credit jitters, would shift the balance of risk toward a deeper consolidation rather than a clean “Santa rally” into year-end.

Key Catalysts Next Week

Next week marks a pivotal moment for investors. The bulk of U.S. economic data is expected to resume after recent delays. Liquidity remains seasonally light. That raises the stakes. A few data points and events could drive outsized volatility. They also carry the potential to reinforce or derail the market’s year‑end setup. Below is a table of the most important market and economic events to watch.

(Click on image to enlarge)

The first week of December reconnects markets with key economic data that had been delayed during the recent government shutdown. The arrival of those data releases reactivates the fundamental underpinnings of market direction. A few strong prints — on inflation, employment, manufacturing, or services — could validate a bullish year-end narrative. Conversely, any surprise weakness could derail current optimism. Inflation data is especially sensitive, and the upcoming PCE release is expected to shape market expectations ahead of the next Fed meeting on December 9–10.

Liquidity remains thin with many traders still on holiday or in partial holiday mode. In such an environment, headline‑driven moves can be magnified. That means surprises, either good or bad, have the potential to move markets significantly more than usual. Lastly, with this being the last week before the Fed’s policy blackout period, any public statements from officials carry extra weight. Market participants will scrutinize every word looking for any tone or messaging that will influence yield expectations, risk sentiment, and positioning as we head into the final stretch of the year.

More By This Author:

The K Shaped Economy In One Graph

Ray Dalio Says Sell: But Not Yet

Permanent Job Losers: A Worrying Facet Of Today’s Economy

Comments

Log in or sign up to join the conversation.