The US Fed has signaled that it would likely begin tapering its bond-buying program before this year’s end. Therefore, from a central bank perspective, the weak American employment growth figures for September must be regarded as very disappointing.

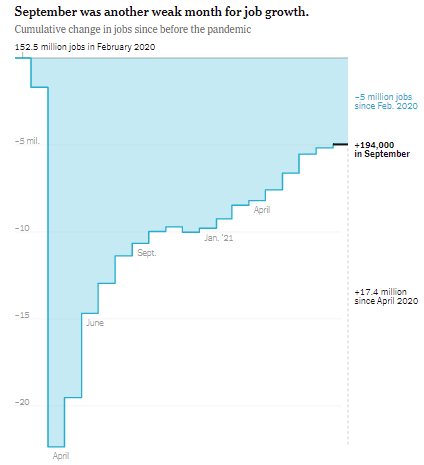

US payroll employment increased by only 194,000 in September compared with increases of 366,000 in August and over 1 million in July. The unemployment rate, which is calculated from the Household Survey, declined to 4.8% in September from 5.4% om August and 5.4% in July.

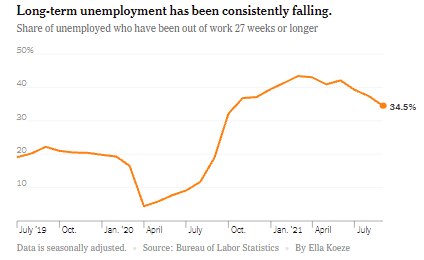

A broader measure of slack in the American labor market, the U6 unemployment rate, which accounts for both unemployed and underemployed workers, was 8.5% in September versus 8.8% in August.

So, the jobs recovery has been slowing even though new job openings increased sharply to 10.9 million in September.

A separate labor turnover survey also observed a steady increase in the number of workers voluntarily quitting their jobs, which is a sign of confidence in job market prospects.

Job shortages are also triggering increasing wage pressures, particularly in the leisure and hospitality sectors.

In other words, by some metrics, the US labor market is tight (elevated job openings, a high quit rate), yet by others, there is considerable unemployment and underemployment.

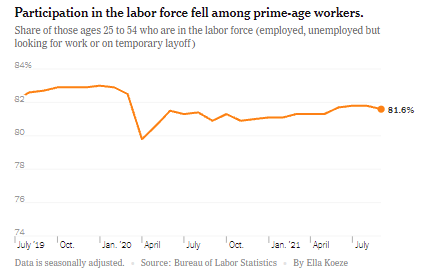

Adding to the confusing messaging from the recent data releases, a decline in September’s labor force participation rate provides a modest indication of slipping confidence (down to 61.6% versus 61.7% in August), while the employment-population ratio increased to 58.7% from 58.5% in August. The latter increase, of course, is a bit of a confidence booster.

It is interesting from a political and economic perspective that the decline in the labor force participation rate when some enhanced unemployment benefits expired didn't seem to convince former employees to re-enter the job market and look for work.

Indeed, policymakers must be a bit puzzled by the weak employment numbers when there are so many unfilled jobs eagerly seeking new employees.

While the weak nonfarm payroll numbers might give pause to the Fed’s early plans to begin tapering on bond purchases, the large number of unfilled jobs and the recent reductions in new COVID cases seem to signal a virtual opposite conclusion.

Comments

Log in or sign up to join the conversation.