Default rates & bankruptcies - are on the agenda as debt matures for quite a few companies. That's an issue to contend with during 'summer doldrums', as they're affectionately called, but that does mean a broad market impact.

That comment is emblematic of the concerns constantly trotted-out by 'bears', who I largely think are strategists or money managers actually looking to buy in the wake of disappointment, and genuinely fearful of 'earnings guidance' or improved results, that would mitigate or mostly offset influence from defaults.

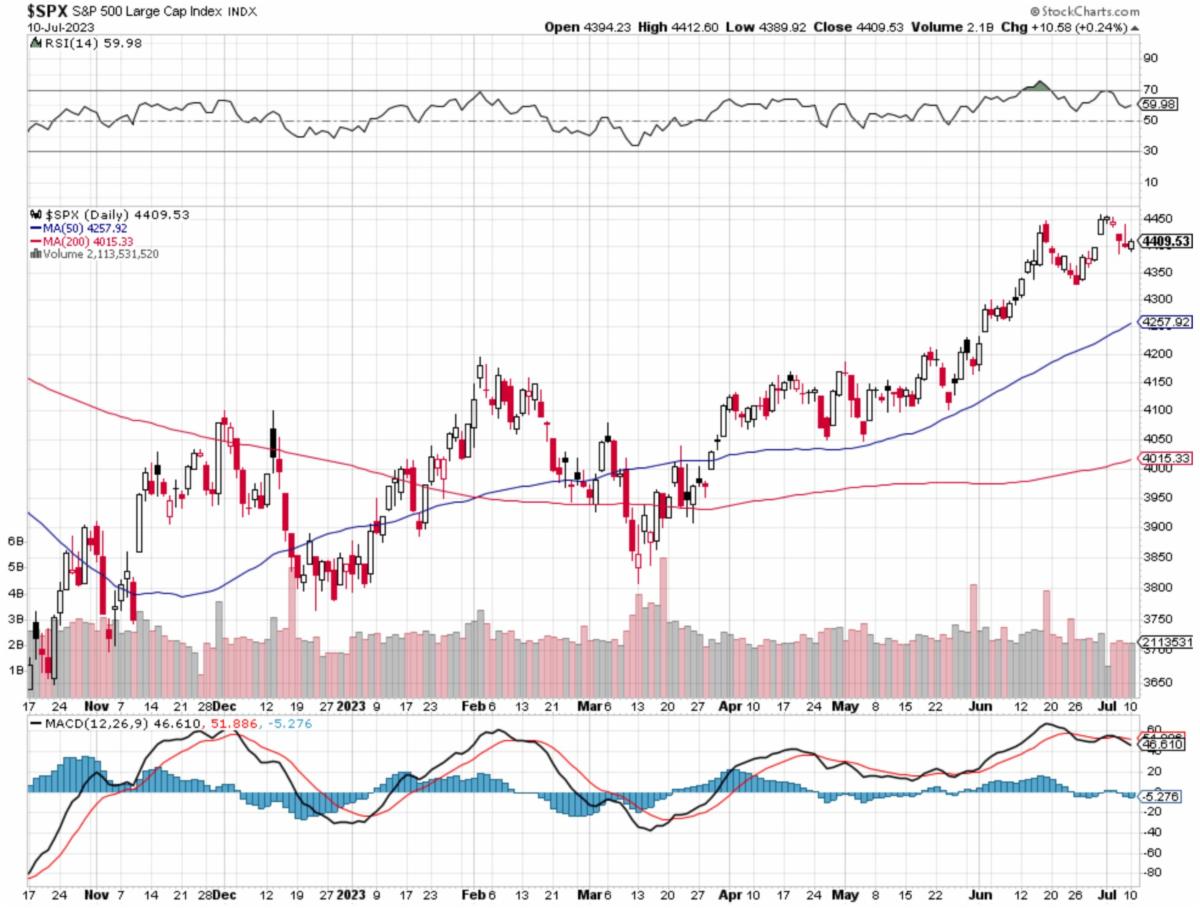

Simply put, 'if' CPI is lower (aside core 'food & energy'), there's a reasonable prospect of many small-cap stocks doing better than commonly contemplated and where they have unique (specialized) fundamental progress, even more.

I actually think the biggest story of the day, besides a secret Kremlin meeting we noted, might be the antics of Turkey's Erdogan. First he released leaders of the Azov brigade that he had promised Putin he'd hold (after surrender) to Zelensky who apparently flew to Turkey over the weekend to get them. Then Turkey ok'd Sweden joining NATO, after long opposing it. Well, we expected that (F-16's were quietly withheld), but I think now Turkey will 'need' F-16's as the Russians (if they still matter, and they do preferably with new regime in the future) will be rather angry. Oh well, Erdogan suddenly acting a bit more like he actually is a NATO member? We'll see where this goes and hopefully not at the expense of grain shipping deals through the Black Sea.

Among stocks not much news today, you know the Semiconductor issues as regards China, and you know we're awaiting CPI, AEHR info., and more. We do note that SOUN is acting a bit better (a normal percentage retracement in contrast to a retreat to a moving average), that BBAI is doing nothing but that can change, and LLAP is firming after initially dipping after the satellite news, and then right back up. Nothing is clearly defined with these, as we monitor.

You might also say that for tiny LPTH, which did (we are grateful) explain the difference between germanium and BD6 (their domestic replacement) via a descriptive LinkedIN post today. We continue to see it as a good back burner hold since the 1.20's (or briefly lower), and look for higher highs (2-3 minimum or more) depending on what they announce and when, and market climate.

In-sum:

There was not a lot pushing prices around on Monday. The narrow leadership is purported to be the 'reason' for a special re-balancing later this month among a few of the biggest (typical NDX component) stocks to avoid 'concentration'.

I do believe this impacts a few stocks we follow, although redistribution might be slightly a 'ding' on some (like Apple, Google or Microsoft) and a 'plus' for others, like possibly AMD and even Amazon (AMZN), all of which are in the NASDAQ 100, but only a handful would be impacted by 'concentration' sales (for being too high market value representation in the Index). So with the same amount of money at such a time, presumably it gets more spread-out to the others.

It is a bit arcane, but just looking at Apple (AAPL), you get a good idea why I bemoan concentration in a handful of stocks that allows just such disparity even within an Index, thus giving an impression of greater strength than exists broadly.

Certainly the over-worn question on Wall Street is whether earnings can hold up in this higher-interest-rate environment. I don't expect a 'rip roaring' market in Summer, but I also realize equity risk is not as severe as some bears tend to think (some bulls too), because small-mid-growth is where managers tend to look in expensive markets to find some value. That quest is continuing.

Bottom-line:

We're on hold with an upward bias ahead of CPI. Better breadth is a key factor in holding things together, especially while most pundits persist in calling for market declines. I get it, and you might see special 're-balancing' as a result of 'concentration modifications' have some slight impact.

I appreciate nearly all of you starting to follow me @stockseer on Twitter for intraday comments, as that's where I'm doing quick takes of markets, mostly in the morning. For now content will remain entirely complimentary.

More By This Author:

Market Briefing For Monday, July 10 '23

Market Briefing For Thursday, July 6

Market Briefing For Wednesday, July 5

Comments

Log in or sign up to join the conversation.