Market Analysis

The USDA’s July US supply/demand revisions for wheat & soybeans generally followed the trade’s expectations after June’s USDA acreage & stocks reports. Higher old and new-crop stocks levels than trade’s averages were a bit negative for corn’s value. Without any prominent bullish US or World grain fundamental from the USDA reports, the investor community resumed its selling at the CBOT. An announced Wednesday meeting in Turkey between Russia, Ukraine and a UN mediator also left many traders on the sidelines waiting to see if a Black Sea export corridor from Odessa might occur after numerous tries.

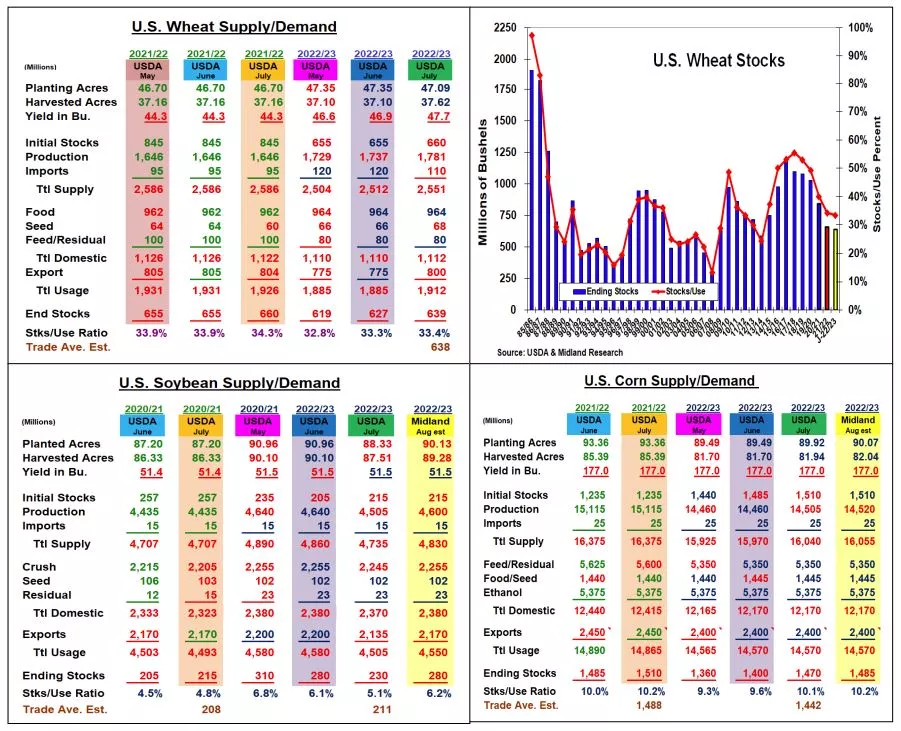

June’s higher US winter wheat harvested area helped boost this variety’s output by 19 million bu to 1.2 billion. A 24 million rise in this month’s US spring wheat & durum crop survey vs the USDA’s previous estimates increased July’s overall crop to 1.781 billion. Smaller French, Ukrainian & Argentine crops were behind the USDA’s unexpected increase in US exports by 25 million to 800 million. This kept July’s US 2022/23 stocks at 639 million, up only 12 million bu from last month & down 21 million from 2021.

The USDA sliced 10 million from old-crop US soybean demand, but it came in the crush, not exports. However, the World Board did decrease their new-crop demand levels after last month’s lower plantings reduced 2022’s US crop outlook by 135 million bu. Dropping crush by 10 million and exports by 65 million left their 2022/23 stock at 230 million. This was down 50 million bu from last month, but above the 210 million level that the trade was expecting. No S Am crop changes were made this month and the USDA sliced 900,000 tons from its world ending stocks.

Despite last month’s neutral June 1 stocks, the USDA sliced 25 million from corn’s old-crop feed demand on lower livestock numbers it seems. June’s higher harvested acres boosted this month’s US output by 45 million to 14.505 billion. With no changes in their corn demand forecasts this month, these 70 million larger beginning supplies increased corn’s 2022/23 stocks to 1,47 billion bu.

What’s Ahead:

Without any bullish surprises in this month’s USDA reports, the CBOT prices remained on the defensive after the update. However, 60-70% of the US corn crop will be going thru pollination in the next 3-4 weeks. Given the expanding dry soils in the Midwest, US weather will be highly influential to prices.

After recent sales, hold your 2022 corn and soybean sales at 33% and your wheat sales at 25%.

More By This Author:

Pre-July U.S. S&D/Wheat Updates - Despite A Lower U.S. Soybean Acreage, The Market Focus Is On Weather

Wet Spring Cuts Soybean Plantings, While Stocks Near Estimates

More Corn, Less Soy - Wet Spring Slowed US Plantings

Comments

Log in or sign up to join the conversation.