Breaking Down Retail Earnings That Highlight Slowing Consumer Spending

Image Source: Unsplash

It is no surprise that the combined weight of elevated inflation, rising interest rates, and uncertainty about the economy have forced consumers to change their spending behavior.

The issue has undoubtedly been at play with lower-income households for some time now. But we can intuitively appreciate that it will not stay restricted to this consumer segment alone and will most likely move up the income chain in the days and weeks ahead.

We saw some of that in the Walmart (WMT - Free Report) report that showed the retailer benefiting from higher-income consumers ‘trading down’ to its stores in response to the aforementioned headwinds.

The retail business is a tough and competitive space even in ‘normal’ times and these are anything but normal times. They need just the right amount of inventory, otherwise, they will either lose sales if they don’t have enough merchandise as was the case earlier in the pandemic or will need to offer steeper discounts and hurt margins if they have too much of it, as we saw with Walmart and Target (TGT - Free Report) in the summer quarter.

Retailers also need to make sure that they have the right type of merchandise, as we saw with Target and Walmart having too much stuff like patio furniture that consumers weren’t interested in buying anymore after the initial pandemic boom. Keeping stores fully staffed in a tight labor market and ensuring just the right amount of price discounts are some of the other challenges that big-box operators like Walmart, Target and others face daily.

It all comes down to execution and management effectiveness.

With respect to the group’s Q3 earnings releases, it has been a mixed show overall. In a backdrop of moderating and shifting consumer spending behavior, some retailers have been more successful than others. Walmart was better, Target was not. Macy’s (M - Free Report), Foot Locker (FL - Free Report), and Lowe’s (LOW - Free Report) executed really well, but others didn’t.

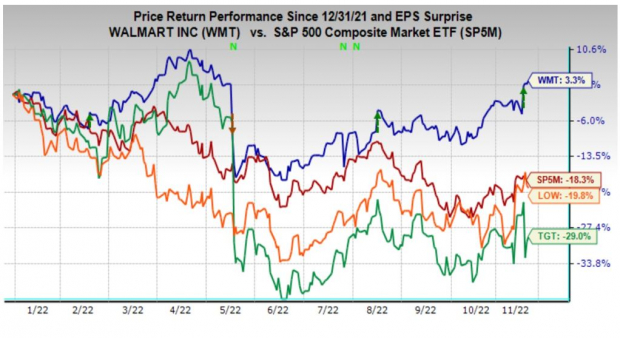

You can see some of this in the year-to-date performance of Walmart (blue line), Target (green line), Lowe’s (orange line) shares relative to the S&P 500 index (red line).

Image Source: Zacks Investment Research

With respect to the Retail sector 2022 Q3 earnings season scorecard, we now have results from 29 of the 34 retailers in the S&P 500 index.

Unlike the official S&P sector classifications that leaves retail sector players spread around different sectors, primarily Consumer Discretionary, Zacks’ stand-along Retail sector classification that houses conventional retailers, digital players and restaurants allows for a more granular understanding of trends in the space.

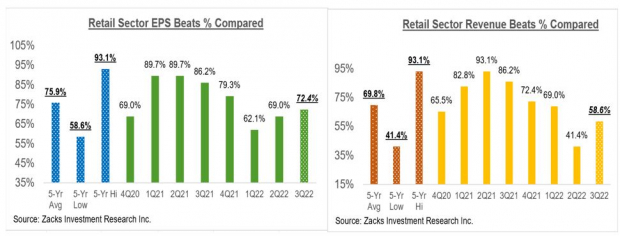

Total Q3 earnings for these retailers are down -5.5% from the same period last year on +8.6% higher revenues, with 72.4% beating EPS estimates and 58.6% beating revenue estimates.

The comparison charts below put the Q3 beats percentages for these retailers in a historical context.

Image Source: Zacks Investment Research

As you can see above, retailers have been struggling to come out with positive surprises thus far, though it’s a better showing relative to what we saw from the group 2022 Q2.

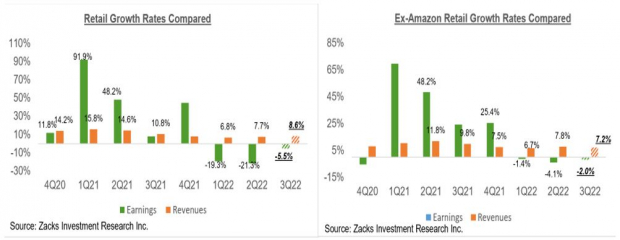

With respect to the earnings and revenue growth rates, Amazon’s weak numbers play a significant role in the year-over-year growth rate for the sector (Amazon is part of the Zacks Retail sector, and not the Zacks Technology sector).

The two comparison charts below show the Q3 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart).

Image Source: Zacks Investment Research

Q3 Earnings Season Scorecard

Including all of the results that came through Friday, November 18th, we now have Q3 results from 476 S&P 500 members that combined account for 95.2% of the index’s total membership.

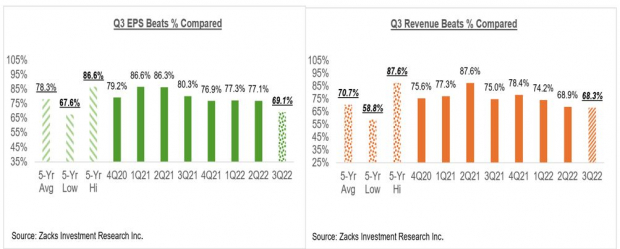

For the 476 index members that have reported results already, total earnings are up +1.8% from the same period last year on +11.8% higher revenues, with 69.1% beating EPS estimates and 68.3% beating revenue estimates.

Here is how the 2022 Q3 earnings and revenue growth rates for these companies compares across different periods.

Image Source: Zacks Investment Research

Here is how the 2022 Q3 EPS and revenue beats percentages for these companies compare across different periods.

Image Source: Zacks Investment Research

The EPS and revenue beats percentages are below what we had seen from this same group of companies in recent quarters, but otherwise within the historical range by now.

Tracking Earnings Estimate Revisions

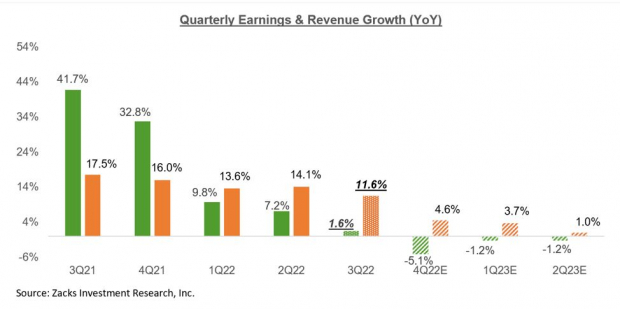

The chart below that shows the blended earnings and revenue growth for 2022 Q3 relative to what we saw in the preceding four quarters and what is expected in the coming three periods.

Image Source: Zacks Investment Research

This is no surprise, as the global economy is going through a synchronized slowdown, under the combined effects of rising interest rates in response to inflationary pressures, still-lingering logistical challenges that have started to ease up and China’s continuing zero-Covid restrictions.

The orange bars in the chart above represent revenue growth. So, for 2022 Q3, revenues are on track to grow +11.6% from the same period last year even though earnings are only expected to be up only +1.6%. This seemingly elevated revenue growth is a direct function of pricing power, with companies able to pass on rising input costs to end consumers. We intuitively know that this can’t go on forever and current projections for the next three quarters bears out this intuition.

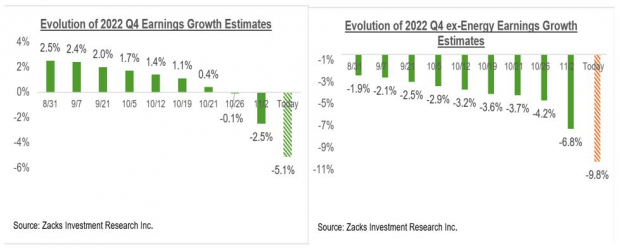

The above chart shows that earnings in the current period (2022 Q4) are expected to be down -5.1% below the year-earlier level on +4.6% higher revenues.

Estimates have been steadily coming down, in line with the trend that we saw ahead of the start of the Q3 earnings season.

Image Source: Zacks Investment Research

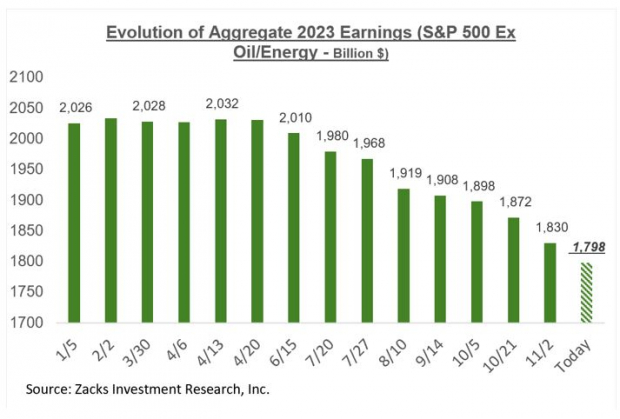

Estimates for full-year 2023 have been coming down as well, with the negative revisions trend particularly notable on an ex-Energy basis. You can see this in the chart below that shows the aggregate 2023 earnings estimate on an ex-Energy basis.

Image Source: Zacks Investment Research

Since mid-April, 2023 earnings estimates in the aggregate have come down by -8.6% for the S&P 500 index as a whole and -11.5% on an ex-Energy basis.

The cuts to estimates have been particularly notable for the Tech (down -18.9% since mid-April), Construction (-25.1%), Retail (-18.6%), Industrial Products (-14.3%), Consumer Discretionary (-19.3%) and Aerospace (-13.4%). Overall, estimates have been cut for 13 of the 16 Zacks sectors.

The chart below shows the overall earnings picture on an annual basis.

Image Source: Zacks Investment Research

There are some in the market who think that 2023 earnings should be below the 2022 level instead of the current expected +2.8% growth simply because the U.S. economy is expected to go through a moderate recession.

I am not suggesting that 2023 earnings can’t be below the 2022 level; they can be, and based on the current revisions trend, are likely headed there. But it is wrong to expect moderate declines in ‘real’ GDP to automatically result in ‘nominal’ or non-inflation adjusted corporate earnings to also decline. Corporate revenues and earnings are ‘nominal’ values and will reflect the effects of inflation. Inflation is expected to come down in 2023, but nevertheless remain positive.

More By This Author:

Previewing Retail Sector Earnings As Inventory Issues Linger

Q3 Earnings Season - Better Than Expected Or Lackluster?

3 Things We Learned From The Q3 Earnings Season

Disclosure: Zacks.com contains statements and statistics that have been obtained from sources believed to be reliable but are not guaranteed as to accuracy or completeness. References to any specific ...

more