Mainstream expectations, those from Wall Street, economists, and corporate strategists, have congealed around a bullish economic outlook for 2026. Most forecasts project stronger economic growth, with contained inflation, and continued investment in technology and capital expenditure. As such, many institutional investors interpret this as a year of opportunity for markets and corporate earnings.That was a point we discussed at this year’s Investment Summit with the following slide.

But it isn’t just earnings that are expected to rise, but due to productivity increases (AI = Less Employment) corporate profit margins are expected swell to historic records.

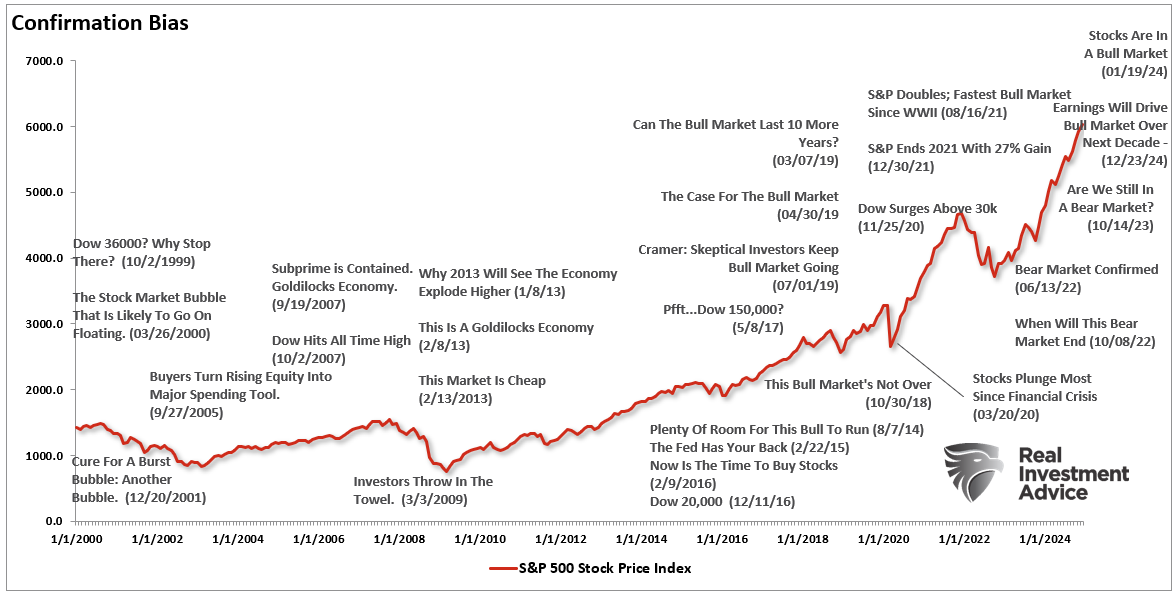

However, whenever I see Wall Street becoming universally bullish, the contrarian investor in me is always reminded of Bob Farrell’s Rule #9:

“When all experts agree, something else will happen.”

As I noted in that linked article:

“Excesses are built by everyone on the same side of the trade. Ultimately, when the shift in sentiment occurs – the reversion is exacerbated by the stampede going in the opposite direction.”

Yet the broader risk landscape is significant as consensus optimism obscures important vulnerabilities. When investors anchor on expected outcomes and overlook low‑probability but high‑impact risks, those risks become amplified. History shows that markets rarely transition smoothly from one year to the next without shocks to inflation, monetary policy, geopolitics, or credit conditions. For example, on January 1st, no one expected President Trump to slap additional tariffs on Europe over the potential purchase of Greenland.

But it happened.

So with that, let’s review mainstream expectations for 2026, and detail the “low probability, high impact risks,” that could derail the complacent expectations of investors.

US Economic Growth: Resilience or Fragile Expansion?

Mainstream Expectation: Most economists expect the US economy to grow above trend in 2026. Goldman Sachs forecasts U.S. GDP expanding about 2.6% year‑over‑year in 2026 compared to consensus estimates of roughly 2.0%. Their team sees above‑consensus growth and a strong rebound from 2025.

Other analysts and institutions, including PwC and RSM US, forecast similar growth in the 2.1% – 2.5% range, driven by consumer spending, corporate investment, and broader economic resilience.

Risk to That View: Growth forecasts assume stability in consumer demand, labor markets, and capital spending. But several risks could undermine this:

- Labor market fragility: Employment growth has slowed sharply in late 2025, and with a declining working‑age population due to lower immigration, net job creation may stay weak. Early data shows average monthly employment growth collapsing to levels historically consistent with labor market stress.

- Tariff and trade uncertainty: The recent threat of higher tariffs on Europe, and continued trade tensions that emerged in 2025, introduce volatility in production and pricing in supply chains. Increased tariffs across major trading partners historically correlate with lower output.

- Global headwinds: The World Bank warns that while global growth remains resilient, fading dynamism and policy uncertainty could reduce demand for U.S. exports.

Our view is that the most critical risk on 2026 is further weakness in the labor market or trade disruptions worsen which could cause growth to fall short of expectations.

Inflation and Monetary Policy: Tame or Sticky?

Mainstream Expectation: Consensus forecasts generally expect inflation to moderate through 2026, with core measures heading toward the Federal Reserve’s 2% target. Goldman Sachs projects core inflation close to 2.1% by the end of 2026.

Some money managers expect the Fed to cut rates one or two times in 2026, assuming inflation continues its downward trend and consumer spending remains resilient.

Risk to That View: Given that inflation is a function of economic supply and demand, a “run it hot economy” could keep inflation “sticky” or slightly higher.

- Sticky core inflation: Some forecasts warn that core inflation may stay above target due to tariff pass‑through, wage pressures, or service inflation. Vanguard’s model suggests core inflation could remain above 2.5% if tariffs and labor tightness persist.

- Monetary policy divergence: J.P. Morgan’s economist predicts the Fed may actually hold rates steady or even raise them in 2027, due to sticky inflation and labor market strength despite market expectations for cuts.

- Fed independence risks: Intensified concerns over central bank autonomy could cause further disruptions and uncertainty over future monetary policy direction.

If inflation proves more persistent than expected or if policy credibility erodes, interest rates may stay elevated weighing on valuations and economic activity.

AI and Corporate Investment: Growth Catalyst or Market Excess?

Mainstream Expectation: Most forecasts see continued strong investment in artificial intelligence and related infrastructure as a driver of both corporate capex and productivity. Most analysts highlight AI’s role in lifting corporate spending and supporting economic expansion.

U.S. corporate bond issuance is also projected to surge, much of it to fund AI data centers, advanced computing infrastructure, and next‑generation platforms.

Risk to That View: The growth from AI investment is uneven and concentrated:

- Concentration of benefits: A relatively small group of mega‑cap firms capture most of the AI investment gains, which can create sector concentration risk in markets and overstate the breadth of economic benefit.

- Corporate debt buildup: Higher bond issuance tied to capex, especially for large tech projects, increases leverage risk, especially if growth slows or credit markets retrench.

- Market pricing risk: A strong investment narrative can inflate asset prices beyond fundamentals, meaning corrections may be abrupt if earnings disappoint.

AI spending is real, but it is not a universal engine for all sectors. Most critically, the overreliance on it for aggregate growth forecasts underestimates broader economic weak spots.

Consumer Spending: Supported or Overstated?

Mainstream Expectation: Analysts expect consumer resilience to remain a backbone of 2026 growth. Strong household balance sheets, robust savings for certain income groups, and wage gains support consumption forecasts. These assumptions pervade GDP models showing above‑trend expansion.

Risk to That View: Consumer dynamics can shift suddenly:

- Wealth inequality in consumption: Wealth effects are most pronounced among higher‑income households. Median consumers without significant asset holdings may reduce spending if jobs or real income weaken.

- Debt and credit stress: Higher interest rates increase borrowing costs for households which could depress discretionary spending.

Consumer spending may remain resilient on average, but broad‑based weakness could emerge quietly before appearing in headline data.

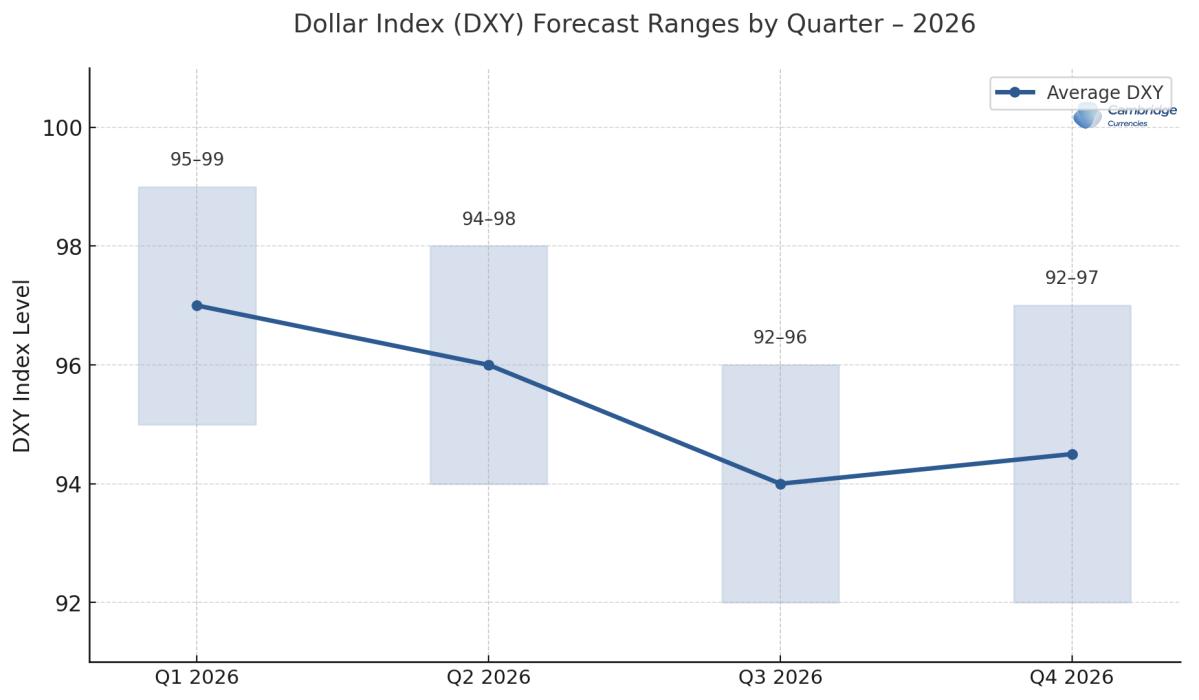

The Dollar and Foreign Exchange: Weakening or Volatile?

Mainstream Expectation: Many strategists anticipate a modest depreciation of the U.S. dollar in 2026. As such, a weaker dollar would boosts export competitiveness and corporate earnings abroad.

Risk to That View: Currency markets are driven by relative risk and capital flows, not just growth differentials:

- Growth risk: Stronger economic growth will attract foreign inflows into dollar-denominated assets for higher yields and relative safety.

- Safe‑haven demand: In times of geopolitical tension or financial stress, the dollar strengthens due to its liquidity and safety. Such would potentially hurt U.S. export competitiveness.

A dollar that strengthens through risk aversion or economic growth would undercut the export growth assumptions embedded in current forecasts.

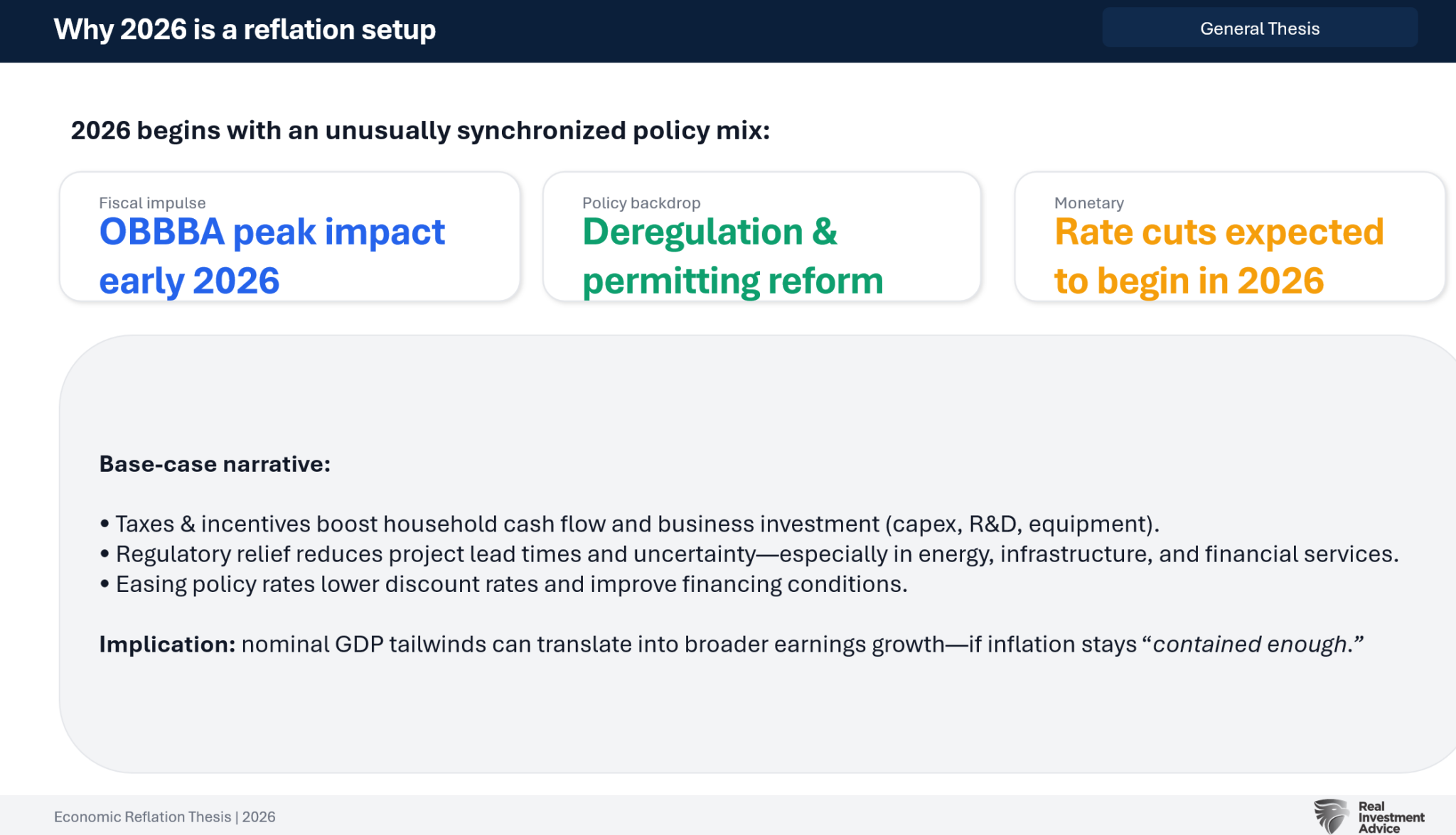

Tax Policy and Fiscal Stimulus: The Reflation Narrative

Mainstream Expectation: New tax measures, including expanded investment credits and incentives, are expected to boost consumer incomes and corporate spending in 2026. Forecasts incorporate these fiscal tailwinds into growth and profitability models.

Risk to That View: Tax benefits often provide short‑lived effects:

- Timing and bias: Households may smooth additional tax savings into future consumption rather than immediately spend them. Corporations might repatriate savings or use them for share repurchases rather than investing.

- Dependence Risk: The outlook for increased capex, spending, and earnings are all dependent on economic growth strengthening into 2026. However, as discussed, there are many risks to that view.

Tax incentives are supportive, but they should be viewed as marginal boosts rather than transformational drivers of long‑term growth.

Portfolio Tactics for Investors in 2026

The purpose of this article is not to suggests that Wall Street analysts, and market participants, are wrong. The purpose is to suggest there are risks to investor portfolios when “everyone is bullish on everything all at once.”

Therefore, given the range of possible outcomes, investors should employ adaptive, risk‑aware strategies. Rather than assuming a base‑case forecast will materialize, use portfolio tactics to help navigate uncertainty:

- Diversification Beyond Tech and Growth: Hold a mix of sectors including value, energy, and financials to reduce concentration risk. Consider allocations to fixed income to offset volatility risks.

- Inflation and Rate Risk Hedging: Maintain allocations to short‑duration bonds to reduce sensitivity to potential rate volatility.

- Dollar and Currency Exposure Management: Hedge currency risk for international holdings. A stronger dollar could undermine international growth outlooks.

- Energy and Commodity Positions: Commodities are subject to economic growth. If growth slows, commodities become a higher risk asset.

- Quality and Balance Sheet Strength: Tilt toward companies with strong balance sheets and stable free cash flow to weather cyclical shocks. Favor dividends and cash returns in uncertain environments.

- Liquidity Reserves: Maintain higher levels of cash or cash equivalents to capitalize on market dislocations. Liquid reserves provide flexibility should growth disappoint.

- Tactical Hedging Strategies: Use options or inverse instruments selectively to protect portfolios against sharp downturns. Volatility may rise unpredictably; structured hedges can provide protection without full market timing.

- Monitoring Macro Signals Actively: Track inflation metrics, labor market data, and Fed communications closely. Be ready to adjust strategies in response to shifts in inflation, policy, or geopolitical developments.

The mainstream outlook for 2026 is cautiously optimistic, grounded in forecasts of steady growth, stable inflation, and continued technology‑led investment. Those expectations are reasonable as base cases. However, investors should not mistake forecasts for outcomes. Each major economic assumption carries material risks. Persistent inflation, monetary policy uncertainty, geopolitical shocks, and uneven growth dynamics could all lead to outcomes well outside consensus expectations.

Prudent investors will build portfolios that protect capital first, anticipate volatility, and adapt rapidly to changing economic realities. The probability distribution of 2026 outcomes is wide, and mistakes can be costly when “all the experts agree.”

More By This Author:

The Energy Sector Is Outpacing Energy PricesEuropean Buyers Strike Or Performance Chasing?

Do Sentiment Trends Boost Reflation Odds

Comments

Log in or sign up to join the conversation.