Image Source: Pixabay

Market Analysis

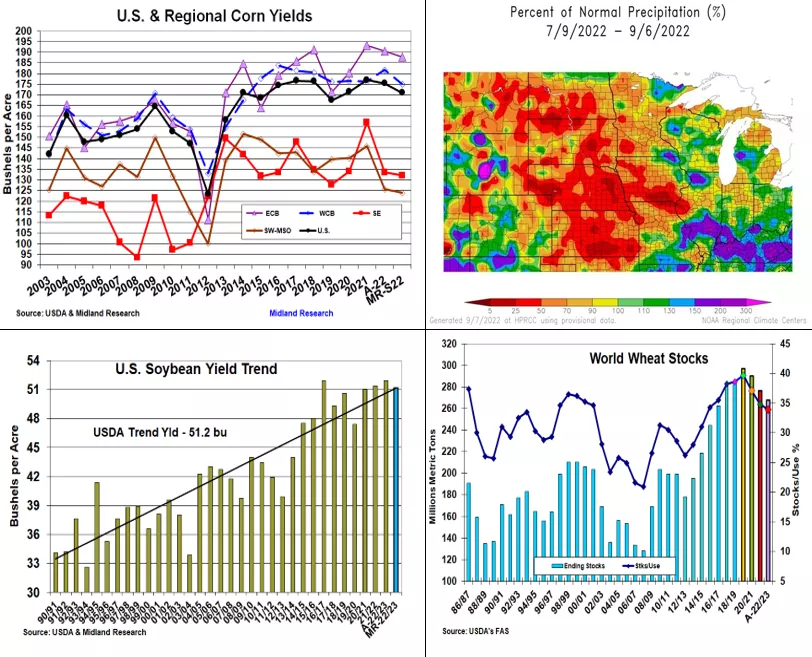

The upcoming September 12 US Crop & Supply/Demand updates have the trade’s attention. This summer’s heat and dryness in the WCB vs the above-normal rainfall in the southern half of the ECB and the Mid-South has diverse expectations surfacing across the Central US. A late USDA announcement they would utilize 2022’s delayed FSA sign- up & prevent plant data from August in their crop area levels has added last-minute uncertainty about 2022’s US-harvested corn & bean acres. Last month’s Midwest Crop Tour revealed some significant yield impacts to the crops west of the Missouri River while the eastern Midwest’s late plant- ings curtailed their field yield results vs 2021. The USDA’s initial 10-state field data will primarily be population counts.

Given the weather and the tour field data, NE, SD, KS, and W & S IA corn yields could reduce the WCB yields by 6.6 bu. Tour results from the ECB suggest a 2.7 bu lower average yield vs August while the SW and SE dip slightly.

Overall, a 171 bu US average yield is expected while the trade’s wire service average is 172.5 bu, down 2.9 bu from last month’s USDA estimate. The trade is expecting a modest 152,000 smaller harvested acres and a 14.09 billion bu crop vs our crop size of 13.995 billion this month. These smaller supplies tighten the US 2023 ending stocks to 1.175 billion bu. with a modest decline in exports. Last month’s FSA acreage data suggests a possible 300,000 larger harvested area to us while the trade’s average estimate is for just a 77,000 increase. However, 2022’s below-normal rainfall west of the Mississippi River has us projecting just a 51.2 bu US trendline yield even with average pod numbers. This could produce a 50 million smaller crop at 4.48 billion bu. Slow exports this summer and larger S Am crops could reduce this US demand and keep new crop US stocks at 240 million, down 5 million bu.

With no US wheat crop updates, the Black Sea conflict, the US winter wheat seedings & the world’s wheat crops will be watched closely after dryness has curtailed Europe, the US winter wheat, and Argentina’s crops so far in 2022.

What’s Ahead:

The impact of the drought on the western Midwest’s crops on 2022’s overall US corn and soybean outputs and stocks has the trade’s attention. This report along with S America’s seeding progress and the Black Sea’s export output will be market factors as the US fall harvest begins to pick up speed. Hold new-crop soybean sales at 45%, corn at 33% & wheat at 25%.

More By This Author:

US ECB Corn & Bean Counts Couldn’t Cover WCB Heat/Dryness

Weather Remains A Big US Corn And Soybean Yield Factor

Weather May Nip Corn & Soy Yields, But Will Resurvey Show More Beans?

Comments

Log in or sign up to join the conversation.