Tuesday Talk: Gaining Again

The market ended last week on an up note and continued to climb yesterday. It seems that September's and early October's wounds have healed. Hard to be sure, but those Israeli Ever Ready Bandage Battle Dressings are out of stock on Amazon for the time being.

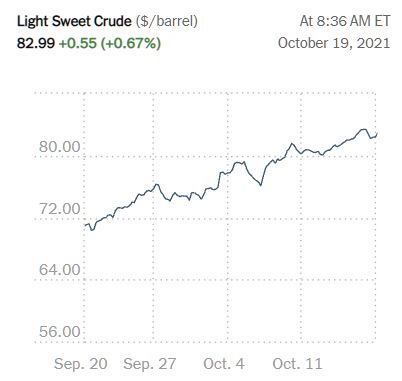

The S&P closed at 4,486 yesterday, up 15 points. The S&P 500 closed at 35,259, up 37 points, while the Nasdaq Composite closed at 15,022 up 125 points. Currently futures are green with S&P futures trading up 18 points, Dow futures up 140 points and Nasdaq 100 futures up 51 points. In commodities markets oil continues to be on a tear, as seen in the chart below:

Chart: The New York Times

TalkMarkets contributor Mish Shedlock says that Despite Widespread Belief In Strong Inflation, The Long Bond Suggests Otherwise.

"Yields are not close to inverting yet but the trend is recessionary, not inflationary. "

"That might look like a meaningless blip but it isn't. If there were inflation fears in bonds, it would manifest itself first and foremost at the long end. Instead, the long end of the curve is now falling while the 2-year rate is going up. This is a recessionary flattening of the curve that one should pay attention to."

Contributor Jeffrey P. Snider provides additional recessionary hints in Far Longer And Deeper Than Just The Past Few Months. Snider writes that current woes in industrial production and slowdowns in growth cannot be blamed solely on here and now events such as Hurricaine Ida or post-pandemic supply chain shortages. You really show read the article and take a look at the included charts, but here is some of what he has to say:

"Well, if not weather then certainly supply problems particularly semiconductors without which no one can finish much for vehicles. Domestic automobile production (Motor Vehicle Assemblies) fell below 8 million (SAAR) in September from a significantly downward revised 8.8 million the month before, dragging down the manufacturing sector. These are recessionary low levels."

"Long before recent American storms and well in advance of delta COVID. Italy had been the best of the European industry, but has struggled since last August. France going back to September 2020. Likewise Spain. Germany’s been in an industrial recession for all of 2021.

How about Japan? There was a clear inflection beginning around the same timeframe as Germany, January 2021, a setback that was fully set aside until April and then downhill from there.

In other words, the entire global industrial sector hasn’t just had a few bad months easily explained by recent weather and pandemic developments. This weakness is synchronized and it goes back only beginning with the Summer Slowdown of 2020. Further back several more years, none of these places has even sniffed previous highs from around the end of 2017 (middle of 2018 for the US)."

"The consistent picture I see is one of deflation and disinflation globally, and that view already misunderstood only further clouded by non-economic interference along the way (helicopters and such). For a few months, the idea of recovery and its inflation might have seemed reasonable maybe even probable given a cursory, surface analysis of this year’s CPI’s."

"There’s a reason why this L-shaped pattern repeats regardless of immediate circumstances. It isn’t supply bottlenecks or even COVID; those just robbed an already deflationary environment of that much more potential which has been continuously impaired going back to 2007 and 2008. Hole-within-a-hole-within-a-hole."

Be that as it may, it's hard to buy all of that in one gulp...

Elsewhere Talkmarkets contributor Bill Smead brings us to the intersection of government, stock markets, personal consumption and privacy in an Op-Ed of sorts entitled Zuckerberg’s Choice.

Smead writes: "We have entered the phase when the body politic and public opinion are aware that Facebook is disturbing our society. This is very important to us as investors, because the big tech companies make up a disproportionately large part of the S&P 500 Index. "

"The Sherman Antitrust Act was written and enacted because our early leaders were concerned about ruining this experiment in Democratic Capitalism. They felt that the most likely “disturbance” would be “the concentration of capital in vast combinations.” We believe we have reached that point with the FAANG stocks. Here is how Niall Ferguson describes Facebook in an article at Bloomberg.com:

I have met Facebook chief executive Mark Zuckerberg only once and it did not go well. It was at a dinner in July 2017, in the aftermath of Donald Trump’s presidential election victory, and controversy was raging about Facebook’s political role. I had the temerity to warn him that he increasingly resembled a cross between John D. Rockefeller and William Randolph Hearst. By that I meant that Facebook was in danger not only of going the way of Standard Oil, the favorite target of the trustbusters of the Progressive Era, but also of becoming as politically toxic as the Hearst newspaper group became in the heyday of yellow journalism."

Smead continues with an analysis of where Facebook is today in terms of government and anti-trust and makes some interesting comparisons to Solomon Brothers and Drexel Burnham Lambert. It is good reading; he concludes with these remarks:

"It seems that Zuckerberg has two choices. Will he fight the government and risk Facebook’s destruction or throw the company to the mercy of the court? Either way, the next few years will be quite entertaining in the world of Facebook (FB) and could tell other monopolistic companies like Google (GOOGL) and Amazon (AMZN) whether to fight the Federal government as it pursues the antitrust law."

Worth thinking about over a cup of coffee and trying to understand just when Facebook becomes a sell...

Getting back to the daily grind contributor Arthur Donner in a TalkMarkets exclusive, notes that The US Job Market And Economy Are Far From Healthy.

"US payroll employment increased by only 194,000 in September compared with increases of 366,000 in August and over 1 million in July. The unemployment rate, which is calculated from the Household Survey, declined to 4.8% in September from 5.4% om August and 5.4% in July. A broader measure of slack in the American labor market, the U6 unemployment rate, which accounts for both unemployed and underemployed workers, was 8.5% in September versus 8.8% in August. So, the jobs recovery has been slowing even though new job openings increased sharply to 10.9 million in September. "

"Indeed, policymakers must be a bit puzzled by the weak employment numbers when there are so many unfilled jobs eagerly seeking new employees. While the weak nonfarm payroll numbers might give pause to the Fed’s early plans to begin tapering on bond purchases, the large number of unfilled jobs and the recent reductions in new COVID cases seem to signal a virtual opposite conclusion."

It's a strange bubble indeed these large groups of prime age workforce folks not returning to the job market and it's not just in the U.S.. Burning through savings now that stimulus programs have run their course while holding out for higher wages seems an unusual endgame.

A few additional observations on the slowdown in the recovery are provided by TM contributor James Picerno who questions Is Weak US Industrial Output Flashing A Warning Sign?

Picerno starts off with this:

"Industrial production in US was surprisingly weak in September, falling a hefty 1.3% vs. the previous month – far below Econoday.com’s consensus point forecast for a moderate 0.2% rise. That’s worrisome, but monthly data is noisy and so it’s premature to read too much into one monthly update."

Picerno then dives into historical stats and charts such as "US Industrial Production During Expansion Since 1970" noting that, "... the current industrial expansion is still far ahead of rebounds in previous expansions since 1970. In other words, there’s still plenty of room for output to falter before it looks like a smoking gun for the economy."

Among the charts included in the article is the one below:

Picerno reminds us that, "Forecasts should be viewed cautiously, of course, particularly the further out in time the estimates run. As such, growth is likely to persist in the near term, but risk is on track to rise."

However since the markets do seem to be gaining again, it would be remiss not to close out with some positive investment food for thought which is brought to us by TalkMarkets contributor Marc Lichtenfeld who discusses The Secret To Successful Investing In Biotech.

"Have you ever had a stock jump 30%, 50% or 100% in one day?It’s an amazing feeling. It doesn’t happen often, but when it does, it’s almost always in the biotech sector. In fact, last Wednesday, Jasper Therapeutics (JSPR) soared 89% in one day. The reason it’s biotech companies usually making these giant moves is no other sector has such important catalysts that can instantly revalue a company."

Here are some companies that Lichtenfeld offers for consideration.

"There are plenty of companies with multibillion-dollar valuations that have no drugs on the market yet.

Compugen (CGEN) has a market cap of about $500 million. The company has no revenue, as it has no products on the market. Compugen has four drugs in its pipeline for the treatment of various cancers, including ovarian, breast and colorectal subtypes. The company is partnered with Bayer (BAYRY), Bristol Myers Squibb (BMY) and AstraZeneca (AZN) on several studies.

Celldex Therapeutics (CLDX) has a $2.3 billion market cap with three drugs in early-stage clinical trials.

Nektar Therapeutics (NKTR) trades with a $3.2 billion valuation and has four drugs in clinical trials – some of them in late-stage trials, so they’re closer to potential approval.

These are just a few examples to show you the potential increases for some biotechs. If Compugen grew to the size of Celldex, that would be more than a 300% gain. And it’s not like Celldex is Pfizer (PFE). Celldex has no products on the market."

Have a good week and as always, caveat emptor!

{kind=link}

Quite interesting, especially the assertion that there is not an inflation in process. Clearly the "method of selected data" is effective at obtaining the desired results in this case. That is to say that excepting food, fuel, and shelter from the determination will show an entirely different set of results.

But conclusions suggesting that a recession is more on the way can be used to provide an excuse for more inflationary pressures, and so would be expected. The appearance of recession in the bonds market is not an adequate excuse for degrading the currency used by the rest of the population. But it appears that the priorities of the fed differ from mine by quite a bit. Rather unfortunate!!