There was some selling of bonds yesterday, and it feels a bit vulnerable here considering the decent total returns recorded year-to-date against all odds given monetary tightening and the future recession risk. There is also a pre-FOMC and pre-ECB theme in the air. Many will wait to get the central bank(s) assessment of things before pulling the trigger.

ECB President Christine Lagarde and Fed Chair Jerome Powell

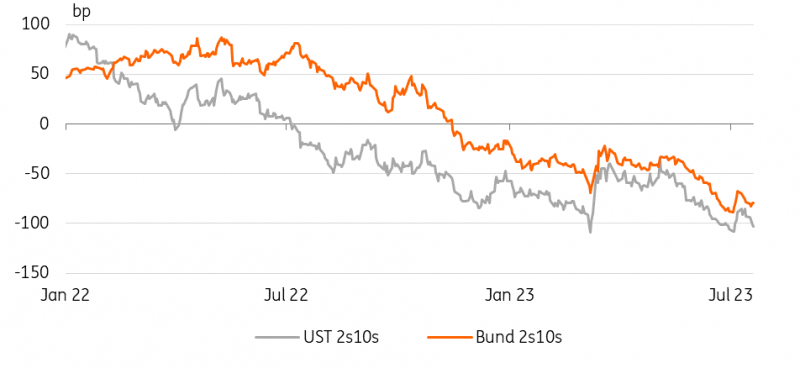

Long duration buying in the past month morphs to a selling tendency

Most of the past month has been dominated by bond buying, typically long duration in nature.

The same has been seen in corporates, and there has also been a decent bid into high-yield bonds. A glance at total return year-to-date show some impressive bond market performances, led by higher beta products. There are always profit-taking risks attached to this. A lot of the buying in the past month or so had helped to keep core yields from getting too carried away to the upside.

But yesterday more selling than usual was seen for a change, in particular out of Asia. This was a factor in unleashing Treasury yields higher. The low jobless claims number pushed in the same direction, but would not have been enough as a stand-alone to push the 10yr yield from 3.75% to 3.85%. And other data today has in fact been quite muted or negative for the economy.

The terminal discount for the funds rate also remains elevated, with the Jan 2025 future still above 3.75%. That keeps the pressure focused on the upside for market rates. The 4% level for the 10yr Treasury yield is firmly in focus here, likely post next week's FOMC outcome; at least we'll likely need to get through that first.

Closing in on cycle peaks

With inflation dynamics looking more encouraging, the general notion is that central banks are close to their cycle peaks in terms of tightening. If we look at current pricing, the market is seeing a good chance that the Fed will deliver its final hike of the cycle next week. Historical patterns suggest that a re-steepening of the yield curve led by the front end then followed as recession eventually ensued. And indeed, if it were to go by the Conference Board's Leading indicator, which posted another drop yesterday, we would have been in recession for a long time already.

However, the context looks somewhat different this time, as some parts of the economy still look unusually resilient. And markets are seeing a growing likelihood of a soft landing, which itself limits the drop in front-end rates as less aggressive rate cuts are then needed. On the flip side, that resilience continues to harbour potential upside risks to inflation. And central banks will therefore tread more cautiously and not take any chances. They are sensitive to their poor track records of forecasting inflation in the past and are basing their policies on current inflation dynamics rather than their models.

Curves have reflattened over past weeks, a clear steepening signal remains elusive

Refinitiv, ING

Fed and ECB set to hike next week, but signalling is key

The Fed and European Central Bank policy-setting meetings are the clear highlights of the upcoming week. The market is attaching a close to 100% probability that both central banks will increase their key interest rates by 25bp. Therefore, the signalling for the subsequent meetings is more relevant for price action.

The Fed had flagged another hike beyond July in its own dot plot. Markets remain more sceptical about such an outcome and attach a roughly one-in-three possibility. Our economist believes that this second hike will eventually not materialise.

Similarly, the ECB has sought to signal that a hike in September remains a viable option, and also our economists think the ECB is likely to hike once more after July. The market is less sure whether that hike will happen in September or come a little later in the year, but overall sees a roughly 90% chance that the depo rate will reach 4%.

The Fed and ECB are unlikely to call an end to their respective tightening cycles, but we will listen more carefully to the nuances around the balance of risks surrounding the central banks’ outlooks. A few data points, especially concerning the ECB, could still influence the degree of determination that policymakers might want to convey. Monday will see the release of the flash PMIs. Tuesday sees the ECB’s quarterly bank lending survey, which will provide a better view of the effective policy transmission thus far.

Only after the meetings will we get more inflation data. The first preliminary country inflation readings for July will be reported out of France and Germany on Friday. That day we will also get the June core PCE deflator, the Fed’s favoured inflation measure, which follows the second quarter GDP report a day earlier.

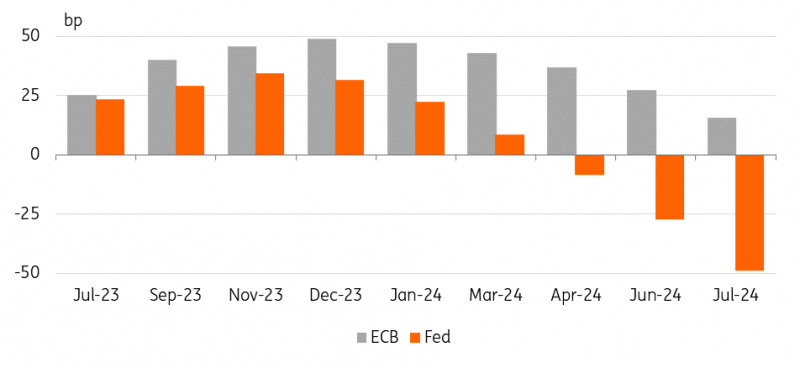

The July hikes are a done deal, but future hikes hang in the balance

Refinitiv, ING

More By This Author:

Collapse Of Grain Deal Rattles The MarketFed To Keep Up The Squeeze With Another 25bp Hike

FX Daily: Dollar Bears Being Asked For Patience

Comments

Log in or sign up to join the conversation.