After years of abundant liquidity, U.S. overnight funding markets are beginning to show signs of strain. Interest rates on overnight repo agreements have climbed steadily this month as the Treasury rebuilds its cash balance and the Fed continues quantitative tightening. Usage of the Fed’s overnight reverse repo (RRP) facility, a key gauge of excess liquidity, has dropped to a four-year low. The result has been a widening spread between repo and fed funds rates, indicating that money market conditions are tightening. As recently noted by Bloomberg,

Since the beginning of September, the gap between repo and the federal funds rate has grown to about 11.5 basis points on average, the widest level since the end of April. That spread was in single digits in July and August as market participants were able to digest supply by shifting allocations to T-bills from repo.

The chart below clearly illustrates the impact of this year’s Treasury refunding on bank liquidity. With the overnight RRP facility now nearly empty, traders fear further stress as corporate tax payments and Treasury auctions settle this week, potentially draining more liquidity. Further, the Treasury is slated to ramp up bill issuance again in October. Standing repo facilities introduced after the 2019 “repocalypse” should prevent a disorderly spike in overnight repo rates. However, the risk of higher funding costs may be here to stay unless the Fed puts an end to QT.

What To Watch Today

Earnings

- No earnings releases today

Economy

(Click on image to enlarge)

![]()

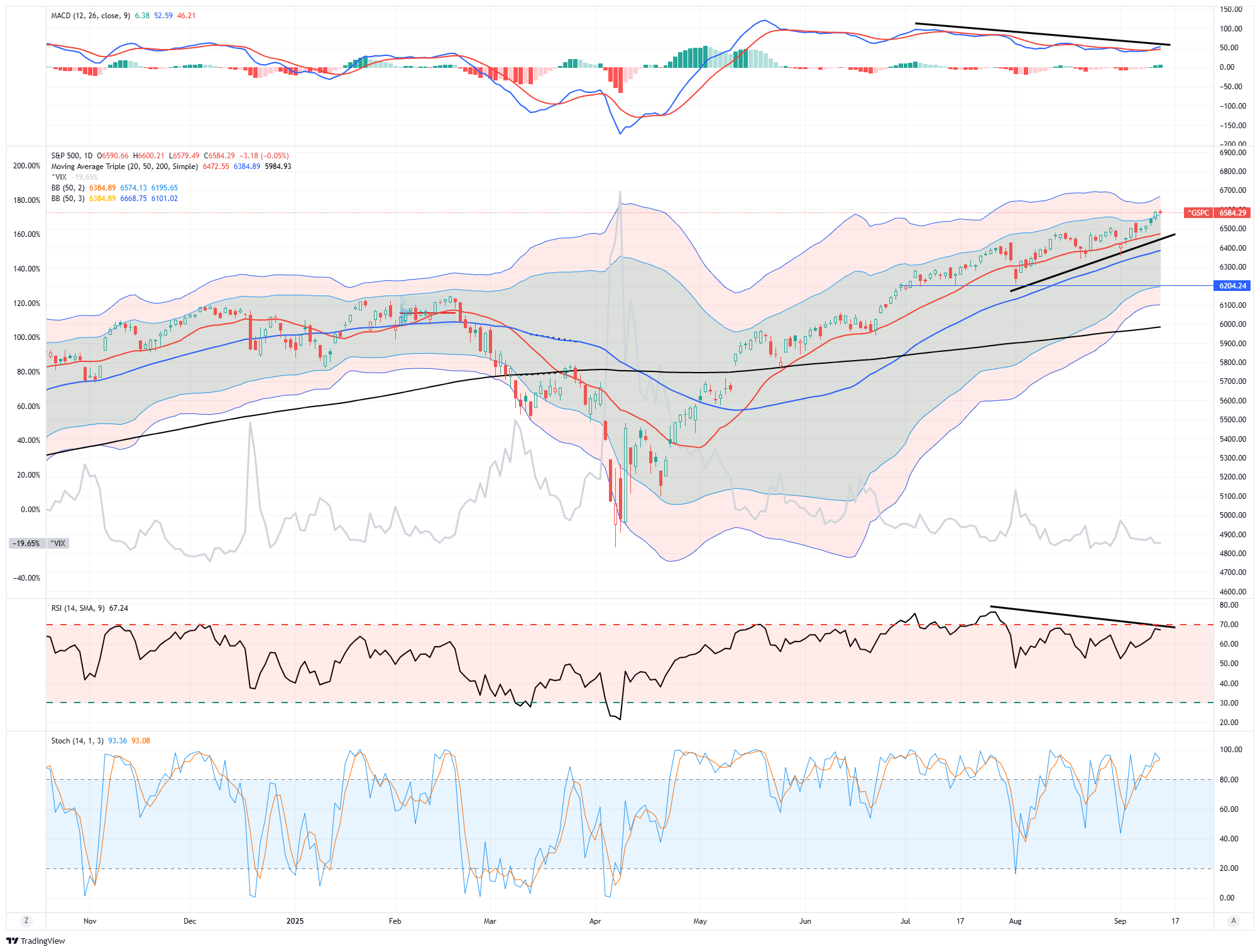

Market Trading Update

As noted, the markets interpreted the combination of sticky but cooling inflation and softer employment as supportive of a rate cut at the September FOMC. Equities extended their summer gains, with the S&P 500 hovering near record highs. As noted by Carson Research, the market has completed a 30% gain since the April lows, one of the fastest in history, which tends to bode well for further gains over the next few months.

But the most dramatic response came from the Treasury bond market. Yields fell sharply across the curve, with the 2-year Treasury, which tends to lead the Federal Reserve policy changes, dropping nearly 20 basis points on the week as traders priced in not just a 25 bps cut on September 17, but increased odds of additional easing into year-end. The two-year yield suggests the Fed is behind the curve in cutting rates by roughly 80bps.

The 10-year yield also slid, flattening the curve’s inversion, as investors anticipated slower growth ahead. This dovish repricing underscores how rapidly Fed expectations can shift when the labor narrative weakens, and it highlights the bond market’s role as the first responder to softer macro signals.

Technically, equity markets are holding up, but signs of fatigue are increasing. The S&P 500, after pushing toward and through recent resistance zones, is trading above its key moving averages of the 20, 50, and 200-day. For example, the 50-day has been rising steadily, supporting pullbacks, and the 200-day continues to anchor the long-term trend. On a shorter scale, recent days’ candles hint at smaller bodies and increased intraday reversals, suggesting that bulls are less aggressive at higher levels.

(Click on image to enlarge)

Momentum indicators continue their negative divergence as the market hit all-time highs this past week. We have noted these divergences over the last few weeks, but the market trend remains broadly bullish. Stochastic oscillators have shown instances of overbought conditions in small time frames, occasionally pulling back, but no major “sell signals” yet. Meanwhile, breadth remains a concern: new 52-week highs are fewer relative to all constituents, and many mid- and small-caps lag the large-cap/mega-cap names that continue to lead. In other words, the market increasingly relies on fewer names (often growth/AI- or tech-adjacent) for the advance.

Support and Resistance Levels: The S&P 500’s near-term support lies at the 20-day moving average (~6,500). The 50-day moving average is roughly in the ~6,400 region but there is deeper support near ~6,200, connected with the previous pullback. Resistance is around the most recent highs in the 6,600-6,700 area (2- 3 standard deviations above the 50-DMA). Notably, volatility (as measured by VIX) remains relatively subdued.

OUTLOOK: Neutral / Slightly Bullish with Guardrails – The trend is still up and technically intact. However, momentum is decelerating, and breadth remains a vulnerability. Traders should expect possible pullbacks or consolidation. Continue to risk-management practices.

The Week Ahead

It’s a heavy week for economic data and the Fed. Today kicks off with the Empire State Manufacturing survey, which is expected to remain in expansion after last month’s strong rebound.

Tomorrow, all eyes turn to retail sales, with expectations calling for another solid gain in the headline figure after July’s increase. Economists expect the retail sales control group, which feeds the GDP calculation, to soften slightly from July’s 0.5% increase. The control group surprised to the upside in each of the last two reports. Thus, another positive surprise for August isn’t out of the question.

Wednesday brings the most important event of the week: the FOMC rate decision and an updated summary of economic projections (SEP). As shown below, markets are pricing in a 25-basis-point cut with near certainty. Thus, the press conference will be closely parsed for clues on whether the Fed leans toward further rate cuts in the months ahead. Housing starts and building permits data also hit before the market opens.

Thursday closes this week’s economic data with initial jobless claims. Markets will be watching closely to see if last week’s sudden jump above 260k was noise or a signal of further softening in the labor market. The Philadelphia Fed manufacturing index will also be released, providing another look into regional manufacturing conditions.

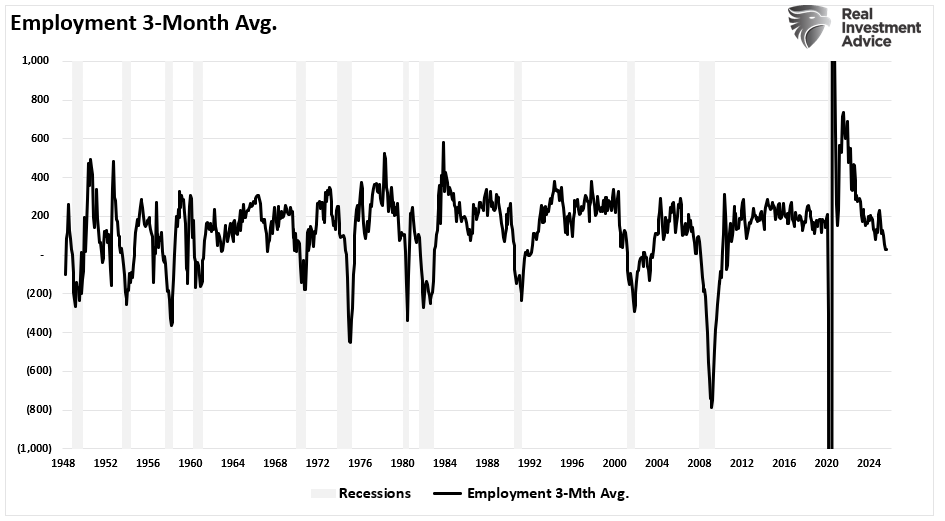

Corporate Earnings Slowdown Signaled By Employment Data

The latest employment data strongly warned of a potential corporate earnings slowdown ahead. This is the first time we have warned about the employment data and its impact on corporate earnings. In May, we penned “Employment Data Confirms Economy Is Slowing.” wherein we stated:

“Given the importance of consumption in the economy and that employment (production) must come first in the cycle, attention to employment data, particularly full-time employment, is crucial to determining economic risk. The risk of a recession remains very low; however, that can change if something causes consumption to contract quickly. Aside from an unexpected, exogenous impact, investors should expect economic growth to continue to slowly weaken to a longer-term trend slightly less than 2% annually. Unfortunately, while not recessionary, that growth rate will make it hard for corporate profitability to remain at record levels.”

The August 2025 employment report further confirmed the deceleration in job growth. Nonfarm payrolls added just 22,000 positions. Economists had expected over 75,000. June’s numbers were revised downward to a net loss of 13,000 jobs, the first monthly decline since 2020. July gained only a minor upward revision. However, what is most important is the “trend” of the data rather than just a one-month data point. As shown, the 3-month average of employment is deteriorating sharply, which has only occurred previously just before the onset of a recession.

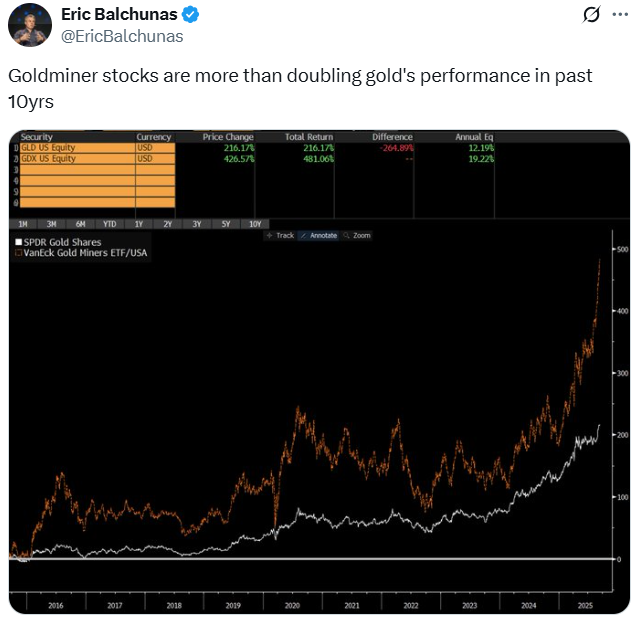

Tweet of the Day

More By This Author:

Covered Call Strategies Gone WildCorporate Earnings Slowdown Signaled By Employment Data

Oilfield Servicers Find New Hope In AI Power Demand

Comments

Log in or sign up to join the conversation.