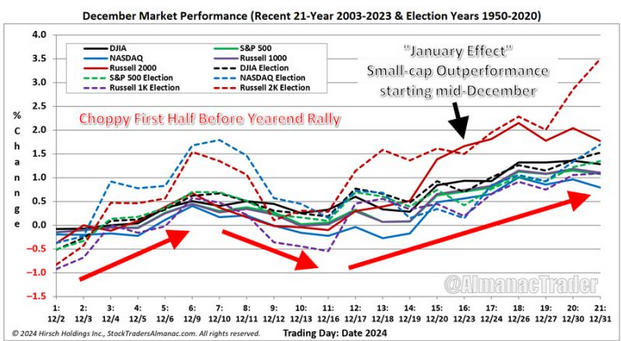

Something to keep in mind from Jeff Hirsch over at the Stock Trader’s almanac:

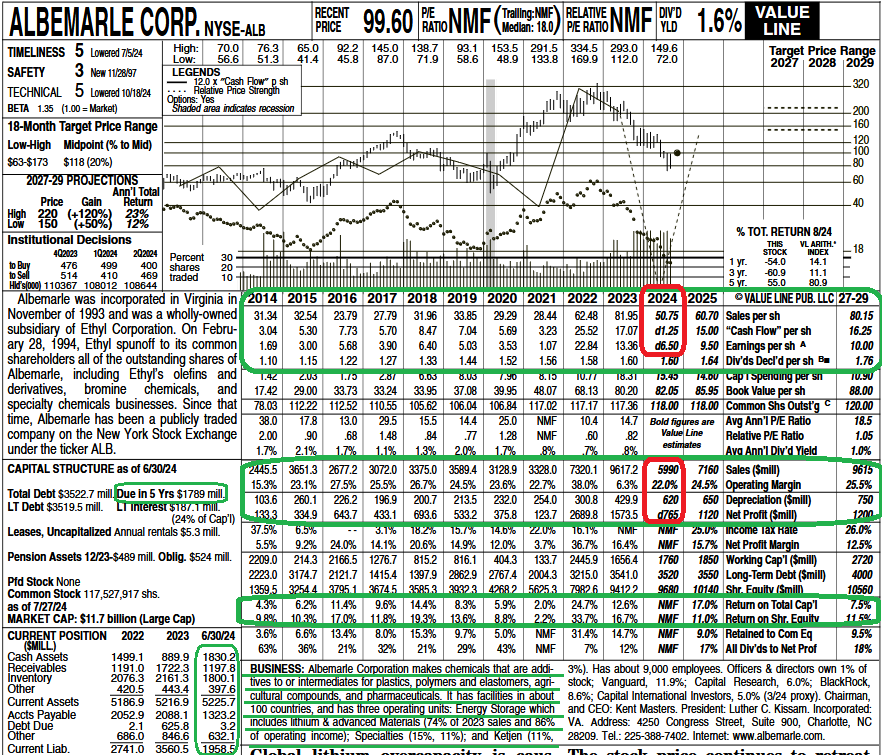

Albemarle Corp. (ALB)

Several months ago we discussed a new position in Albemarle Corp. (basis ~$93.22). It is not a large position yet because at the time of initiation there was limited excess (un-invested) capital to put to work. As new capital came in, price ran away from us. We don’t “buy up.” We do think we will get additional opportunities to size this position up as more data comes in, but if not, we’re okay with what we have.

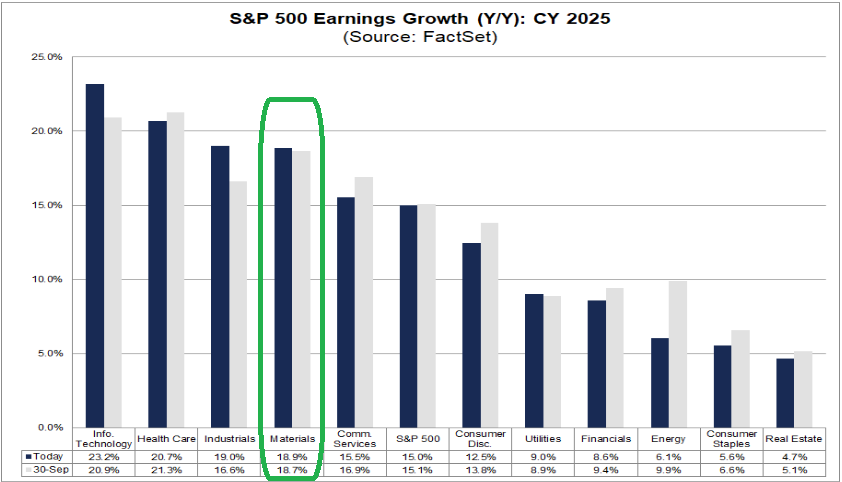

ALB is in keeping with our theme to find more “Materials” exposure in 2025 – as the sector has been decimated and earnings growth is expected to recover handsomely:

(Click on image to enlarge)

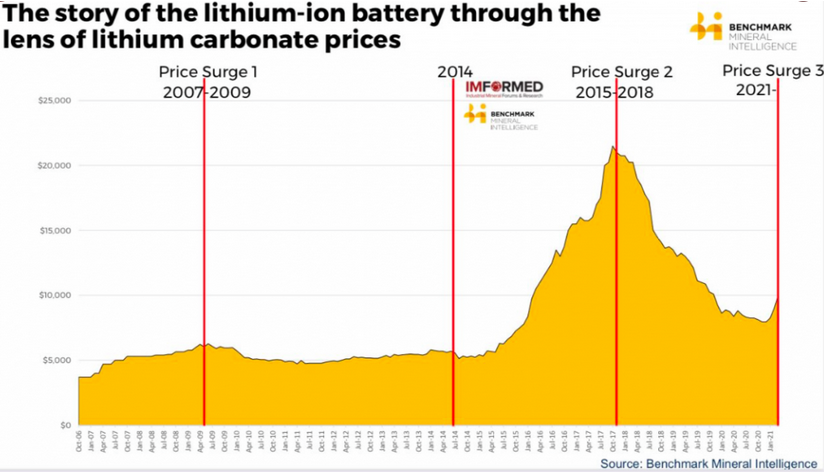

Albemarle’s primary business is Lithium production. We can see below the stock’s most recent spike and collapse in price (from 2021-2024) correlates with the spike and drop in price of Lithium Carbonate:

(Click on image to enlarge)

I generally avoid “commodity” stocks for this very reason (with the exception of Oil and Nat Gas stocks when I can buy the commodity cheaper on the NYSE than in the fields). I learned that tactic from J. Paul Getty in his legendary book “How To Be Rich.”

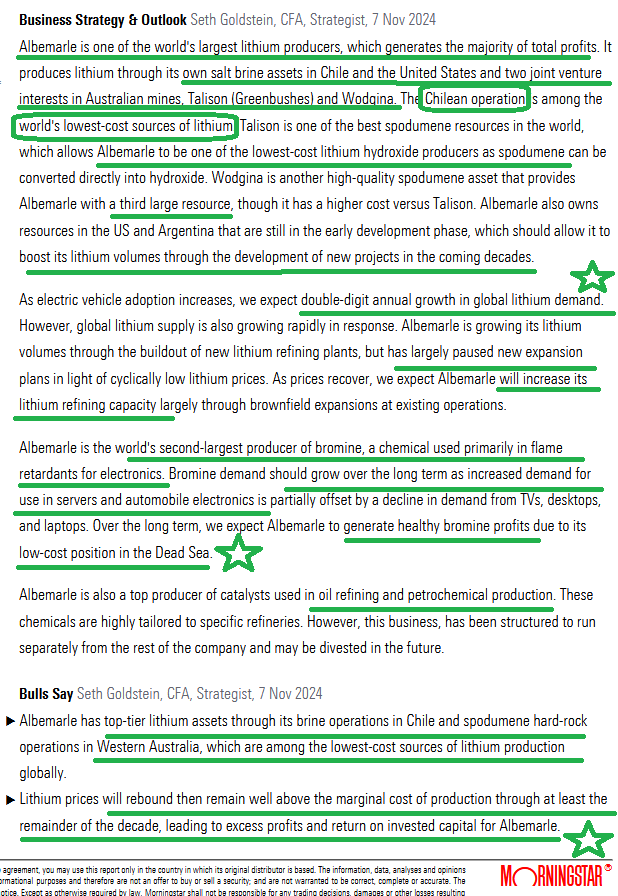

However, when you look at Albemarle’s long-term price chart, the correlation unravels. Albemarle historically has a moat around its business which – when executing at proper levels – can mint money irrespective of the price of the underlying commodity:

(Click on image to enlarge)

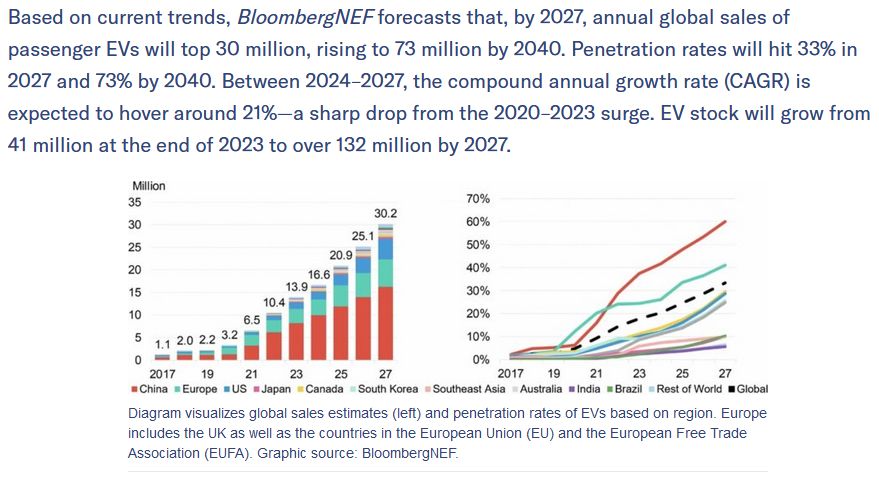

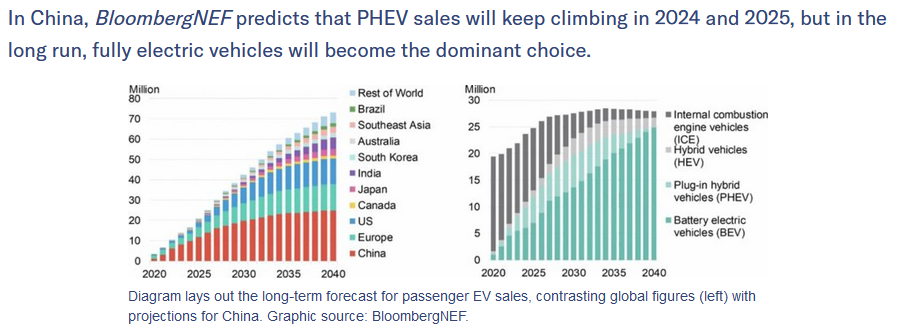

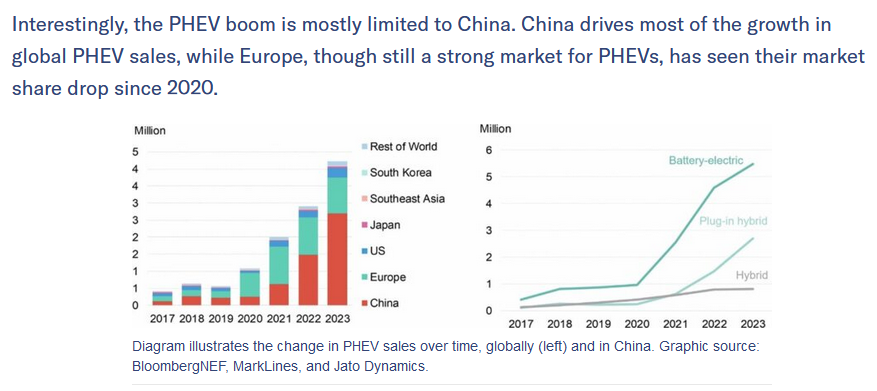

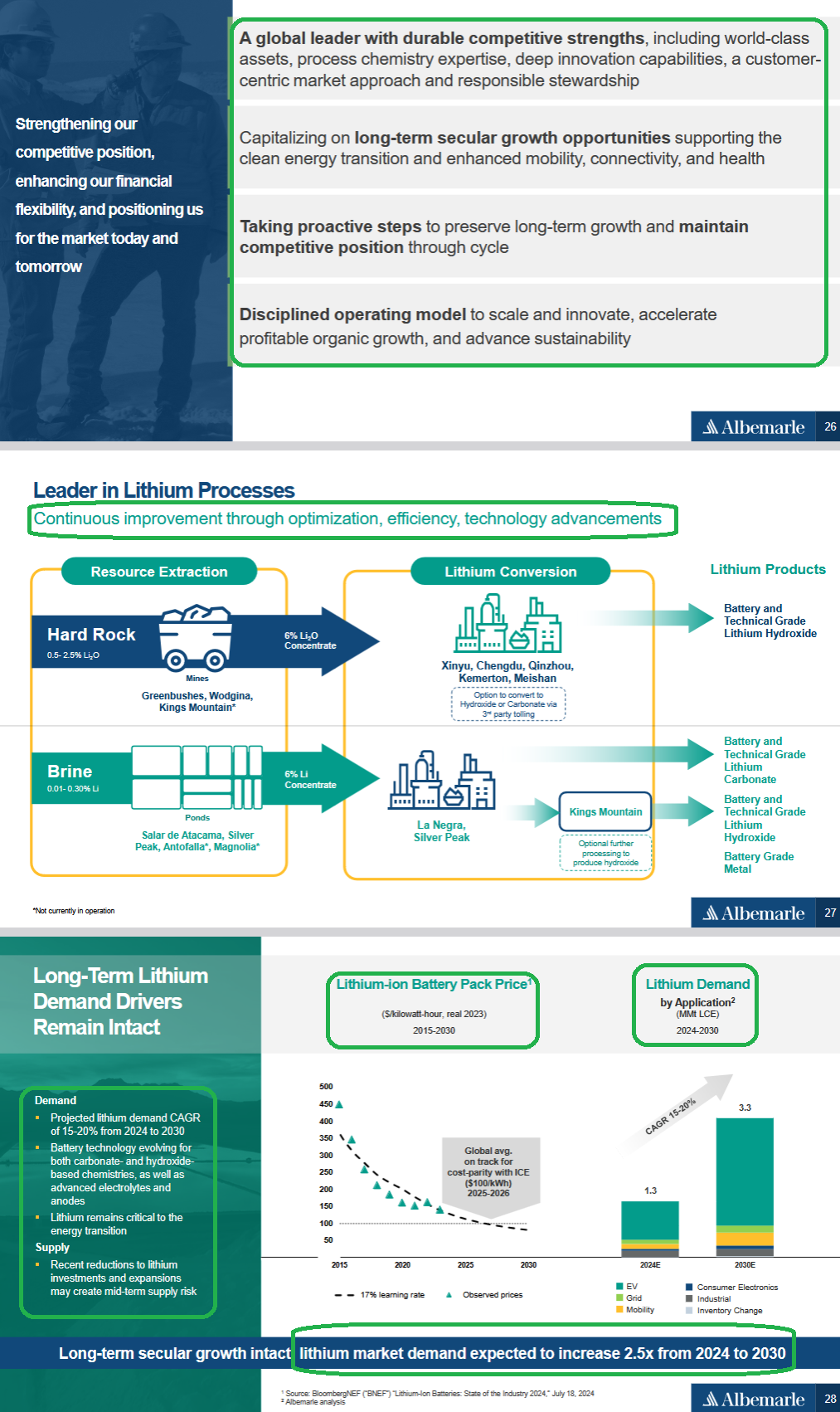

China’s appetite for EVs shows no signs of abating – even if N.A. sales have softened of late. If these estimates prove to be 25% true, ALB will not be able to handle all of the demand required in coming years:

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

2024 was an aberration due to short term global lithium overcapacity.

(Click on image to enlarge)

Turnaround Tactics:

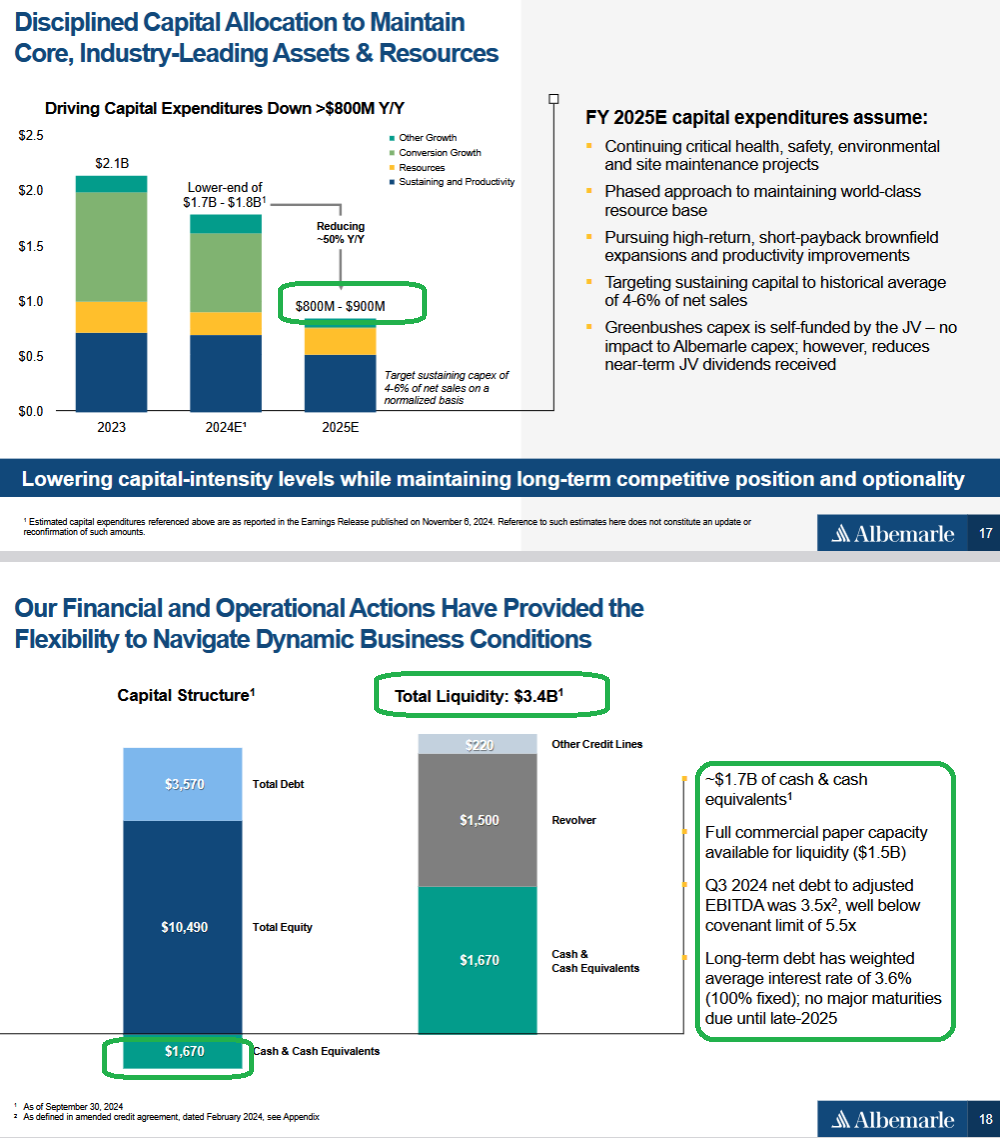

1. Management’s plan to reduce both operating costs and capital expenditures in response to cyclically low lithium prices.

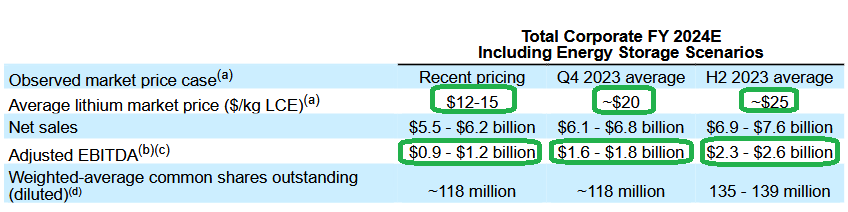

2. Management announced 2025 capital expenditures will be reduced by 50% versus 2024 levels. Albemarle is also implementing overhead cost reductions that should largely offset lower sequential realized lithium prices during the fourth quarter, with the majority of cost savings to be implemented in 2025.

3. Capex and cost reductions could drive profit growth and positive free cash flow generation by 2026 if lithium prices remain lower for longer.

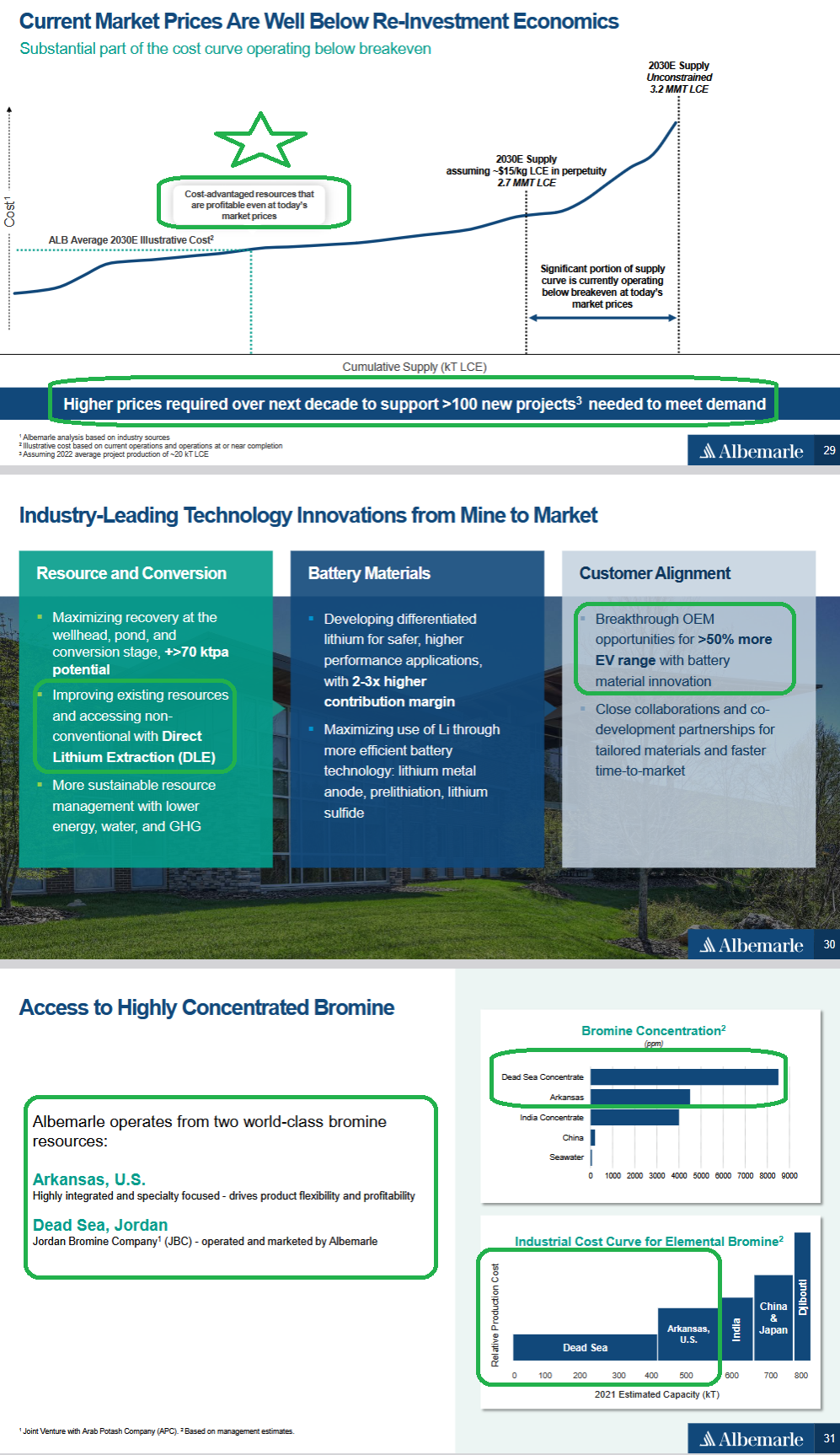

4. Lithium carbonate prices remain at multiyear lows, around $10,000 per metric ton on an index basis.

5. End market demand continues to grow. Global electric vehicle sales are set to grow in 2024, and utility-scale batteries used in energy storage systems are seeing strong demand growth, driving lithium demand higher.

6. In response to low prices, many producers, including Albemarle and its peers, are cutting supply. We expect the market will return to balance in 2025 from a current supply deficit.

Investor Highlights

(Click on image to enlarge)

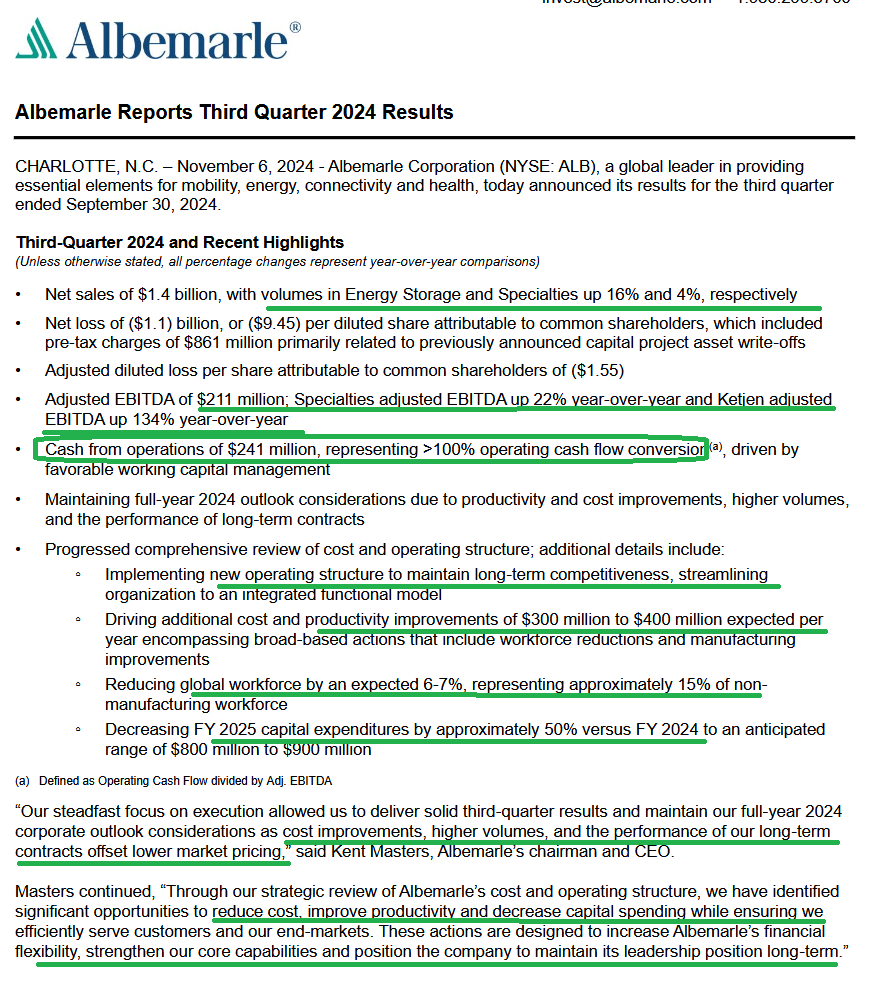

Q3 Highlights

(Click on image to enlarge)

General Market

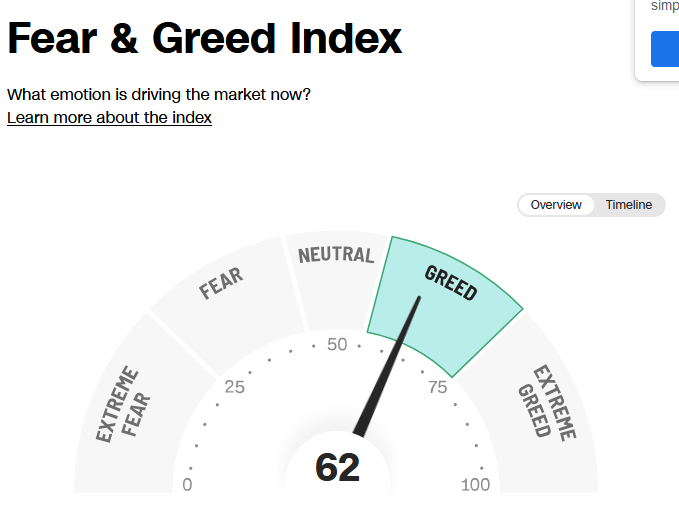

The CNN “Fear and Greed” flat-lined from 64 last week to 62 this week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

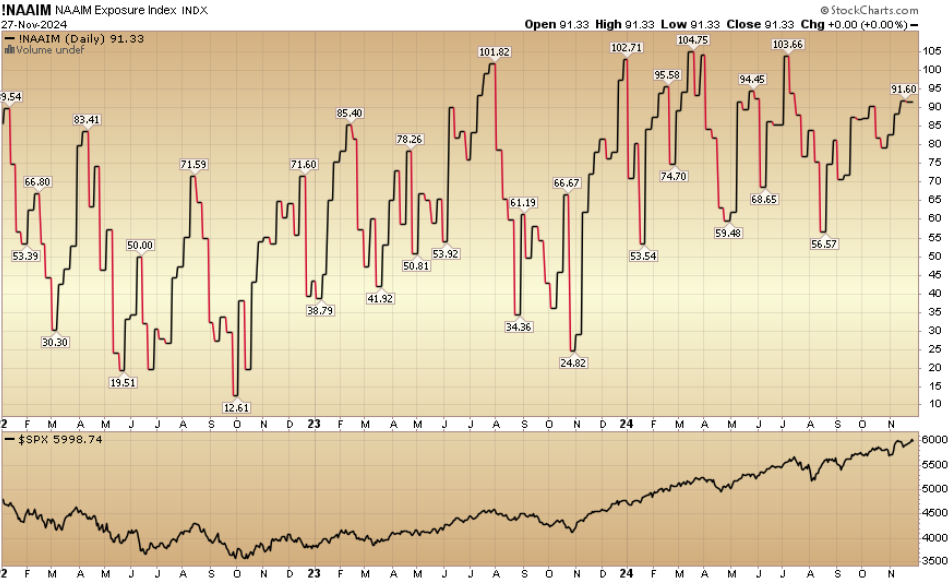

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) flat-lined at 91.33% this week from 91.60% equity exposure last week.

(Click on image to enlarge)

More By This Author:

“Turkey Or Goose?” Stock Market (And Sentiment Results)

“It’s All About Confidence” Stock Market (And Sentiment Results)…

“Tis The Season” Stock Market (And Sentiment Results)

Comments

Log in or sign up to join the conversation.