Tuesday Talk: Powell, Power And Politics

President Biden nominated Jerome Powell for a second term as Chair of the Federal Reserve Bank, yesterday. While most of the bets were on Powell, some were surprised and the Nasdaq sold-off on the announcement, turning sharply lower at the end of the trading day largely due to profit-taking.

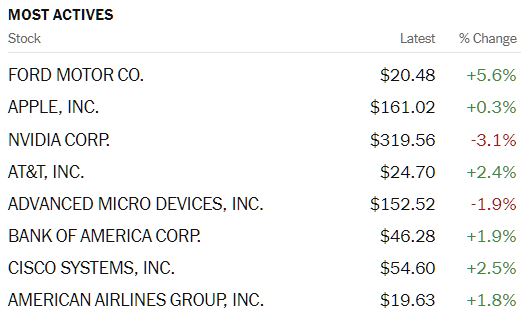

The S&P 500 closed at 4,682, down 15 points, the Dow closed at 35,619, up 17 points and the Nasdaq Composite closed at 15,885, down 203 points. Most actives were all among the blue chips.

Chart: The New York Times

Currently market futures are mixed: S&P futures are trading down less than a point, Dow futures are trading up 14 points, and Nasdaq 100 futures are trading down 57 points. This morning traders and investors are awaiting the release of November preliminary Manufacturing and Services PMI data.

In headline video news the Staff at LMAX Group see the Market Shaken Up On Powell Reappointment. "The reappointment of Fed Chair Powell is the big story into Tuesday. The market has since reacted accordingly, pricing in a more hawkish leaning Fed. This has resulted in more US Dollar upside and reversal in US equities."

TalkMarkets contributor Saqib Iqbal writes the Gold Price Seems Vulnerable Near $1,800, Awaits PCE Inflation Data .

"The gold price plummeted overnight after US President Joe Biden reappointed Jerome Powell as chairman of the Federal Reserve...After the news broke overnight, those rates were dropped, and Fed Funds futures prices became more aggressive. Assisted by a revaluation of the US Treasury bond market, bars (GLD) fell sharply against the US dollar. For the first time since February 2020, the yield on the 5-year rate-sensitive bond exceeded 1.3%."

"As the markets digest Biden’s decision while overriding (Fed Chair candidate and now Vice Chair nominee) Lael Brainard’s forward-looking price forecasts, yellow metal prices could experience increased volatility...As long as the chairmanship has no political implications, the Fed can focus more aggressively on inflation given current levels...The Fed should gain political weight from the executive branch as a result of this. The Personal Consumption Expenditure Price Index will break the boundaries on Wednesday, updating market price information. In October, analysts expect the PCE, which excludes volatile food and energy prices, to rise 4.1%. The PCE increased by 3.6% in September...Gold could fall more than expected, as the (inflation) rate hikes are likely to push (interest) rates higher...After Biden’s announcement, Fed futures moved from a 17.9% probability on November 19 to a 26.5% probability on November 22 due to the expectation of a 50 basis point rate hike at the June 2022 FOMC meeting."

Marc Chandler who covers the forex beat had the following comments about the Powell reappointment in his article, Tech Sell-Off Continues:

"We suspect many pundits exaggerated the link between the re-nomination of Powell for a second term and the sell-off in US debt and technology shares. First, it was not a surprise. Second, it assumes a substantive difference in the conduct of monetary policy between Powell and Brainard. There isn't. The difference was on regulatory issues and on the role of climate change. Third, the idea that the Fed may accelerate its bond purchases next month was sparked by the high CPI reading on November 10. Yesterday, Bostic joined fellow Fed President Bullard. Two governors (Clarida and Waller) also seem to be moving in that direction (Waller may be faster than Clarida). The fact of the matter (is that), nearly all of the high-frequency data for October, including employment, auto sales, retail sales, industrial production, and inflation, came in higher than expected."

Still, Chandlers says, "The markets are unsettled. Bond yields have jumped, tech stocks are leading an equity slump, and yesterday's crude oil bounce reversed (BNO). Gold, which peaked last week near $1877, has been dumped to around $1793. The tech sell-off in the US carried into the Asia Pacific session, and Hong Kong led most markets lower."

With inflation also gathering momentum in Europe and elsewhere, contributor William L. Anderson wants to remind us that, No, Inflation Is Not Good For You. He has harsh words for those who think otherwise.

"President Joe Biden is touting an endorsement of his “Build Back Better” initiatives by a number of Nobel economics winners who have claimed the proposed programs included in the legislation would reduce inflation...There is an important point to be made here: all of these “experts” are willing to say they believe inflation is a problem for most people and the disagreement isn’t so much about the real and potential harm inflation brings, but rather the duration of the current spikes. However, there also exists among radical progressives a belief that inflation actually is a good thing because, in their minds, it transfers wealth from the rich to the poor."

In addition to taking more than one economist and political scientist to task Anderson makes the following salient points:

"...the incessant money pumping from the Federal Reserve System coupled with its suppression of interest rates has benefitted the wealthiest Americans at the expense of everyone else. Take billionaires like Jeff Bezos and Bill Gates, for example. The vast amount of the official wealth owned by these men is in Amazon and Microsoft stock, respectively, and we have seen a large increase in stock prices due to Fed policies...Middle-class people, on the other hand, historically have increased their wealth through saving...Fed policies have severely limited these options, driving investments into equities, and many middle-class people who are not sophisticated investors find it difficult to navigate the wild swings in stock prices that have come with inflation-driven asset bubbles."

I'm not entirely convinced of that. Internet based trading as well as online investor education has made middle-class investors more savvy than in the past and according to the website Fair Observer "account for almost as much volume on the US stock market as mutual and hedge funds combined". I would however, agree that meager returns in safe-haven assets like CDs and municipal bonds are impetus for Jane and Joe investors to increase their exposure to riskier assets like stocks.

Whether one shares Anderson's convictions about current Fed policy being bad for the economy (he is far from the only one) he is most likely point on when he writes, "Whatever temporary gains many workers are experiencing with higher wages, the euphoria is not likely to last long."

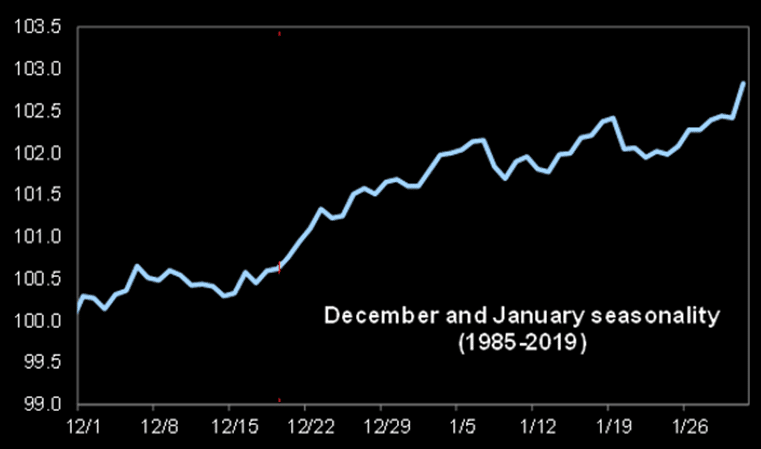

TM contributor Lance Roberts notes a Santa Claus Rally Is Coming, But Will Markets Correct First? To be sure, of that he is unsure. Roberts is largely bullish, but in a detailed article, laden with historical references, he also notes what could go wrong. Here is some of what he has to say:

"At the moment, investors are “making their list, and checking it twice.” Sure, prices remain near all-time highs, but the Fed is remaining accommodative (at least for now.) Earnings remain very “nice,” and the market largely views “pandemic” related risks largely priced in. Yes, inflation is “naughty,” but the market seems convinced it will be transient...Hopes are high that profit margins will continue to be strong, and eventually, earnings will catch up to valuations."

"There are more than just a few caveats to this analysis, both bullish and bearish.

- From the bullish perspective, sentiment remains optimistic, momentum is strong, and speculation is rampant. Such can certainly keep stocks elevated in the near term.

- From a bearish view, valuations, inflation, and the Fed remain challenges. However, while these broader factors tend to play out over longer periods, they provide the “fuel” for an exogenous catalyst. Such could be a spike in interest rates, a more hawkish Fed, or an expected battle over the “debt ceiling.”"

"The good news is that if “Santa does visit Broad and Wall,” the January effect has a greater degree of potential success. Of course, there is no guarantee of that either, but historical odds are strong that momentum will carry through."

"However, beyond that in 2022, I don’t have a clue. Currently, Wall Street analysts are optimistic with Goldman Sachs (GS) predicting the S&P to hit 5100 next year. Anything is possible, but when looking at the market on a longer-term basis, with earnings and economic growth likely peaking, I am a bit more sanguine on outcomes."

Michael Kramer has a column title fit for closing out today's round-up. In his article, Stock Market: Will The Last One Out Please Remember To Turn Off The Lights?, Kramer notes that things like Fed tapers, higher interest rates, higher commodity prices, high company valuations and a strengthening dollar might not be the best thing for the stock market.

"(Monday) Stocks started the day higher, but it didn’t end well. The market initially jumped on the news that Jay Powell would get a second term as the Fed Chair. It was so widely applauded that quite literally everything went up. You know, like stocks, the fed funds futures, the dollar, the 2-year yield."

"So wait, if the entire market, except for stocks, thinks that the (Fed) taper will end sooner and rates are going to rise faster, how is that good for stocks? How is it good for stocks that the dollar is increasing as rates rise? Probably not so good. How is it good that the energy, materials, and industrials rallied to start the day with the dollar ripping higher and rising above resistance at 96.30, and now probably on its way to 97.70?"

"...the S&P 500 (SPX) seemed to catch on late in the day about the potential problems it is now facing. You know, like a high valuation, slowing EPS growth, slowing global growth, a strengthening dollar, and tightening financial conditions."

Kramer writes a daily column, so as is to be expected the currency of some of his remarks may be fleeting from time to time. But for what it's worth he writes, "I don’t know what else to say, if the only things the bulls have to hang their hat on its seasonality and inflows, then I just ask that the last one out please remember to turn out the lights. The party is over."

The trading day is about to get underway, I suspect it may be a windy one.

Have a good one, see you on Thursday.

{kind=link}