Image Source: Pexels

After months of steep declines and fleeting meme-fueled rallies, Beyond Meat (BYND) is once again in the spotlight – this time for its massive $900 million debt-for-equity deal. Once celebrated as the face of plant-based innovation, the company now finds itself fighting for survival amid collapsing sales, widening losses, and a heavily diluted shareholder base.

The recent restructuring, which converted hundreds of millions in debt into new shares, bought Beyond some breathing room from bankruptcy but came at a steep price –more than quadrupling the share count and leaving investors to wonder: was this a genuine lifeline, or the company’s last gasp before collapse?

Behind the headlines, Beyond’s fundamentals tell a grim story. Revenue continues to decline year-over-year, margins remain razor thin, and cash burn persists despite aggressive cost cutting. Even with short term debt relief, liquidity pressures are mounting, and management may need to raise more capital before 2026.

The brand that once symbolized the future of sustainable eating has lost its spark, as consumers increasingly turn to cheaper and simpler protein alternatives. While Beyond hopes new value priced offerings and expanded Walmart distribution can reignite demand, early results show little sign of a lasting turnaround.

Still, some investors see signs of hope. They point to Beyond’s global retail reach, well-known brand, and partnerships with restaurants as possible stabilizers. Management’s focus on cutting costs and improving efficiency could help the company move closer to breaking even by 2026.

However, many remain skeptical, arguing that Beyond’s business model is fundamentally weak – hurt by low demand, high prices, and growing competition from both real meat and other plant-based brands.

This tug-of-war between optimism and reality now defines Beyond Meat’s story. The recent stock surge – fueled more by short squeezes and social media buzz than fundamentals – underscores how speculative sentiment around the stock has become.

For long-term investors, Beyond’s future hinges on its ability to rebuild consumer trust, restore profitability, and execute a disciplined turnaround before its cash runway runs out.

The bottom line? Beyond Meat’s $900 million debt deal may have delayed the inevitable – but whether it marks a true comeback or the company’s final gasp before collapse will depend on what happens next.

Let’s map it using the IDDA (Capital, Intentional, Fundamental, Sentimental, Technical):

IDDA Point 1 & 2: Capital & Intentional

Before investing in Beyond Meat, ask yourself:

Do you want exposure to the plant-based food industry, knowing it’s in a tough cycle with shrinking demand and rising competition?

Are you comfortable investing in a company undergoing financial distress, with potential for further dilution or capital raises?

Do you believe Beyond can successfully reinvent its products and pricing strategy to win back consumers and achieve profitability by 2026?

For long term investors, Beyond Meat represents a high risk turnaround story – one that may reward only if management executes a complete strategic reset. For short term investors, the recent rally offers a case study in meme driven volatility rather than a genuine recovery.

With its financial health strained and brand appeal fading, Beyond Meat stands at a crossroads: either it evolves into a leaner, more disciplined food tech player, or it becomes another cautionary tale of hype that couldn’t hold up to reality.

IDDA Point 3: Fundamental

Beyond Meat’s financial situation remains fragile, with years of losses, falling sales, and worsening cash flow despite efforts to recover. The company has been carrying over $1 billion in debt since 2021, which led management to restructure part of it and extend repayment to 2030. While this helped reduce short term bankruptcy risk, it came at a big cost – massive dilution, with more than 316 million new shares added to the existing 76 million. The deal bought the company time but didn’t solve its main problem: a business model that continues to lose money.

Although Beyond Meat makes a small gross profit, sales are far too low to cover its high running costs. Revenue keeps falling each year, and the company is still losing large amounts of cash. Efforts to cut expenses and simplify operations have not produced lasting results, and with limited funds available, Beyond Meat may need to raise more money before 2026 unless it finds a way to turn profitable.

The brand has also lost much of its buzz since its 2020 peak, when plant-based meats were the next big thing. Many early customers never came back, saying the products are too expensive and don’t taste as good as real meat. The main retail business continues to weaken, while sales to restaurants and overseas markets haven’t grown enough to make up the difference. Management has admitted the company needs a major reset to rebuild its brand and customer base.

Price remains one of Beyond Meat’s biggest obstacles. In a cost-of-living crisis, shoppers are watching every dollar, and Beyond’s products, often several dollars more per pound than real meat, are a tough sell. CEO Ethan Brown acknowledged that higher prices are hurting sales, noting that even a $2 difference can make consumers switch back to regular meat. Until the company can cut costs or bring prices down, meaningful growth will likely stay out of reach.

At a market value of about $577 million, Beyond Meat’s stock already reflects the challenges ahead. With roughly $300 million in yearly sales and heavy losses, the company must make a major turnaround just to justify its current valuation. Management hopes to return to profitability over the next couple of years, but that goal remains uncertain. Overall, Beyond Meat’s situation paints a picture of a company still struggling to survive – weighed down by dilution, weak demand, and a business model that has yet to prove it can last.

Fundamental Risk: Very High

IDDA Point 4: Sentimental

Strengths

Short-Term Breathing Room:

Beyond Meat’s recent debt-for-shares deal pushed some payments out to 2030, easing immediate pressure and giving the company a bit more time to sort out its finances.

Focus on Cutting Costs:

Management is working to reduce expenses and run the business more efficiently, which could slowly help shrink losses and move the company closer to breaking even.

Strong Brand Name:

Even though its popularity has faded, Beyond Meat is still one of the best-known names in plant-based foods, with products sold in major supermarkets and restaurants worldwide.

Risks

Big Share Dilution and Ongoing Losses:

Turning debt into new shares added over 300 million shares, reducing the value for existing investors without solving the company’s ongoing cash problems.

Falling Sales and Customer Drop-Off:

Fewer people are buying Beyond’s products as high prices, taste issues, and waning interest in “fake meat” continue to hurt repeat sales and brand loyalty.

Hype-Driven Stock Rally:

The recent surge in Beyond Meat’s stock price came mostly from short-term social media buzz, not business improvement – leaving the stock at risk of another sharp drop once the excitement fades.

Investor sentiment toward Beyond Meat remains uncertain and mostly driven by short-term trading rather than real confidence in the business. The recent jump in share price was mainly fueled by social media buzz and a short squeeze, not by any real improvement in sales or profits. Some investors see the debt deal as a short term fix that keeps the company afloat for now, but most analysts view it as a temporary move that diluted existing shareholders and gave more control to lenders.

Overall, excitement around the stock feels more like hype than genuine optimism, with most investors staying cautious as the company’s future still depends on a very uncertain recovery in demand and profitability.

Sentimental Risk: Very High

IDDA Point 5: Technical

On the weekly chart:

The pattern has been in a clear downtrend over the past few years.

The bearish Ichimoku cloud has thinned out significantly, suggesting bearish momentum may be losing strength.

The recent bullish candlestick briefly surged above the cloud, testing it as a resistance zone before pulling back below.

Overall, the weekly chart shows a choppy downtrend with sharp swings every few months – movements that could offer short-term trading opportunities but also highlight the stock’s volatility.

The latest surge was mainly driven by a social media-fueled short squeeze rather than real business improvement. A viral post from a popular trader sparked a wave of retail buying, forcing short sellers to cover their positions and pushing prices sharply higher.

This rally also aligned with news of Beyond Meat’s $900 million debt-for-equity swap, which eased short-term bankruptcy fears but led to major share dilution. While the price temporarily broke above the Ichimoku cloud, it quickly pulled back, showing that resistance remains strong and the broader downtrend is still intact.

(Click on image to enlarge)

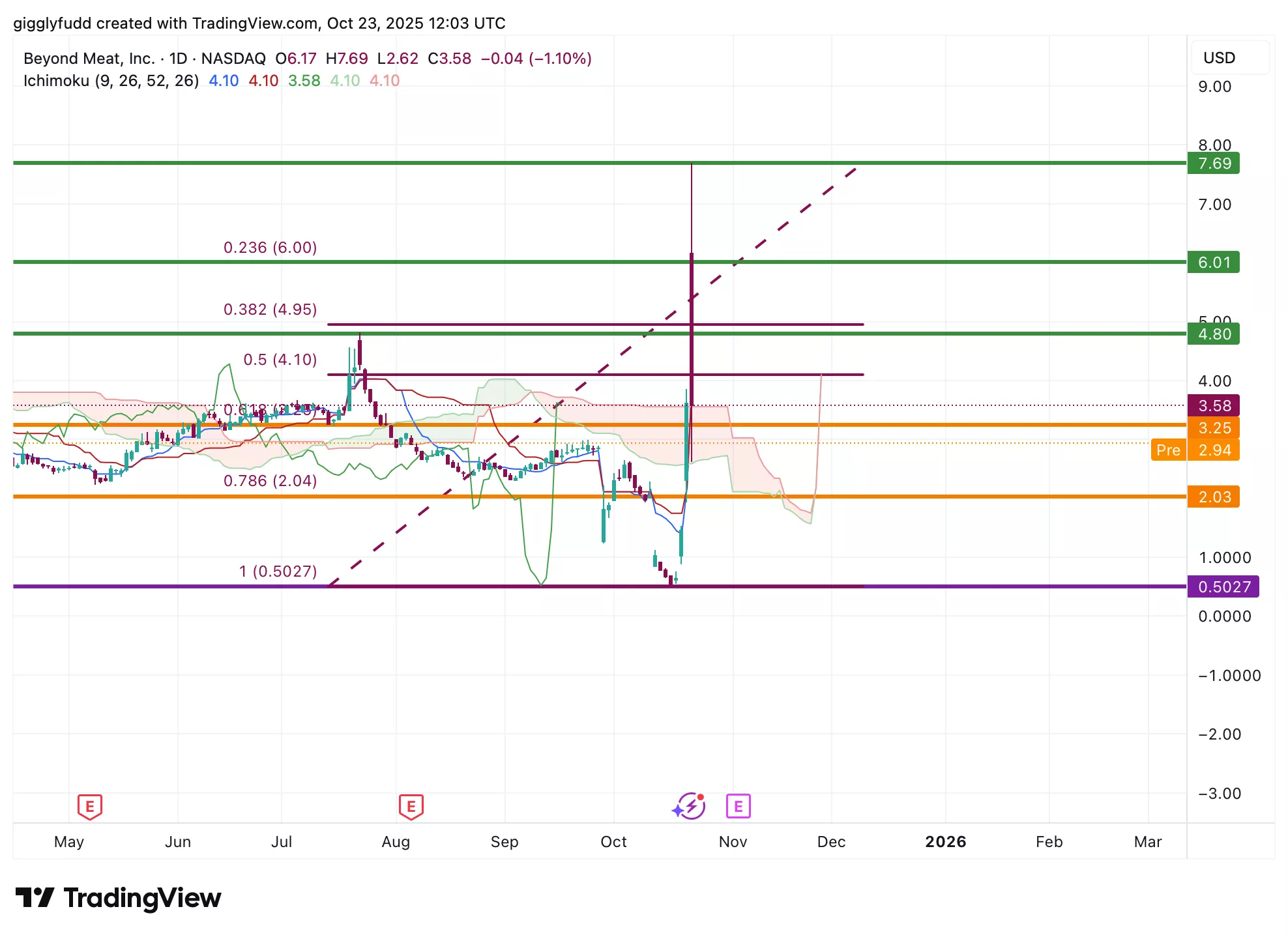

On the daily chart:

A sudden price swing pushed the stock above the Ichimoku cloud, with the cloud now acting as a short-term support zone.

A bearish engulfing pattern has formed, signaling the potential start of a new downtrend.

The bearish Ichimoku cloud has thinned out significantly, suggesting a pause or possible end to the recent bearish momentum.

On the daily chart, a sudden price swing pushed the stock above the Ichimoku cloud, which is now acting as a short-term support zone and showing some temporary upward momentum. However, a bearish engulfing pattern has appeared, signaling the possible start of a new downtrend as sellers begin to take over after the recent rally. This pattern often shows a shift in market sentiment, suggesting that buying strength is starting to fade.

At the same time, the bearish Ichimoku cloud has thinned out noticeably, hinting that the overall downward pressure could be slowing. Altogether, the chart presents mixed signals – short-term volatility with both buyers and sellers competing for control.

If the price continues to hold above the cloud, further upward momentum can be expected. However, if it breaks below the cloud, it may signal the return of downward momentum.

(Click on image to enlarge)

Investors looking to get in BYND can consider these Buy Limit Entries:

Current market price 3.58 (High Risk – FOMO entry)

3.25 (High Risk)

2.04 (Medium Risk)

0.50(LowRisk)

Investors looking to take profit can consider these Sell Limit Levels:

4.80 (Short term)

6.00 (Medium term)

7.69(Long term)

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: High

Final Thoughts on Beyond Meat (BYND)

Beyond Meat’s $900 million debt-for-equity swap has become a major turning point for the struggling plant-based company – giving it short-term breathing room but raising new long-term concerns. The deal helped reduce the immediate risk of bankruptcy by extending some debt payments to 2030, but it came with a big downside: massive dilution, which greatly increased the number of shares and weakened the value for existing investors. Once seen as a leader in the plant-based food industry, Beyond Meat is now dealing with falling sales, heavy losses, and a shrinking customer base.

The recent jump in its stock price was mostly driven by social media buzz and a short squeeze, not by real improvement in its business, leaving many investors to wonder if this “lifeline” might actually be its last chance to stay afloat. Supporters believe the deal gives Beyond time to cut costs and rebuild, pointing to its strong brand, wide retail presence, and growing partnerships like Walmart as signs it could slowly recover.

Critics, however, say the main problems remain – demand is weak, competition is increasing, and profits are still far away. The large number of new shares has also reduced potential gains for shareholders, even if sales improve. From a technical view, the stock has shown wild ups and downs, with a brief move above the Ichimoku cloud that quickly failed to hold. Unless the price can stay above that level, downward pressure could return and the longer-term downtrend may continue.

Key Takeaways:

Beyond Meat’s $900 million debt deal has given the company time – but not a clear path to recovery. Bulls see a window for turnaround if cost cuts and brand rebuilding efforts succeed. Bears view the move as a temporary fix that delays deeper financial trouble. For long-term investors, BYND remains a high-risk speculation requiring patience and conviction. For short-term investors, volatility may create quick opportunities – but without lasting fundamentals, caution is essential.

Overall Stock Risk: Very High

More By This Author:

Ferrari Stock Plunged Hard. Is It A Short-Term Drop Or A Long-Term Decline?

Coca-Cola Stock Is Quietly Making A Move Most Investors Are Missing

Has Qualcomm Finally Woken Up? The AI Breakout Wall Street Didn’t See Coming

Comments

Log in or sign up to join the conversation.