Image Source: Pexels

Friday’s market crack certainly woke up the more complacent bullish investors. Of course, the complacency was warranted, given the recent market surge, conversations about “TINA” (There Is No Alternative), and how “this time is different.” But that is what a speculative bull run looks and feels like. However, deep inside, you know there are risks. Valuations seem insane, credit spreads are historically tight, and sentiment and trading activity push more speculative extremes. Such is why, while considered “bearish,” we discuss risk management protocols. Why? Because such actions can protect you when it matters most. This is why I want to discuss a different approach to portfolio management with you today. Rather, how to think like a “bear,” so you see the risks of the speculative bull run. However, to act like a “bull” to capture the gains while available.

But that is a difficult skill to master.

Yes, thinking like a bear means you are aware of the exceedingly high levels of investor complacency, that valuations are stretched, and credit spreads have been crushed. Furthermore, margin debt is at very high levels, which provides the fuel for the eventual downturn.

The problem with speculative bull runs is that they always end, and most of the time that ending is destructive. It is inherently logical that, as an investor, you want to move to protect your capital. The problem is that a bearish posture can lead to more severe underperformance because the market is in full speculative mode. Such is why, as an investor, it is logical to engage in bearish thinking, but must maintain a bullish bias amid a bull run. That means you must engage selectively, ride momentum where it leads, and keep disciplined exits.

As noted, that is a difficult skill to master, but that is your edge: you see the warning signs, yet you don’t surrender to them too early.

Howard Marks once argued that psychology overwhelmingly defines speculative bull runs. Price divorces value as crowds chase narratives. While the optimists win short-term, and the pessimists are mocked, Marks warns that during these periods, “value” takes a back seat and momentum becomes the dominant force. Marks underscored that manias shift the center of gravity from intrinsic worth to consensus euphoria. So when you think like a bear, your job is not to dogmatically short every overvalued name, but to structure your exposure to survive the mania’s reversal.

However, marrying the two mindsets is challenging. While valuation models can anchor your long‑term expectations, near-term indicators like relative strength and momentum overlays can help navigate potentially dangerous waters. Like any good captain in uncharted waters, they follow the navigation but pay attention to their instincts.

Why Fundamental Analysis Alone Fails in Mania Mode

Under normal conditions, valuation metrics drive returns. You buy cheap (low P/S, high free cash flow yield, strong ROE) and wait for mean reversion. But in a speculative bull run, those rules often fail. As discussed recently, high volatility and “bad balance sheet” (poor fundamentals) are what investors are chasing. That is because the perceived risk of loss is extremely low, even though it is not.

But that is what happens during market manias. As the crowd chases momentum and dismisses warnings, it pushes prices beyond what the underlying assets justify. This is what is called “valuation expansion.” As shown below, valuations, in the short term, reflect consumer (investor) sentiment. The chart shows the correlation between consumers’ expectations of higher prices in 12 months versus trailing 12-month valuations.

Warren Buffett emphasized this point, stating that in speculative manias, the market becomes a voting machine first (popularity), then later a weighing machine (intrinsic value). In mania phases, price can outrun value over long periods before eventually reverting. Betting on the value convergence too early is dangerous. The reason, as John Maynard Keynes noted, is that.“The market can remain irrational longer than you can remain solvent.”

As we discussed in a recent BullBearReport on the AI Bubble:

“The critical issue for investors, both then and now, was that many were “right” about the Dot.com bubble. However, they were so early in their warnings that they were wrong in their portfolios. The same warning applies currently. Is there a bubble in AI? Maybe. But, I would even suggest that it is pretty likely. As investors, we must realize that during the “inflation” phase of the bubble, there is a lot of money to be made, but the cycle will eventually end.”

That’s why fighting parabolic moves can be so problematic. As Peter Lynch once stated:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in the corrections themselves.”

Thus, if you followed pure valuation discipline, you would often be sidelined during the high-return leg. Worse, you might have to “catch the knife” when the reversal begins. So you need to adapt your thinking to allow “bearishness” to control risk, but remain “bullish” to allow for the fact that momentum may temporarily drive prices higher..

One pitfall, however, is correlation. Historically non-correlated assets in speculative environments will move in tandem as investors look for the next speculative opportunity. Large-cap, high volatility, emerging market, international, gold, and bitcoin are all being chased higher in the current market. Each has its own narrative to justify its move higher, but buyers’ speculative fervor outstripping supply pushes prices further. In this environment, traditional diversification will likely fail to protect you in a downturn. Your differentiation comes from picking “which” levered momentum plays to hold and having triggers to exit them before they become toxic.

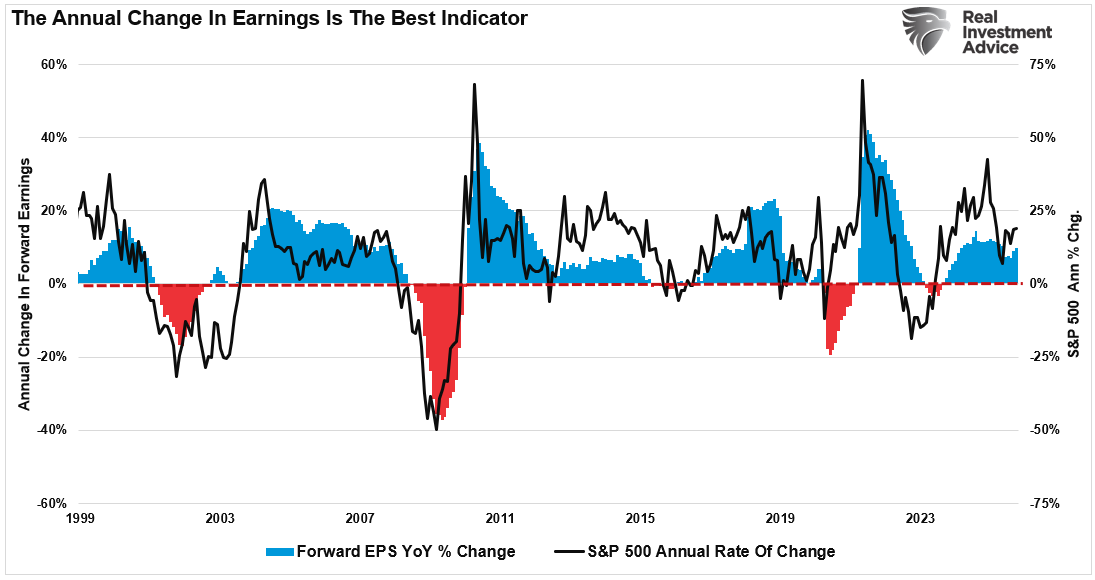

The good news is that markets do not collapse at once, and you will not wake up one morning with stocks down 50%. Instead, the initial sharp move lower will signal that some market “dynamic” has shifted. No one will ever know what that will be in advance. However, it will be an event that causes investors to “revalue” their forward earnings estimates. If those estimates decline, the current market will be repriced for lower future earnings. As shown, there is a high correlation between the market and the 12-month rate of change in forward earnings estimates.

The lesson is that valuation signals are essential but insufficient. You need momentum lenses, risk thresholds, and rules for scaling exposure and exiting when conditions shift. These give you a fighting chance in a speculative bull run.

How to Manage Risk & Exposure During the Mania

You have a framework now: think like a bear, engage like a bull, and overlay defenses. But how do you operationalize that in real portfolios? Below are the steps and principles from our approach and Mark’s wisdom.

- Establish trend break rules and define when the trend is broken. Use moving averages, momentum divergences, or multi‑timeframe trend signals. When a trend breaks, reduce exposure.

- Scale into exposure. Don’t go all in at once. Add when strength confirms. If the market corrects, your position is still manageable.

- Use stop zones and dynamic trailing thresholds. Set stop levels or trailing stops that adapt. Cut losers early. Lock in profits on winners when they begin to stall.

- Tier exposure by risk class. Have distinct layers: value core, momentum growth sleeve, and optional speculative layer. The speculative layer should be small, optional, and easy to cut.

- Monitor outside‑equity signals. Watch credit spreads, yield curves, bond markets, and sentiment extremes. Those often show cracks before equities do.

- Transition to a defensive posture incrementally. Move from “stop buying” to “reduce aggressive holdings” rather than all at once. You don’t have to hit complete defense unless the trends demand.

- Always maintain optionality. Hold dry powder. Leave capacity to enter new momentum trends or reallocate when the old ones shed. You want to be able to pivot.

- Accept uncertainty and probabilistic thinking. Risk and probability matter more than certainty. You can’t know exactly when the shift happens, but you can manage positioning around probabilities.

- Be unemotional and contrarian at extremes. Great investors are unemotional. In extremes, follow contrarian logic: reduce exposure when others lean heavily in. Resist being swept by sentiment. At mania highs, the crowd is usually at its most overextended.

- Review and adapt constantly. Conditions change. What looks good today may become a trap tomorrow. Stay vigilant. Reassess allocations regularly.

By applying these rules, you can capture much of the upside of a speculative market while protecting against the inevitable reversion.

A Roadmap: Where This Strategy Wins and When It Loses

This hybrid approach is not perfect. There are strengths, and there are risks. But it’s more durable than rigid value or blind momentum.

When it wins:

- During strong speculative rallies, where momentum dominates, investors can participate in the gains and avoid collapsing names.

- Technical signals can keep investors aligned with the market in environments where fundamentals are weak but liquidity and psychology are strong.

- When the trend eventually breaks, stop rules trigger exits, preserving investor capital.

When it struggles:

- Momentum-based strategies will fail if the trend reverses abruptly and violently without warning.

- During choppy market phases, investors will likely suffer underperformance when the trend direction is unclear, as trend signals whipsaw.

- A pure value strategy will outperform in sustained value-driven rebounds (after deep crashes), where fundamentals again dominate.

You mitigate those risks by:

- Staying light in speculative exposures

- Keeping a strong value core

- Loosening stop logic in volatile whipsaw phases

- Being ready to switch investment strategies when the cycle changes

The path isn’t perfect, but it gives you flexibility.

Think Like a Bear, Invest Like A Bull

In today’s market environment, where risk is elevated, it can pay to “think like a bear, but invest like a bull.” As Howard Marks previously wrote about navigating speculative manias:

“In hot times, the few who do remember the past are dismissed as relics of the old, lacking the ability to imagine the new. But it invariably turns out that there’s nothing new in terms of investor behavior. Mark Twain said that “history does not repeat itself, but it does rhyme,” and what rhymes are the important themes.

The bottom line is that even though knowing financial history is important, requiring people to study it won’t make a big difference, because they’ll ignore its lessons. There’s a very strong tendency for people to believe in things which, if true, would make them rich. As Demosthenes said, “For that a man wishes, he generally believes to be true”

Just like in the movies, where they show a person in a dilemma to have an angel on one side and a devil on the other, in the case of investing, investors have prudence and memory on one shoulder and greed on the other. Most of the time greed wins. As long as human nature is part of the investment environment, which it always will be, we’ll experience bubbles and crashes.“

There have only been a few points in history where the market is as overbought and extended, technically, as it is currently.

Given that knowledge, investors must learn to live in tension. Think like a bear, so you’re ready for danger. Invest like a bull to participate in the current wealth-building opportunity. No rule says you can ONLY be a bull or a bear. It is okay, and logical, to be a bit of both.

Critically, you must adopt probabilistic thinking and reject certainty.

This combined approach gives you a fighting chance in environments where liquidity and psychology override fundamentals. It also preserves your survival when sentiment eventually reverses.

More By This Author:

Rally Into Year-End: 3 Reasons To “Buy Dips”

Liquidity Warning: SOFR Raises The Red Flag

The Psychology Of Investing In A Zero-Risk Illusion

Comments

Log in or sign up to join the conversation.