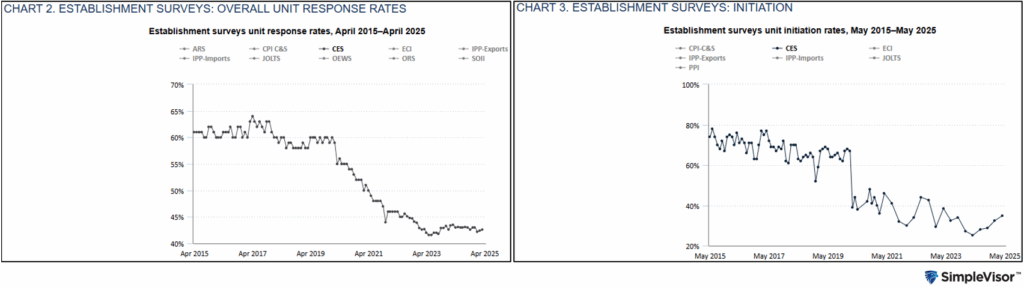

The White House has turned its attention to the Bureau of Labor Statistics after a series of steep payroll revisions rattled confidence in the government’s jobs data. President Trump fired the agency’s commissioner last month and has nominated a longtime critic to take her place, pledging reforms to improve accuracy. But the problems run deeper than leadership, and the Trump administration’s approach is unlikely to move the needle.

Survey response rates, once above 90% in the household survey, have slipped to around 70% in recent years. For the establishment survey, new business participation has collapsed from 78% a decade ago to just 35% today. A leading hypothesis? Survey fatigue: people are overloaded with voluntary questionnaires in the digital age. With fewer companies and households responding, revisions have grown larger: the gap between the first and third payroll estimates has nearly doubled since 2019.

At the same time, resources are shrinking. Adjusted for inflation, the BLS budget has fallen 13% since 2016, and Trump has requested another 8% reduction for the next fiscal year. Under Trump, the agency has even disbanded unpaid expert advisory committees that once guided modernization. As former commissioner Bill Beach opined, “there’s not much we can do to reverse declining response rates. We’ve tried everything.”

For investors, this means BLS data will likely remain noisy and prone to revision for the foreseeable future. Trump’s leadership changes and budget cuts may grab headlines, but the underlying numbers are unlikely to improve without a clear path to stronger participation and adequate resources to make it happen.

(Click on image to enlarge)

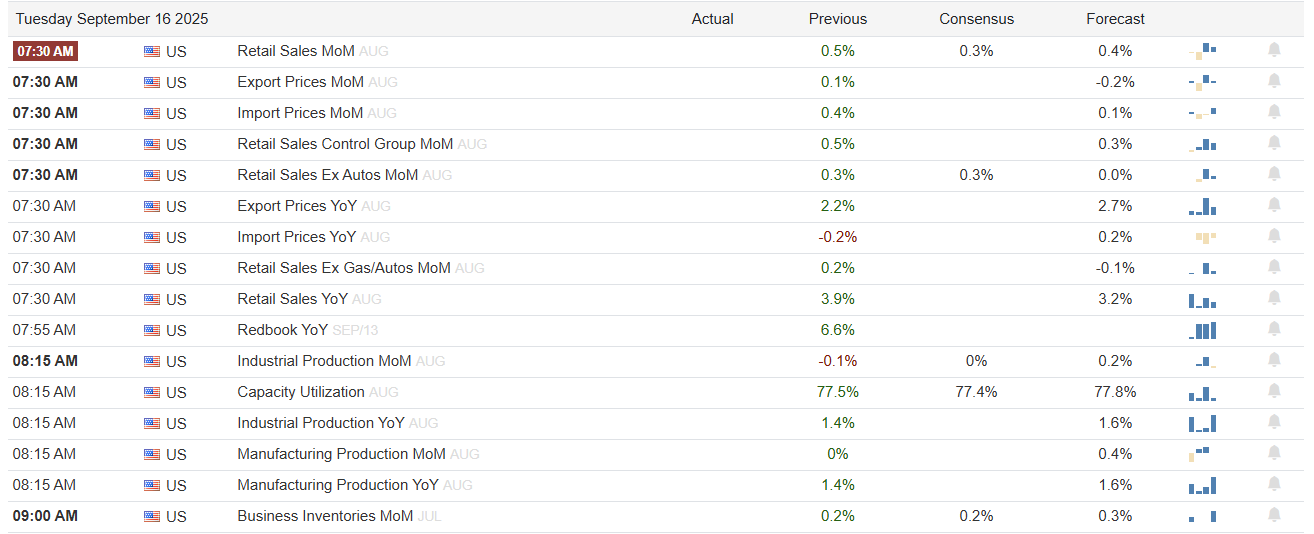

What To Watch Today

Earnings

- No earnings releases today

Economy

(Click on image to enlarge)

Market Trading Update

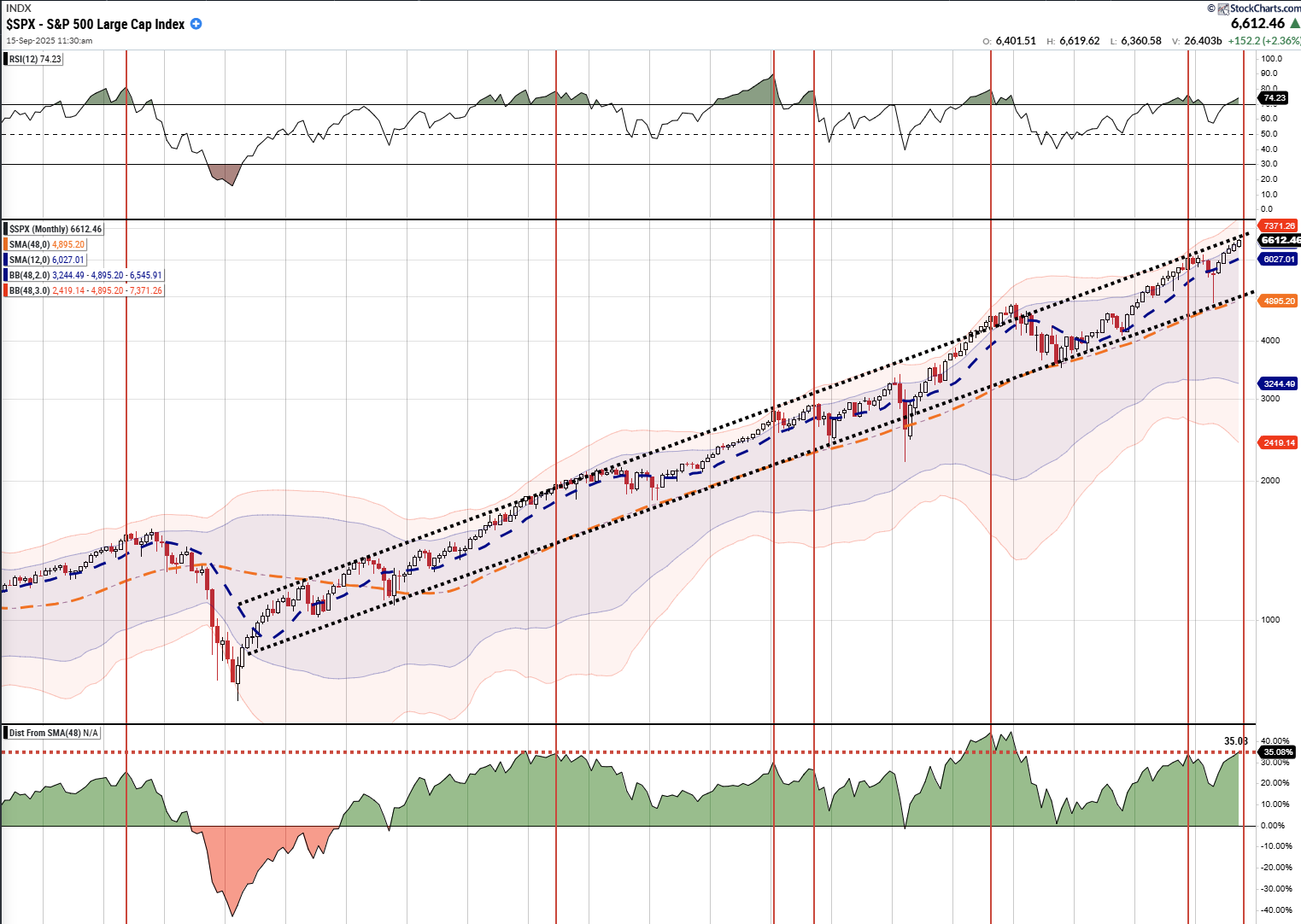

Yesterday, we discussed the S&P 500’s overall technical backdrop as we head into this week’s FOMC meeting. While bullish sentiment remains high, the market continues to drift higher on low momentum and volatility compression. Notably, there is nothing wrong with volatility compression, as it is a function of the bullish sentiment, which is currently driving the market. The problem is when something happens that “wakes” the bears, and there is a sharp reversal.

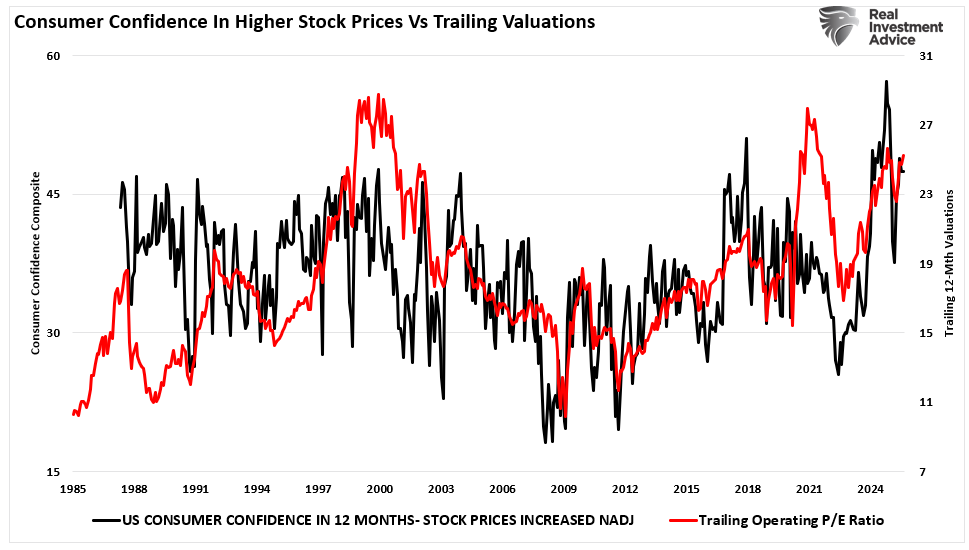

Consumer confidence in higher stock prices over the next 12 months also remains elevated, which supports higher valuations. In other words, investors are optimistic about stock prices going forward, so they are willing to overpay for earnings today, expecting the market to pay them tomorrow.

What this means is that as long as investors believe in higher asset prices, they can continue to propel markets higher. However, as shown in the monthly chart below, similar conditions have existed over the last 20 years that did not work out so optimistically. With the markets well deviated above the 4-year moving average, with complacency high, and the market overbought on many levels, reversions previously occurred. Will this time be different? It is always possible, but the odds of such an outcome seem spectacularly low.

(Click on image to enlarge)

I am not suggesting the market is about to crash. But with the market at the top of its long-term trend channel and well deviated and overbought, investors should at least consider the risk they are undertaking in their portfolios.

Trade accordingly.

Foreign Buyers Still Want U.S. Assets, Just Not the Dollar

Foreign investors are still buying U.S. assets, but trends show they are increasingly betting against the dollar’s strength. According to Deutsche Bank’s George Saravelos, currency-hedged flows into U.S. stocks and bonds are outpacing unhedged flows for the first time this decade. That shift helps explain why the dollar has weakened even as U.S. equities remain near record highs.

The S&P 500 is up more than 12% this year, but foreign indexes have surged by more. South Korea’s KOSPI is up 42% and Hong Kong’s Hang Seng nearly 32%. When translated back into dollars, the relative gains abroad are even stronger, giving investors reason to hedge against a falling U.S. currency.

With the Fed set to cut rates this week while other central banks remain on hold, the cost of hedging dollar assets will only get cheaper. That suggests continued demand for U.S. markets, but without the currency boost that has historically accompanied foreign inflows.

Invest Or Index – Exploring 5-Different Strategies

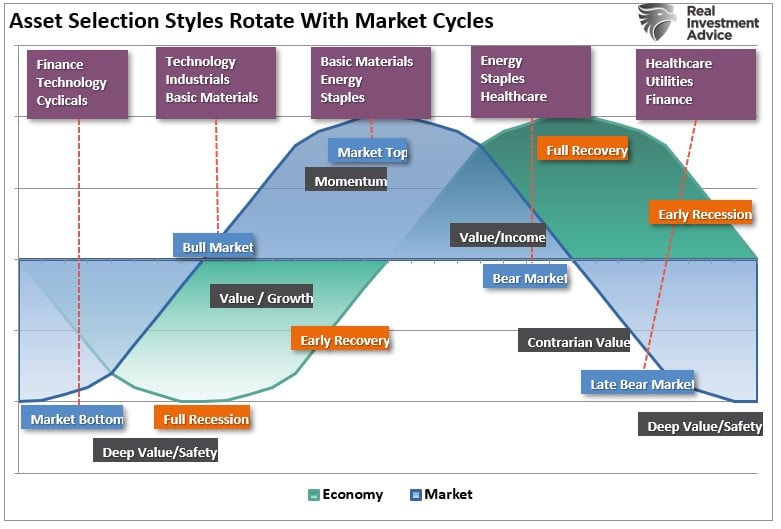

Investing is about choices. Every investor faces the same challenge: how to grow wealth while controlling risk. Over the years, distinct approaches have proven effective, though none guarantee success. Some strategies require patience. Others demand discipline in timing and execution. A few provide stability and income. There is no right or wrong way to invest, and every strategy has pros and cons. In some cycles, one approach will outperform another. That doesn’t mean a strategy is broken; it just means it is out of favor in the current environment. The problem that investors often face is that they abandon an underperforming strategy to chase another, often at precisely the wrong time.

The cycle rotation on investment strategies was discussed in detail in “Why Investing Is Like Gardening:”

Like everything in life, there is a “season” and a “cycle.” When it comes to the markets, “seasons” are dictated by the “technical and economic constructs,” and the “cycles” are dictated by “valuations.” The seasons are shown in the chart below.

Tweet of the Day

More By This Author:

Invest Or Index – Exploring 5-Different Strategies

Overnight Funding Costs Signal Liquidity Strain

Covered Call Strategies Gone Wild

Comments

Log in or sign up to join the conversation.