With September-quarter results from more than 85% of S&P 500 members already out, the bulk of the Q3 reporting cycle is now behind us.

The overall takeaway from the Q3 earnings season was one of relief and reassurance, with actual quarterly reports belying pre-season fears of an impending ‘earnings cliff’. As we have repeatedly pointed out, the picture that emerged from the Q3 earnings season wasn’t great, but it wasn’t bad either. To that end, here are the three things we learned from the Q3 earnings season.

First, growth is fading. Take a look at the chart below that shows the blended earnings and revenue growth for 2022 Q3 relative to what we saw in the preceding four quarters and what is expected in the coming three periods.

Image Source: Zacks Investment Research

This is no surprise, as the global economy is going through a synchronized slowdown, under the combined effects of rising interest rates in response to inflationary pressures, still-lingering logistical challenges that have started to ease up, and China’s continuing zero-Covid restrictions.

The orange bars in the chart above represent revenue growth. So, for 2022 Q3, revenues are on track to grow +11.3% from the same period last year even though earnings are only expected to be up +1.6%. This seemingly elevated revenue growth is a direct function of pricing power, with companies able to pass on rising input costs to end consumers. We intuitively know that this can’t go on forever and current projections for the next three quarters bears out this intuition.

Second, margins are holding up better than most of us would have expected. Net margins in the aggregate have been below the year-earlier in each of the last three quarters, but the pressures aren’t distributed evenly across the different sectors.

If we look at the Q3 results that have come out already, net margins are down 130 basis points for the 429 S&P 500 members in the aggregate, with 10 of the 16 Zacks sectors suffering margin contraction. On the flip side, four sectors enjoyed higher margins relative to the year-earlier period, led by the Energy sector.

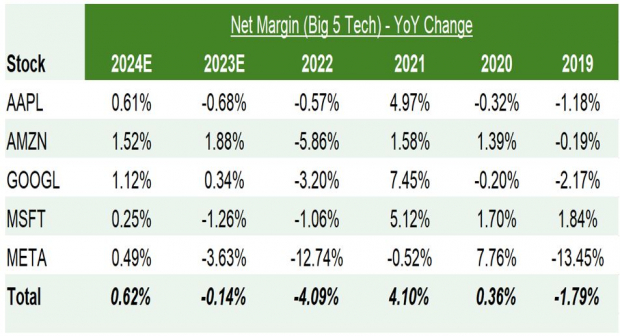

Sectors suffering the biggest margin squeeze include Technology, Basic Materials, and Finance. We discussed last week the earnings outlook for the Technology sector, particularly what we call the ‘Big 5 Tech Players’ – Apple (AAPL - Free Report), Amazon (AMZN - Free Report), Alphabet (GOOGL - Free Report), Microsoft (MSFT - Free Report) and Meta (META - Free Report).

We pointed out in that note how each of these Tech leaders was in a mad rush over the last few year-plus to add employees, which has left them with bloated payroll expenses. The issue is particularly acute with Meta and Amazon, whose net margins this year are expected to be 1274 basis points and 586 basis points, respectively below the 2021 level, as you can see in the table below.

Image Source: Zacks Investment Research

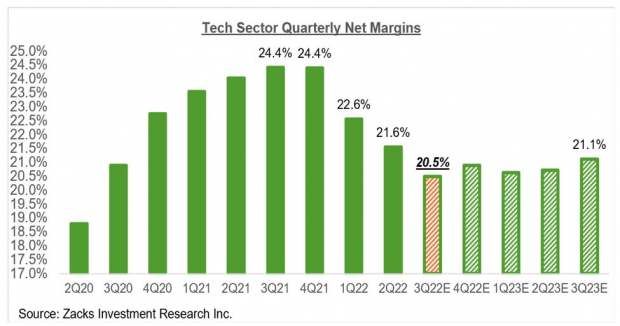

The margin issue is hardly restricted to the ‘Big 5 Tech Players’, as the issue is very much present in the broader Tech sector, as the chart below shows.

Image Source: Zacks Investment Research

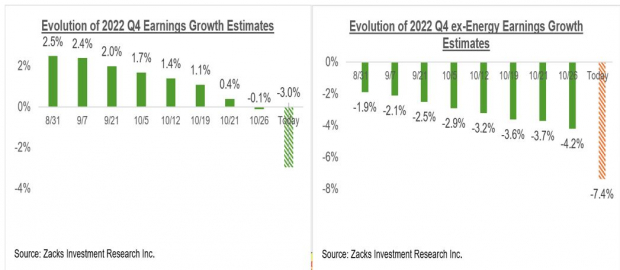

Third, the narrative that earnings estimates remain too high is misleading if not altogether wrong. Regular readers of our earnings commentary know that we have consistently flagged the persistent cuts to forward earnings estimates over the last few months.

The charts below show how earnings growth expectations for 2022 Q4 have evolved in recent weeks. The left-hand side chart shows S&P 500 earnings growth expectations in the aggregate, while the left-hand side chart shows the same data on an ex-Energy basis.

Image Source: Zacks Investment Research

We take earnings estimate revisions very seriously as they form the core of our stock-rating system. The way we see it, earnings estimates for 2023 outside of the Energy sector peaked in April and have been steadily trending down since then.

The chart below shows the aggregate 2023 earnings estimate on an ex-Energy basis.

Image Source: Zacks Investment Research

Since mid-April, 2023 earnings estimates in the aggregate have come down by -7.4% for the S&P 500 index as a whole and -10.4% on an ex-Energy basis. The cuts to estimates have been particularly notable for the Tech (down -17.4% since mid-April), Construction (-21.5%), Retail (-18.2%), Industrial Products (-11.8%), Consumer Discretionary (-15.1%), and Aerospace (-11.5%).

If we look at Amazon and Meta, 2023 earnings estimates for Amazon have come down -19.8% for Amazon (from $21.7 per share to $1.74 per share) and -30.4% for Meta (from $11.15 per share to $7.76 per share) over the last 3 months.

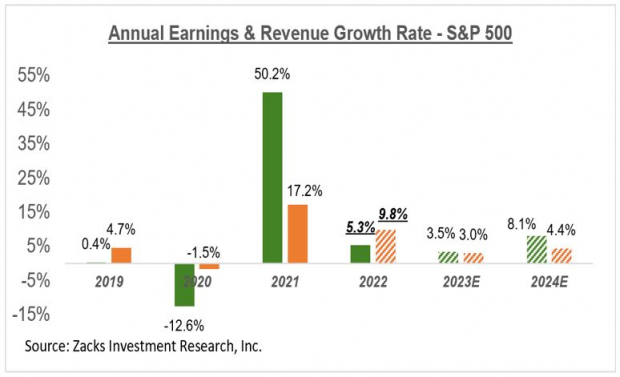

The chart below shows the overall earnings picture on an annual basis.

Image Source: Zacks Investment Research

This goes to our earlier comment about the revisions narrative being misleading if not altogether wrong. Estimates have been coming down for a while now and are down more than -10% for 2023 on an ex-Energy basis since mid-April, as we stated earlier.

There are some in the market who think that 2023 earnings should be below the 2022 level instead of the current expected +3.5% growth simply because the U.S. economy is expected to go through a moderate recession.

I am not suggesting that 2023 earnings can’t be below the 2022 level; they can be and on current revisions, trends are likely headed there. But it is wrong to expect moderate declines in ‘real’ GDP to automatically result in ‘nominal’ or non-inflation adjusted corporate earnings to also decline. Corporate revenues and earnings are ‘nominal’ values and will reflect the effects of inflation. Inflation is expected to come down in 2023 but nevertheless, remain positive.

Q3 Earnings Season Scorecard

Including all of the results through Friday, November 4th, we now have Q3 results from 429 S&P 500 members that combined account for 85.8% of the index’s total membership.

The bulk of the Q3 earnings season for the large-cap companies in the S&P 500 index is now behind us. But there are still a ton of small and mid-cap companies that have yet to report quarterly results. This week will bring in results from more than 1,000 companies, including 30 S&P 500 members.

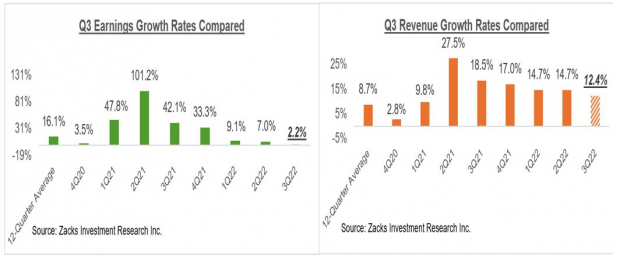

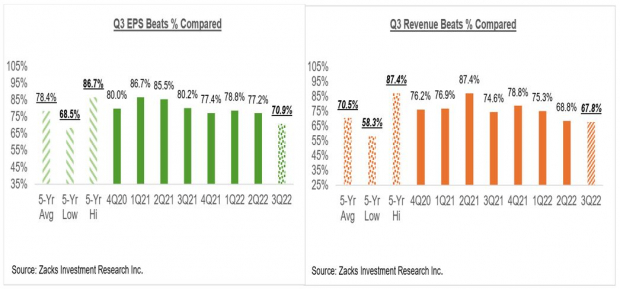

For the 429 index members that have reported results already, total earnings are up +2.2% from the same period last year on +12.4% higher revenues, with 70.9% beating EPS estimates and 67.8% beating revenue estimates.

Here is how the 2022 Q3 earnings and revenue growth rates for these 429 companies compare across different periods.

Image Source: Zacks Investment Research

Here is how the 2022 Q3 EPS and revenue beat percentages for these 429 companies compare across different periods.

Image Source: Zacks Investment Research

The EPS and revenue beat percentages were notably on the weak side earlier in the reporting cycle. But as you can see above, they are very much within the historical range by now.

More By This Author:

How To Make The Most Of Today's Market

The Earnings Picture Is Good, But Not Great

Here's What To Expect From Big Tech Earnings

Comments

Log in or sign up to join the conversation.