From WSJ:

“It’s the ‘Godot’ recession,” said Ray Farris, chief economist at Credit Suisse. Mr. Farris found himself among a small minority of economists last fall who predicted the economy would narrowly skirt a downturn this year. Every six months, economists have predicted a recession six months later, he said. “By the middle of the year, people will still be expecting a recession in six months’ time.”

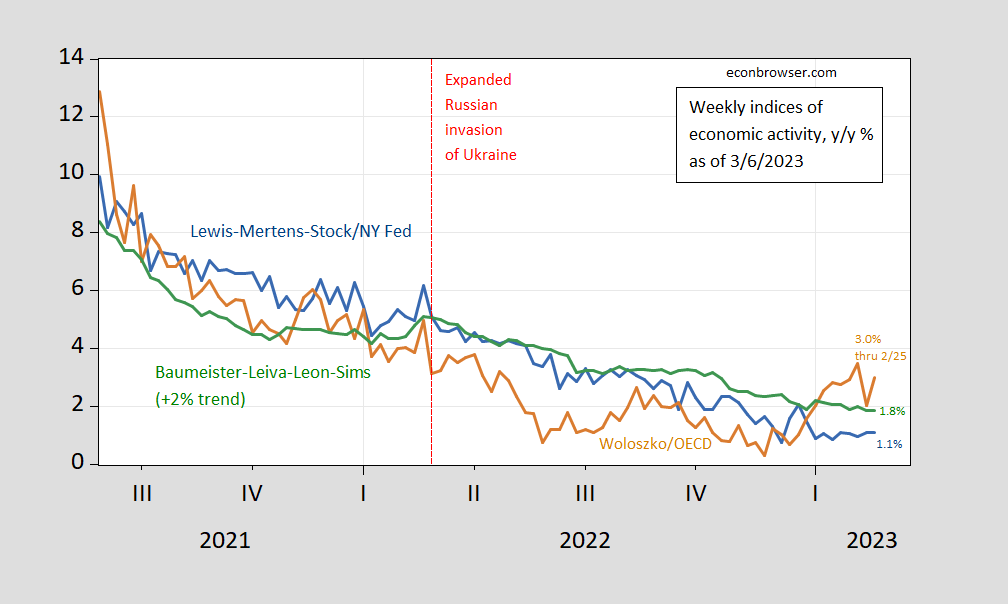

The article refers to a set of indicators (you can see monthly in this post), but here are the latest weekly indicators – the Lewis-Mertens-Stock Weekly Economic Index, the Baumeister-Leiva Leon-Sims WECI, and the OECD Weekly Tracker, for data through 2/25.

(Click on image to enlarge)

Figure 1: Lewis-Mertens-Stock Weekly Economic Index (blue), OECD Weekly Tracker (tan), and Baumeister-Leiva-Leon-Sims Weekly Economic Conditions Index for US plus 2% trend (green). Source: NY Fed via FRED, OECD, WECI.

The Weekly Tracker, which had dipped into negative for the week ending 11/26, now at 3% exceeds the WEI (1.1%) and WECI+2% (1.8%). The WEI reading for the week ending 2/25 of 1.1% is interpretable as a y/y quarter growth of 1.1% if the 1.1% reading were to persist for an entire quarter. The Baumeister et al. reading of -0.2% is interpreted as a -0.2% growth rate in excess of long term trend growth rate. Average growth of US GDP over the 2000-19 period is about 2%, so this implies a 1.8% growth rate for the year ending 2/11. The OECD Weekly Tracker reading of 3.0% is interpretable as a y/y growth rate of 3.0% for the year ending 2/25.

The OECD Weekly Tracker continues to rise, even as the other two series slowly decline. It’s important to remember the WEI relies on correlations in ten series available at the weekly frequency (e.g., unemployment claims, fuel sales, retail sales), while the WECI relies on a mixed frequency dynamic factor model. The Weekly Tracker — at 3.0% — is a “big data” approach that uses Google Trends and machine learning to track GDP. As such, it does not rely on actual economic indices per se.

Returning to the recession forecast, Prakken and Herzon at S&P Global Market Intelligence (nee IHS Markit) write in today’s US Forecast Flash:

− S&P Global Market Intelligence revised up its forecast of real GDP growth for 2023 from 0.7% to 1.0%, meas-ured year-over-year.1 The revision mainly reflects an upward revision in our estimate of Q1 growth, from – 1.3% last month to -0.4% this month, driven by unex-pectedly strong consumer spending in January that was only partly offset by downward revisions in net ex-ports and inventory investment.

We expect the economy to contract just 0.1% in Q2, when a countercyclical rebound in vehicle production will add approximately 0.6 percentage point to GDP growth. While the base forecast does show two con-secutive quarterly declines in GDP, the episode might be better characterized as a pause in activity rather than an outright recession, as output falls just 0.1%over the two quarters. Positive but below trend growth resumes in the second half of the year.

More By This Author:

Russia: Waiting For Inflation?

Output: Where We’ve Been And Where We Are Relative To Potential

If The Housing *Is* The Business Cycle, What Does This Picture Mean?

Comments

Log in or sign up to join the conversation.