The wait is over, and President Trump has nominated Kevin Warsh to head the Federal Reserve. To better appreciate Warsh’s views on monetary policy and what they may entail for markets, we summarize a recent Wall Street Journal editorial he wrote, The Federal Reserve’s Broken Leadership. Our market-related thoughts are below the bullet points.

- Warsh believes that AI will unleash a productivity boom, leading to higher real wages, a lower debt-to-GDP ratio, and “be a significant disinflationary force, increasing productivity and bolstering American competitiveness.“

- He wants to redirect lending from speculative uses to productive ones. “Money on Wall Street is too easy, and credit on Main Street is too tight. The Fed’s bloated balance sheet, designed to support the biggest firms in a bygone crisis era, can be reduced significantly.”

- Changing banking regulations to level the playing field between small and large banks. “The Fed’s rules and regulations have systematically disadvantaged small and medium-sized banks, which has slowed the flow of credit to the real economy.“

From a market perspective, Warsh’s quote, “the Fed’s bloated balance sheet,” will make him appear hawkish to some. Beyond the editorial, he has stated on numerous other occasions that he doesn’t support QE unless under dire circumstances. That said, his opinion on the benefits of AI, favoring productivity over speculation, and his forecast of higher real wages, makes a case for disinflation and strong economic growth, which should provide for lower interest rates and a strong economic tailwind for asset prices.

It’s worth noting that Warsh was a Fed Governor during the financial crisis (2006-2011). He voted for the bank bailouts and the initial round of QE, as well as the more questionable second round.

What To Watch Today

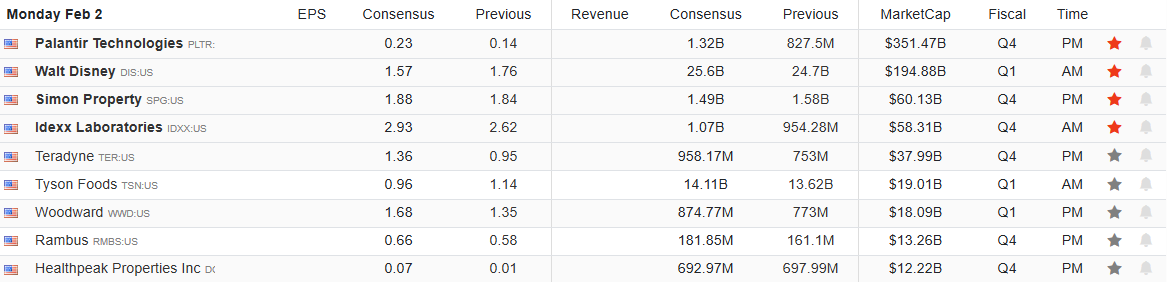

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

Market Trading Update

The S&P 500 closed the week at 6939, pulling back slightly from the highs it tested earlier in January. Price action remains constructive and in a bullish uptrend. However, recent sessions reflect continued resistance at all-time highs. Furthermore, market internals have softened, with relative strength negatively diverging from the bullish market trend. Such divergences typically precede weaker market outcomes, particularly when leadership has narrowed as earnings reactions from large-cap names have turned more mixed. While the index still holds above its key moving averages, the slope has flattened.

(Click on image to enlarge)

We are also closely monitoring market momentum, which has cooled in recent days, and breadth weakened under the surface. The percentage of S&P 500 stocks trading above their 50-day moving average declined over the past two weeks, while relative strength indexes are trending lower.

Volatility picked up last week, with daily intraday swings widening. The VIX remains suppressed, but skew has risen, suggesting investors are hedging downside risk. Options markets show increased demand for protection heading into this coming Friday’s January Employment Report. Technical support now sits near 6857, the 20-day moving average. A decisive break below would shift the short-term bias from neutral to defensive. Resistance remains firm at 7000. That range has rejected the price twice this month. A close above that level would suggest renewed upside momentum, especially if supported by strong earnings and macro data.

(Click on image to enlarge)

For now, the market is range-bound, waiting for confirmation. We have a lot of earnings reports this coming week, which could shift market sentiment. However, weak guidance or a hot jobs number could tilt sentiment more defensive. Positioning remains cautious, and until breadth improves, rallies may struggle for follow-through.

The Week Ahead

We have another active week ahead with earnings from some large companies and the monthly round of employment data.

Starting with economic data, the ISM manufacturing on Monday and the services survey on Wednesday will provide updates on corporate sentiment and their views on inflation and the labor market. On the labor front, JOLTS on Monday, ADP on Tuesday, and the BLS report on Friday are expected to show slightly better job growth, but still well below the employment-population growth rate. To wit, the BLS is expected to show 70k net new jobs, but the population of employable people is growing by roughly double that.

The top earnings announcements this week are as follows:

- Monday: Palantir and Disney

- Tuesday: AMD, Pepsi, and Merck

- Wednesday: Google, Qualcomm, Lilly, and AbbVie

- Thursday: Amazon

Mainstream Expectations: Hope vs Potential Risk

Mainstream expectations, those from Wall Street, economists, and corporate strategists, have congealed around a bullish economic outlook for 2026. Most forecasts project stronger economic growth, with contained inflation, and continued investment in technology and capital expenditure. As such, many institutional investors interpret this as a year of opportunity for markets and corporate earnings.That was a point we discussed at this year’s Investment Summit with the following slide.

But it isn’t just earnings that are expected to rise, but due to productivity increases (AI = Less Employment) corporate profit margins are expected swell to historic records.

However, whenever I see Wall Street becoming universally bullish, the contrarian investor in me is always reminded of Bob Farrell’s Rule #9:

When all experts agree, something else will happen.

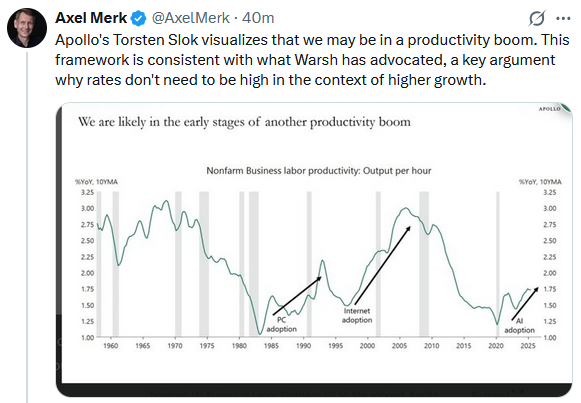

Tweet of the Day

More By This Author:

Meta And Microsoft: Great Earnings But Different ResultsMainstream Expectations: Hope Vs. Potential Risk

The Energy Sector Is Outpacing Energy Prices

Comments

Log in or sign up to join the conversation.