“Wipe Out” is an appropriate description of what is happening beneath the calm surface of the bull market. As we head into the end of the year, many are hoping for “Santa to visit Broad and Wall”. However, those hopes are not just about adding to this year’s already excessive annual gains. Instead, for many, it’s the hope to recover some brutal losses.

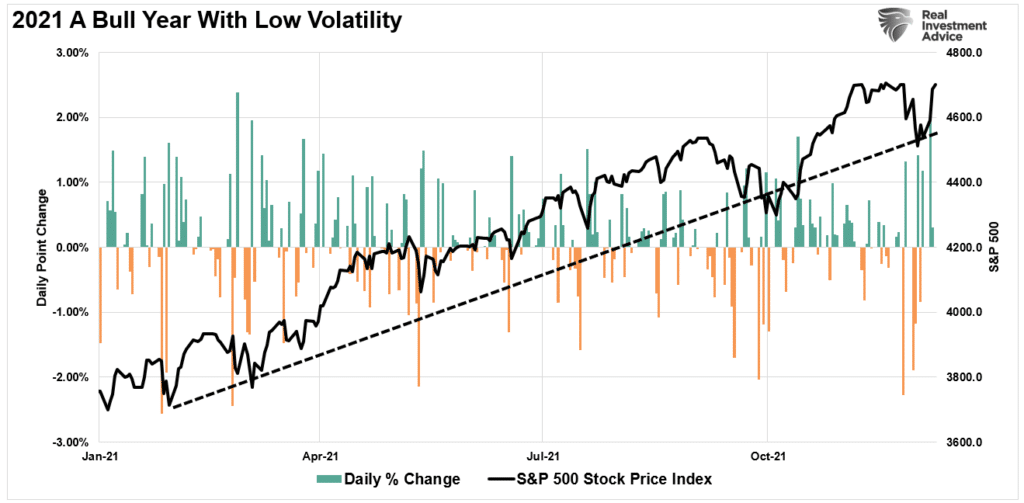

If you haven’t been paying much attention, the market is currently sitting near all-time highs. While it has risen nearly 26% this year, there were a couple of very normal 5% corrections along the way.

By looking at the chart, you would assume that performance across the index was pretty equal. However, that would be an erroneous assumption.

As the old saying goes:

“You can’t judge a book by its cover.”

Market Cap Weighted Illusion

One of the problems with the financial markets currently is the illusion of performance. That illusion gets created by the largest market capitalization-weighted stocks. (Market capitalization is calculated by taking the price of a company multiplied by its number of shares outstanding.)

Notably, except for the Dow Jones Industrial Average (DIA), the major market indexes are weighted by market capitalization. Therefore, as a company’s stock price appreciates, it becomes a more significant index constituent. Such means that prices changes in the largest stocks have an outsized influence on the index.

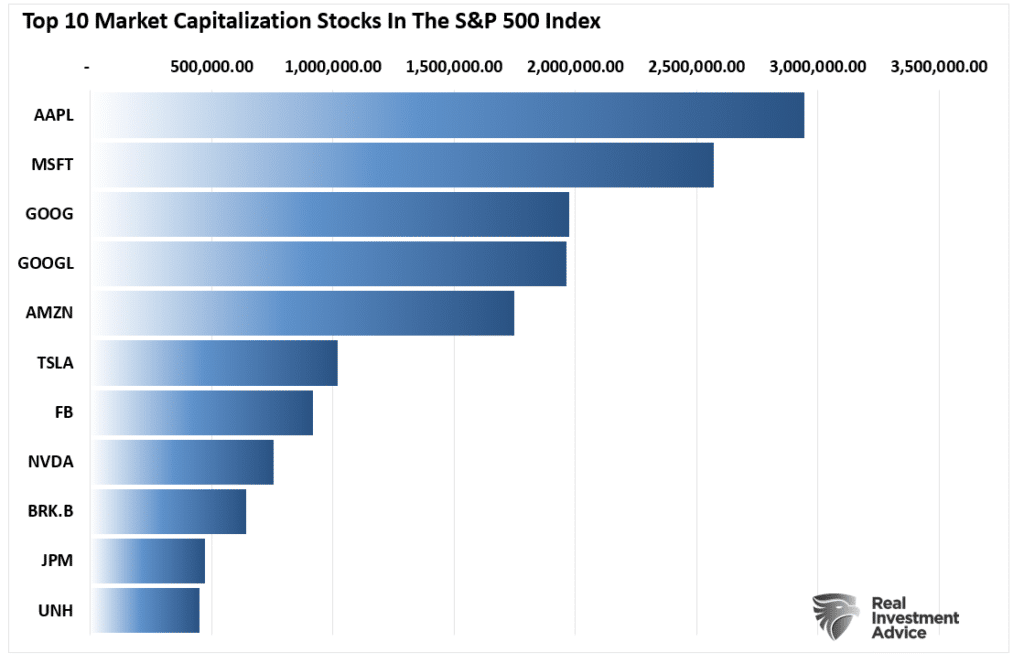

You will recognize the names of the top-10 stocks in the index.

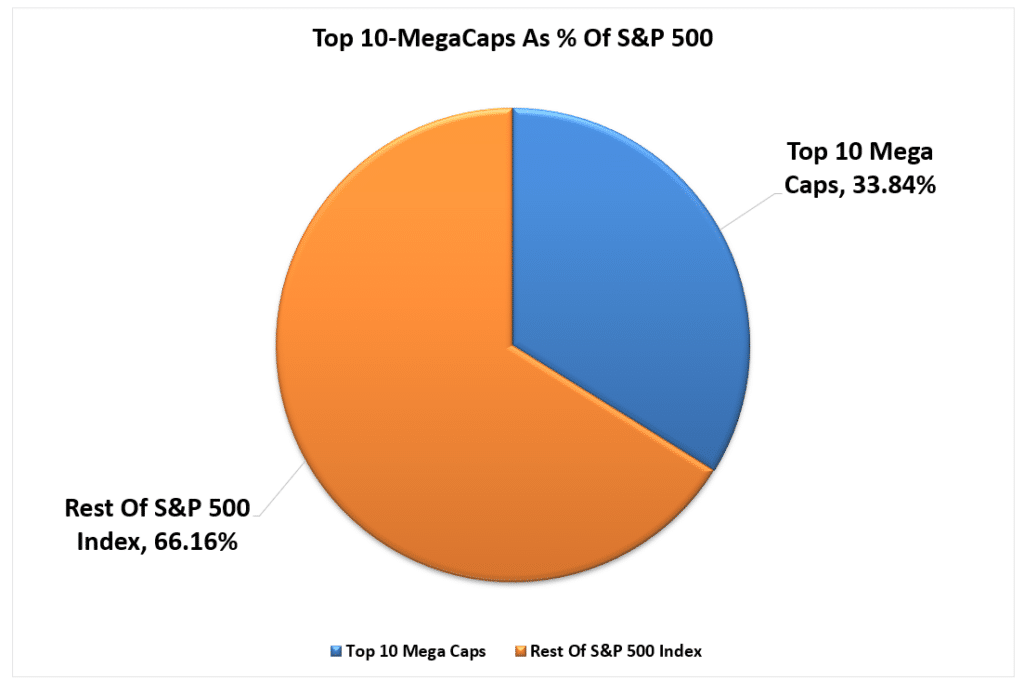

Currently, the top-10 stocks in the S&P 500 index comprise more than 1/3rd of the entire index. In other words, a 1% gain in the top-10 stocks is the same as a 1% gain in the bottom 90%.

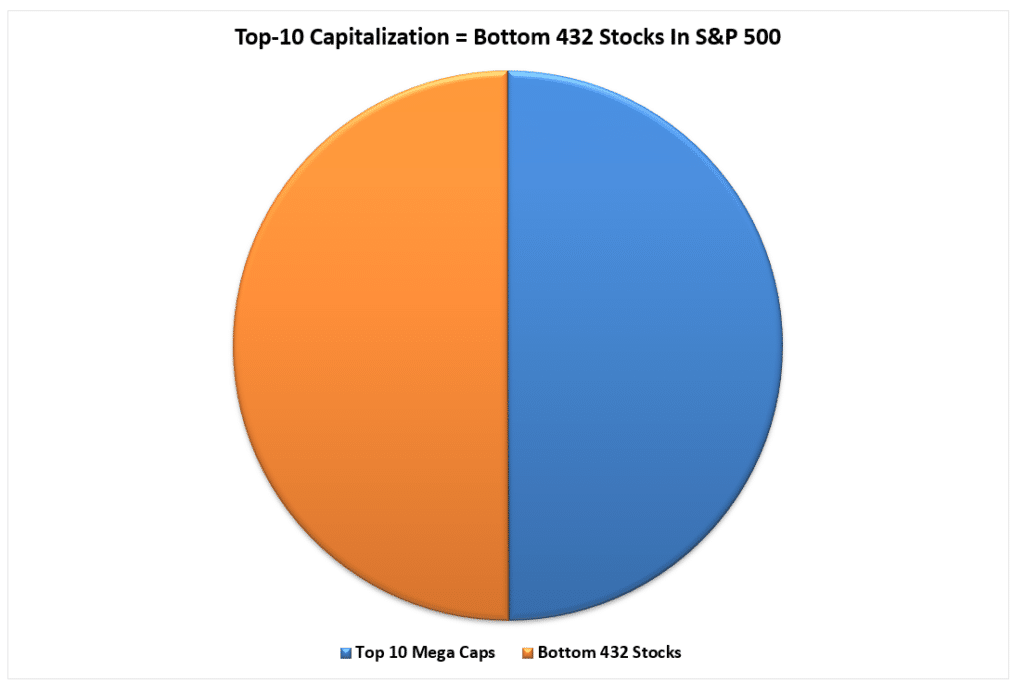

Another look at the contribution skew is to compare how many companies it would take to comprise the same weighting. Currently, out of 500 stocks, the bottom 432 stocks comprise the same market capitalization as the top-10.

Such is the story of 2021. Had it not been for the enormous returns in companies like Apple (AAPL), Google (GOOG), Microsoft (MSFT), Tesla (TSLA), and Nvidia (NVDA), the years return would be much different.

Below The Surface The Damage Is Evident

As noted, without the support of the top-10 holdings, the year-to-date returns and overall volatility would be pretty different.

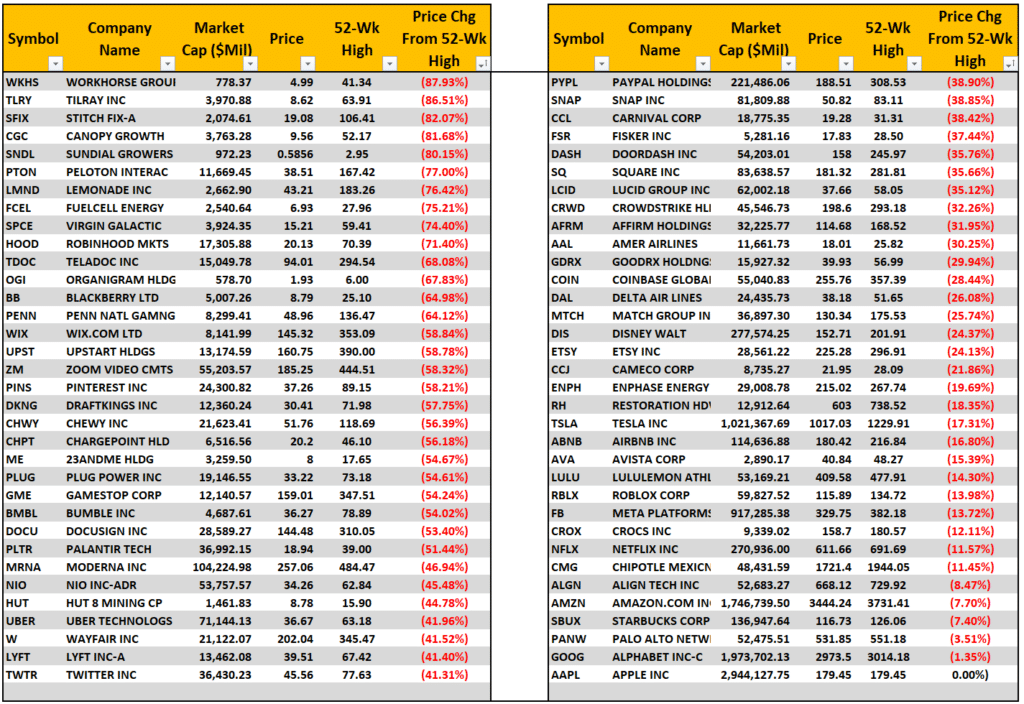

However, looking at a sampling of the more “popular” trading stocks, you can understand current retail traders’ frustration. A vast majority of 2020 and early 2021’s high-flying stocks are down significantly from their respective 52-week highs.

(Click on image to enlarge)

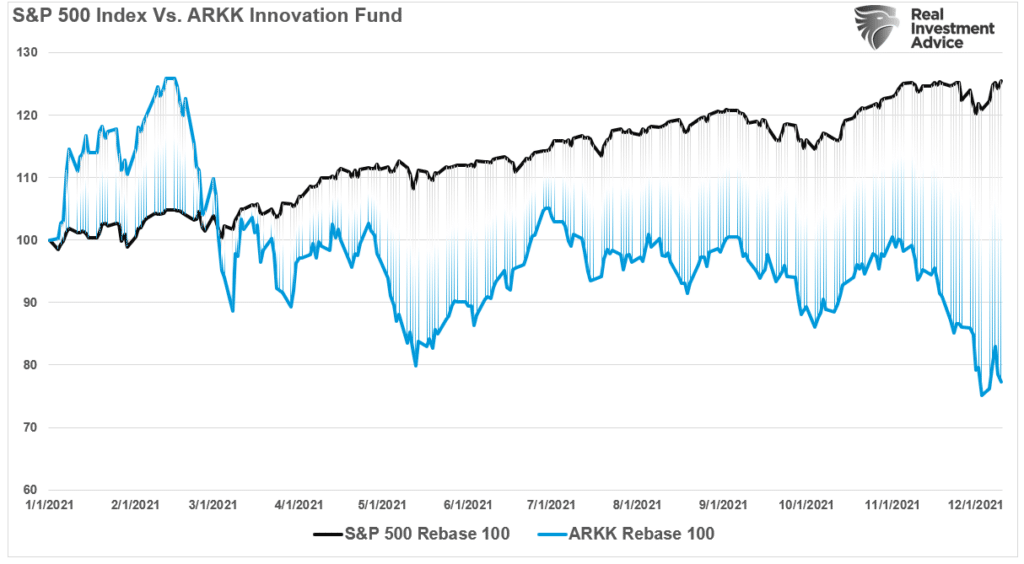

Of course, probably one of the best representations of the disparity between the index and the “wipe–out” below the surface is the ARKK Innovation Fund (ARKK). In 2020, the media proclaimed Cathie Wood the top investor of the year. Millennials and Gen Z investors poured money into her fund to chase the upcoming technology stocks of the next generation.

Unfortunately, that turned out to be a bad bet.

While the S&P 500 index is up roughly 25% in 2021, ARKK is down more than 20%. That is quite a performance differential but shows the disparity between the mega-cap companies and everyone else.

However, it is NOT just the “meme” stocks that significantly underperformed the index. If you owned a diversified portfolio of small, mid, emerging, and international stocks, performance significantly lagged the S&P 500 index.

On a global basis, as noted by Sentiment Trader, just about everything is underperforming the S&P 500.

“The percentage of country ETFs outperforming the S&P 500 on a rolling 1-year basis has fallen to the lowest level since May 2020.”

As they conclude”

Strength is primarily evident in the U.S., with overseas indexes showing an alarming level of relative underperformance. When trends were lagging like this in the past, annualized returns in the MSCI indexes have been poor.

A Significant Risk

The point you should take away from this analysis is the significant risk posed to investors with capital hiding in a handful of stocks. Over the last several weeks, we noted the “lack of liquidity” in the markets, along with weak breadth. To wit:

The stock market is a function of buyers and sellers agreeing to a transaction at a specific price. Or rather, “for every seller, there must be a buyer.”

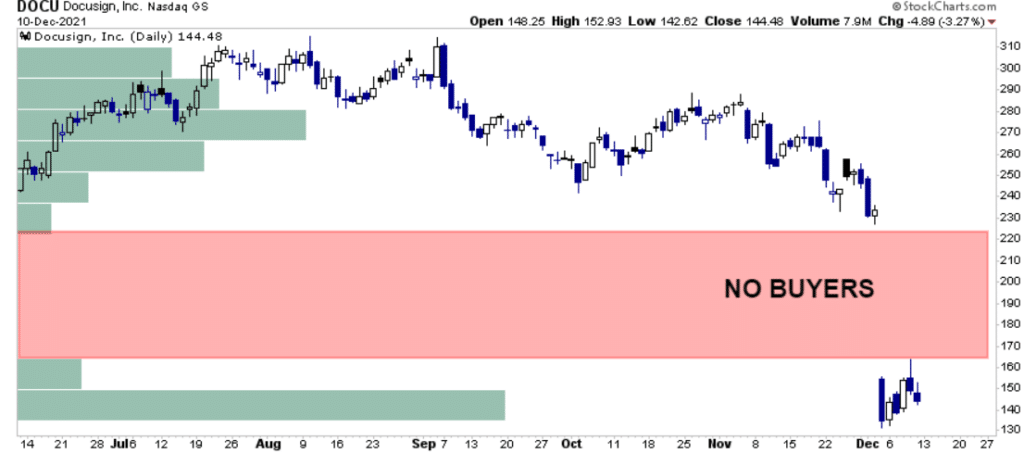

Such is why downturns in the market tend to be a “wipe-out” rather than a “pullback.” A good example recently was Docusign (DOCU).

When there are not enough buyers at current prices to absorb an increase in selling pressure, prices gap down. While there are indeed buyers for every seller, they are at significantly lower prices.

However, during these “wipe-outs,” capital continues to flow into the index’s top holdings. Such is because these stocks are highly liquid. For traders, they provide a “safe haven” to move large amounts of capital without creating a gap between buyers and sellers.

However, if capital flows reverse from these top-10 holdings for some reason, the illusion of a strong market will fade quickly. Most likely those flows will be into bonds for safety as something has likely changed the bullish psychology of the market.

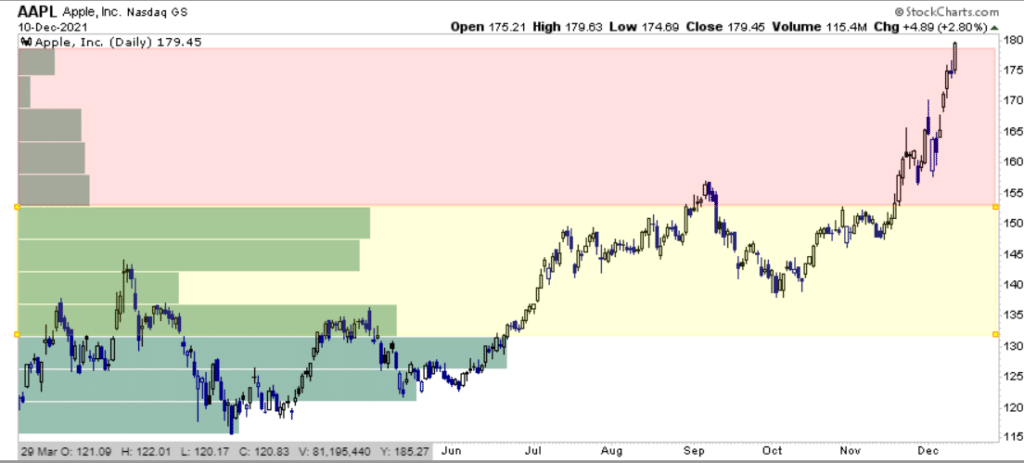

Just in case you are wondering, buyers are significantly lower in Apple currently.

While the top-10 holdings of the major indexes continue to be a “safe haven” for traders currently, heading into 2022, I would keep a close watch on them. They are likely going to be the best indication for when the flight to safety has started.

Of course, if you have been holding “meme” stocks this year, the “wipe-out” should already have you thinking about changing your investment strategy.

Comments

Log in or sign up to join the conversation.